Question

Just trying to get some help on what I could possibly say here. I mean do I really say that the mortgage loans are significantly

Just trying to get some help on what I could possibly say here. I mean do I really say that the mortgage loans are significantly undercosted and the auto loans are significantly overcosted and the personal loans are slightly overcosted? That they need to price their mortgage loan fee at $730 to even get the 3.9% profit % revenue they thought they were getting under the simple costing method?

There's also a question of whether my analysis is even totally correct. How does the fact that only certain percentages of the loans get closed and the rest don't even go past the analysis stage affect the numbers?

This is a tutoring service is it not? I'm asking for help, not to answer the question for me.

ABC Problem (25 Points) (Use Excel template provided)

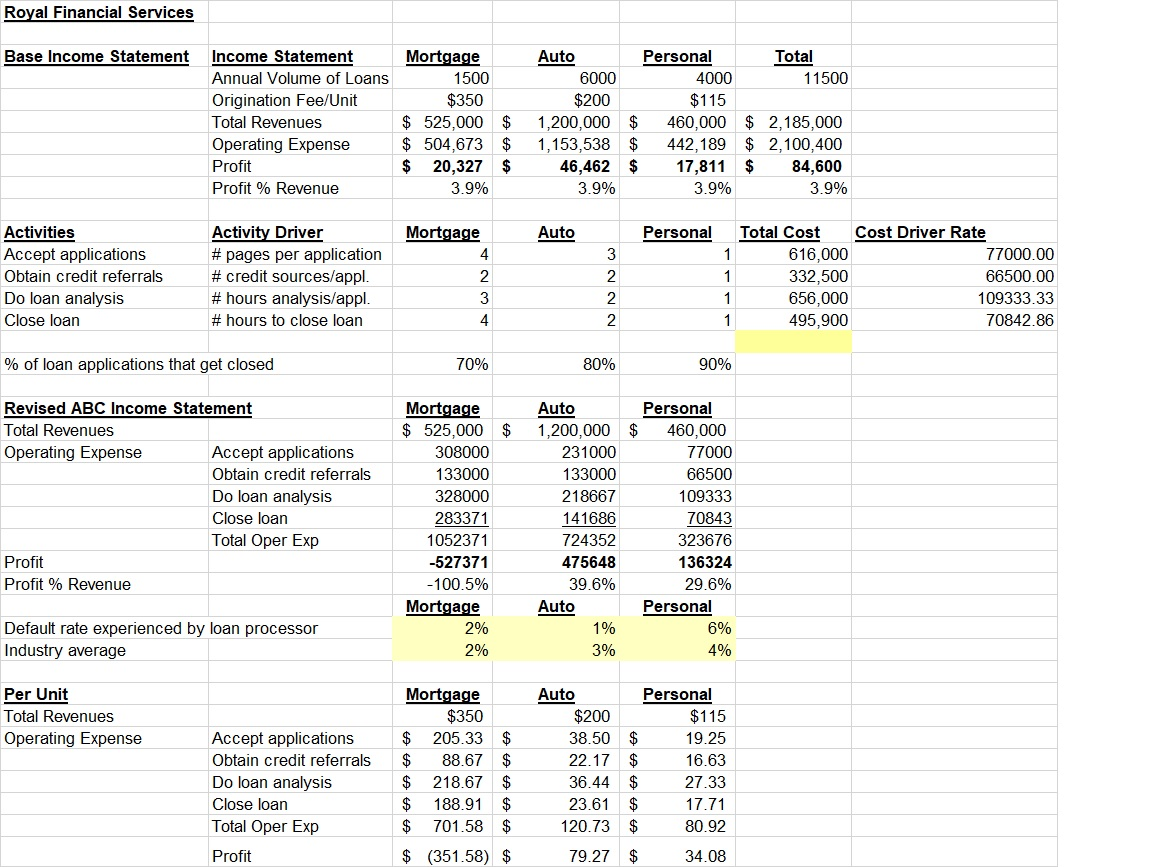

Royal Financial Services (RFS) provides front end loan origination services for a number of banks who process and maintain loan portfolios. RFS accepts applications from customers and processes them through closing of the loan agreement before turning the loan over to customer banks. RFS is paid regardless of whether the loan closes or not. RFS currently services three types of loans - residential mortgages, auto loans, and personal unsecured loans. RFS has no cost accounting system so total operating expenses are simply allocated to each product line based on revenue.

For the year just ended, RFS reported financial results as follows:

Income Statement Mortgage Auto Personal Total

Annual Volume of Loans 1500 6000 4000 11500

Origination Fee/Unit $350 $200 $115

Total Revenues $525,000 $1,200,000 $460,000 $2,185,000

Operating Expense $504,673 $1,153,538 $442,189 $2,100,400

Profit $20,327 $46,462 $17,811 $84,600

Profit % Revenue 3.9% 3.9% 3.9% 3.9%

RFS management is concerned about the overall low profitability of the business and has asked you to apply activity-based analysis in order to give RFS a better understanding of relative product profitability. After extensive interviewing of staff and analysis of RFS's cost structure, you determine there are four primary activities that RFS performs, with cost drivers and total cost as follows:

Activities Activity Driver Mortgage Auto Personal Total Cost

Accept applications # pages per application 4 3 1 616,000

Obtain credit referrals # credit sources/applic. 2 2 1 332,500

Do loan analysis # hours analysis/applic. 3 2 1 656,000

Close loan # hours to close loan 4 2 1 495,900

You determine that the application processing and loan analysis activities are performed using internal RFS resources while the credit and closing activities are performed primarily by external credit agencies and law offices on a per transaction basis (e.g. $X per credit check, $Y per closing hour). You also learn 70% of the mortgages end up being closed (the remainder are not approved after loan analysis); 80% of auto loans close and 90% of personal loans close.

You also identify a key external measure of how well RFS is performing versus the industry. While RFS does not bear the cost of defaults, their customers do track RFS performance and use it to negotiate future origination fee rates.

Mortgage Auto Personal

Default rate experienced by loan processor 2% 1% 6%

Industry average 2% 3% 4%

Here is my analysis

Royal Financial Services Base Income Statement Income Statement Annual Volume of Loans Origination Fee/Unit Mortgage Auto Personal Total 1500 6000 4000 11500 $350 $200 $115 Total Revenues $ 525,000 $ 1,200,000 $ 460,000 $2,185,000 Operating Expense $ 504,673 $ 1,153,538 $ 442,189 $2,100,400 Profit $ 20,327 $ 46,462 $ 17,811 Profit % Revenue 3.9% 3.9% 3.9% $ 84,600 3.9% Activities Accept applications Obtain credit referrals Do loan analysis Close loan % of loan applications that get closed Revised ABC Income Statement Activity Driver #pages per application Mortgage Auto Personal Total Cost Cost Driver Rate 4 3 1 616,000 77000.00 # credit sources/appl. 2 2 1 332,500 66500.00 # hours analysis/appl. 3 2 1 656,000 109333.33 # hours to close loan 4 2 1 495,900 70842.86 70% 80% 90% Mortgage Auto Personal Total Revenues $ 525,000 $ 1,200,000 $ 460,000 Operating Expense Accept applications 308000 231000 77000 Obtain credit referrals 133000 133000 66500 Do loan analysis 328000 218667 109333 Close loan 283371 141686 70843 Total Oper Exp 1052371 724352 323676 Profit -527371 475648 136324 Profit % Revenue -100.5% 39.6% 29.6% Mortgage Auto Personal Default rate experienced by loan processor 2% 1% 6% Industry average 2% 3% 4% Per Unit Mortgage Auto Personal Total Revenues $350 $200 $115 Operating Expense Accept applications $ 205.33 $ 38.50 $ 19.25 Obtain credit referrals $ 88.67 $ 22.17 $ 16.63 Do loan analysis $ 218.67 $ 36.44 $ 27.33 Close loan $ 188.91 $ 23.61 $ 17.71 Total Oper Exp $ 701.58 $ 120.73 $ 80.92 Profit $ (351.58) $ 79.27 $ 34.08

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurship

Authors: Andrew Zacharakis, William D Bygrave

5th Edition

1119563097, 9781119563099