Question

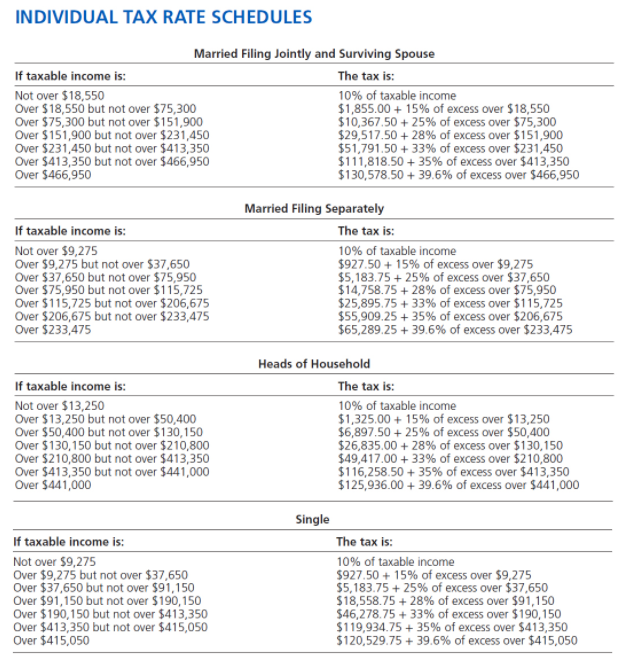

Jaclyn Biggs, who files as a head of household, never paid AMT before 2016. In 2016, her $197,900 taxable income included $178,000 ordinary income and

Jaclyn Biggs, who files as a head of household, never paid AMT before 2016. In 2016, her $197,900 taxable income included $178,000 ordinary income and a $19,900 capital gain taxed at 15 percent. Her 2016 AMTI in excess of her exemption amount was $218,175. (Round your intermediate calculations and final answers to the nearest whole dollar amount.)

a. Compute Jaclyns total income tax for 2016.

b. Assume that Jaclyn has a $5,200 minimum tax credit carryforward from 2016. Her 2017 taxable income is $179,100, all of which is ordinary income. Her 2017 AMTI in excess of her exemption amount is $146,900. Compute Jaclyns total tax for 2017 (use the 2016 tax rates) and her minimum tax carryforward into 2018.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

CIA Review Part 2 Internal Audit Practice For The New 3 Part Exam

Authors: Irvin N.Gleim

17th Edition

158194375X, 978-1581943757