Just need answers for Quetion 2 Part A and B please

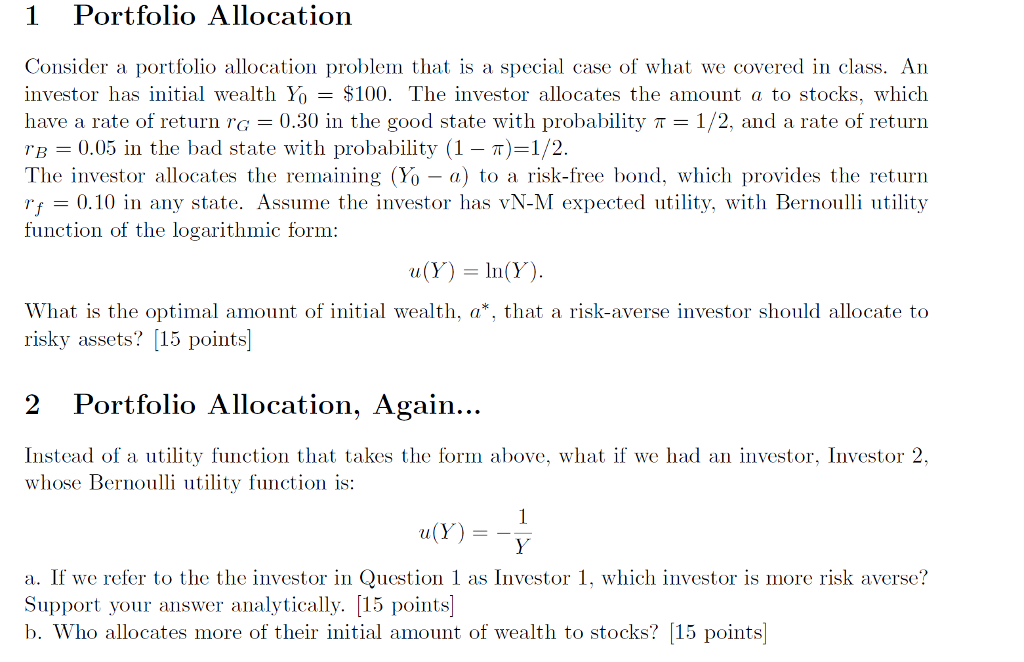

1 Portfolio Allocation Consider a portfolio allocation problem that is a special case of what we covered in class. An investor has initial wealth Yo- $100. The investor allocates the amount a to stocks, which have a rate of return r0.30 in the good state with probability T-1/2, and a rate of return rB 0.05 in the bad state with probability (1-)-1/2. The investor allocates the remaining (Yo -a) to a risk-free bond, which provides the return rf 0.10 in any state. Assume the investor has vN-M expected utility, with Bernoulli utility function of the logarithmic form: a(Y) = ln(Y). What is the optimal amount of initial wealth, a*, that a risk-averse investor should allocate to risky assets? [15 points] 2 Portfolio Allocation, Again. Instead of a utility function that takes the form above, what if we had an investor, Investor 2, whose Bernoulli utility function is: a(Y) = T a. If we refer to the the investor in Question 1 as Investor 1, which investor is more risk averse? Support your answer analytically. 15 points b. Who allocates more of their initial amount of wealth to stocks? 15 points 1 Portfolio Allocation Consider a portfolio allocation problem that is a special case of what we covered in class. An investor has initial wealth Yo- $100. The investor allocates the amount a to stocks, which have a rate of return r0.30 in the good state with probability T-1/2, and a rate of return rB 0.05 in the bad state with probability (1-)-1/2. The investor allocates the remaining (Yo -a) to a risk-free bond, which provides the return rf 0.10 in any state. Assume the investor has vN-M expected utility, with Bernoulli utility function of the logarithmic form: a(Y) = ln(Y). What is the optimal amount of initial wealth, a*, that a risk-averse investor should allocate to risky assets? [15 points] 2 Portfolio Allocation, Again. Instead of a utility function that takes the form above, what if we had an investor, Investor 2, whose Bernoulli utility function is: a(Y) = T a. If we refer to the the investor in Question 1 as Investor 1, which investor is more risk averse? Support your answer analytically. 15 points b. Who allocates more of their initial amount of wealth to stocks? 15 points