Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Just Choose the right option. URGENT HELP REQUIRED! Dont need to show working. Ill surely gives u thumbs up Question 11 1 points Save Answ

Just Choose the right option. URGENT HELP REQUIRED! Dont need to show working. Ill surely gives u thumbs up

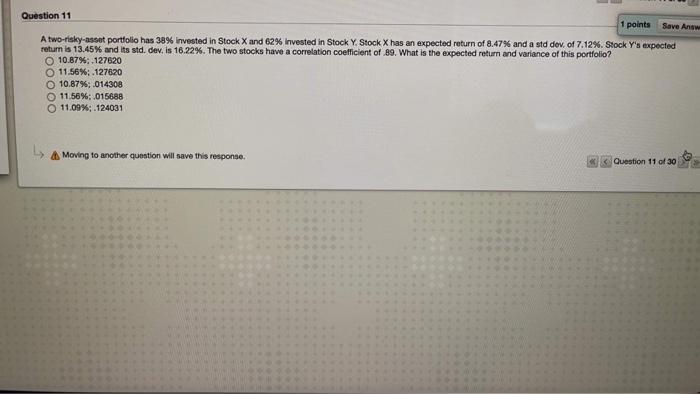

Question 11 1 points Save Answ A two-risky-asset portfolio has 38% invested in Stock X and 62% Invested in Stock Y. Stock X has an expected return of 8.47% and a std dov. of 7.12%. Stock Y's expected return is 13.45% and its std. dev. Is 16.22%. The two stocks have a correlation coefficient of 89. What is the expected return and variance of this portfolio? O 10.87% -127620 11.56%: 127620 10.87%; 014308 11.56%:.015688 11.09%;.124031 A Moving to another question will save this response. Question 11 of 30 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Full Guide To Bitcoin Investment

Authors: J.b. Yupangco

1st Edition

8389911302, 978-8389911308