Answered step by step

Verified Expert Solution

Question

1 Approved Answer

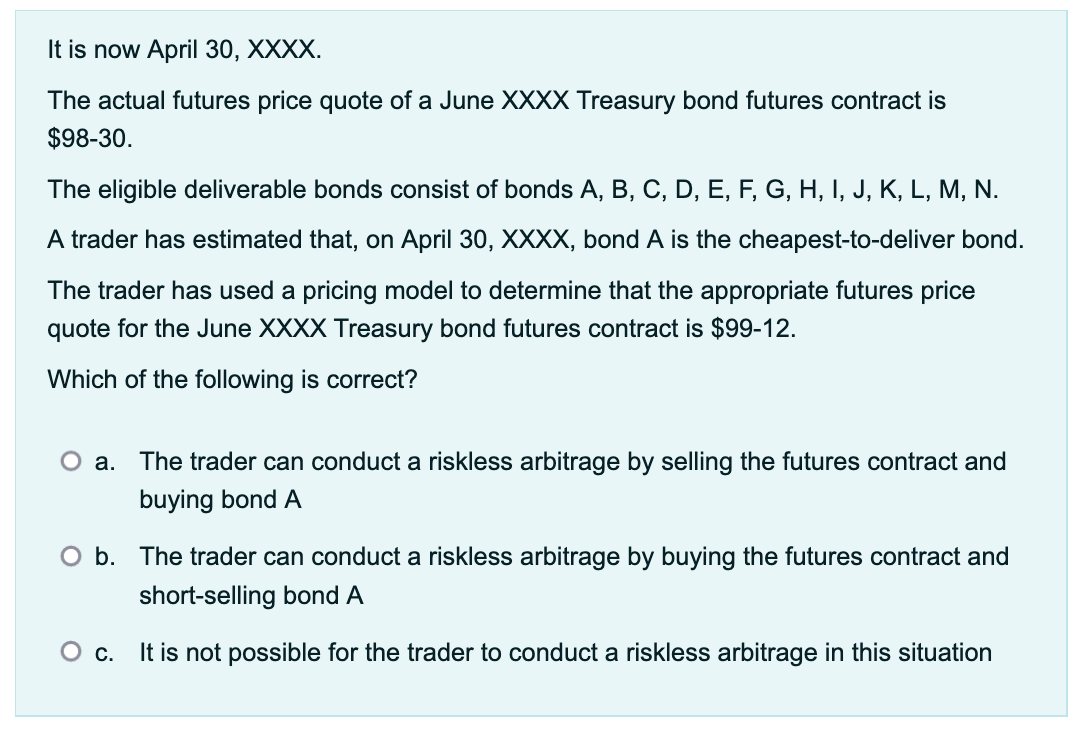

It is now April 3 0 , XXXX . The actual futures price quote of a June XXXX Treasury bond futures contract is $ 9

It is now April XXXX

The actual futures price quote of a June XXXX Treasury bond futures contract is $

The eligible deliverable bonds consist of bonds A B C D E F G H I, J K L M N

A trader has estimated that, on April XXXX bond A is the cheapesttodeliver bond.

The trader has used a pricing model to determine that the appropriate futures price quote for the June XXXX Treasury bond futures contract is $

Which of the following is correct?

a The trader can conduct a riskless arbitrage by selling the futures contract and buying bond

b The trader can conduct a riskless arbitrage by buying the futures contract and shortselling bond

c It is not possible for the trader to conduct a riskless arbitrage in this situation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Wall Street Journal Complete Personal Finance Guidebook

Authors: Jeff D. Opdyke

1st Edition

030733600X, 978-0274804573