Answered step by step

Verified Expert Solution

Question

1 Approved Answer

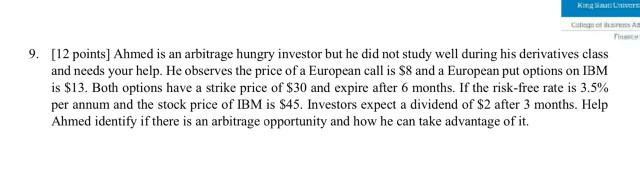

Katrs Callage 9. [12 points) Ahmed is an arbitrage hungry investor but he did not study well during his derivatives class and needs your help.

Katrs Callage 9. [12 points) Ahmed is an arbitrage hungry investor but he did not study well during his derivatives class and needs your help. He observes the price of a European call is $8 and a European put options on IBM is $13. Both options have a strike price of $30 and expire after 6 months. If the risk-free rate is 3.5% per annum and the stock price of IBM is $45. Investors expect a dividend of $2 after 3 months. Help Ahmed identify if there is an arbitrage opportunity and how he can take advantage of it

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investing All In One For Dummies

Authors: Eric Tyson

2nd Edition

1119873037, 978-1119873037