Answered step by step

Verified Expert Solution

Question

1 Approved Answer

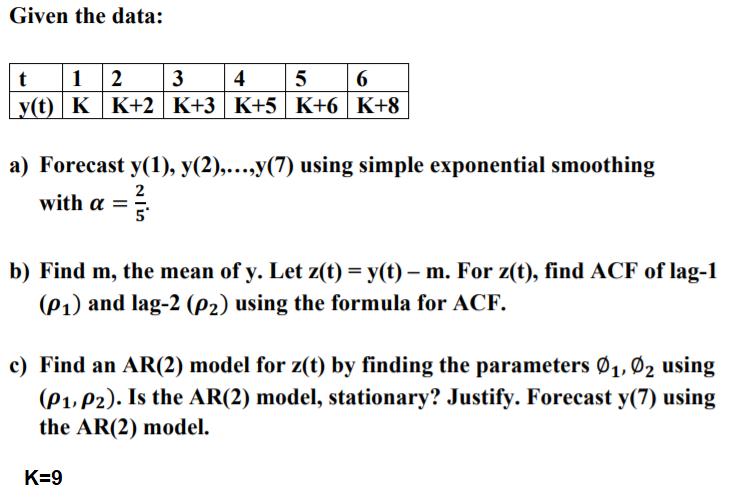

Given the data: 12 y(t) K K+2 K+3 K+5 K+6 K+8 3 4 5 6. a) Forecast y(1), y(2),...,y(7) using simple exponential smoothing 2

Given the data: 12 y(t) K K+2 K+3 K+5 K+6 K+8 3 4 5 6. a) Forecast y(1), y(2),...,y(7) using simple exponential smoothing 2 with a = 5* b) Find m, the mean of y. Let z(t) = y(t) m. For z(t), find ACF of lag-1 (P1) and lag-2 (P2) using the formula for ACF. c) Find an AR(2) model for z(t) by finding the parameters 1, 02 using (P1, P2). Is the AR(2) model, stationary? Justify. Forecast y(7) using the AR(2) model. K=9

Step by Step Solution

★★★★★

3.45 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistical Techniques In Business And Economics

Authors: Douglas Lind, William Marchal, Samuel Wathen

18th Edition

1260239470, 978-1260239478