Answered step by step

Verified Expert Solution

Question

1 Approved Answer

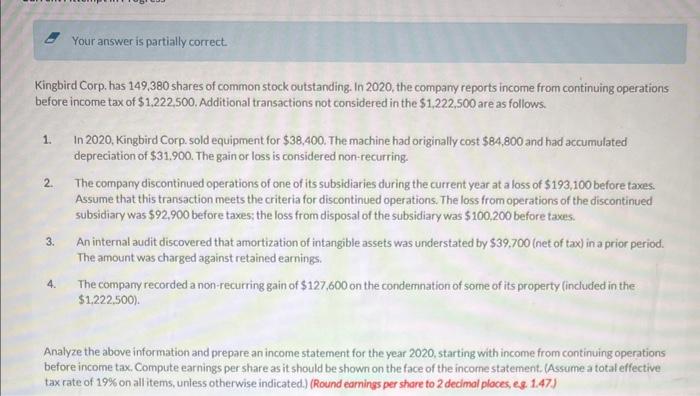

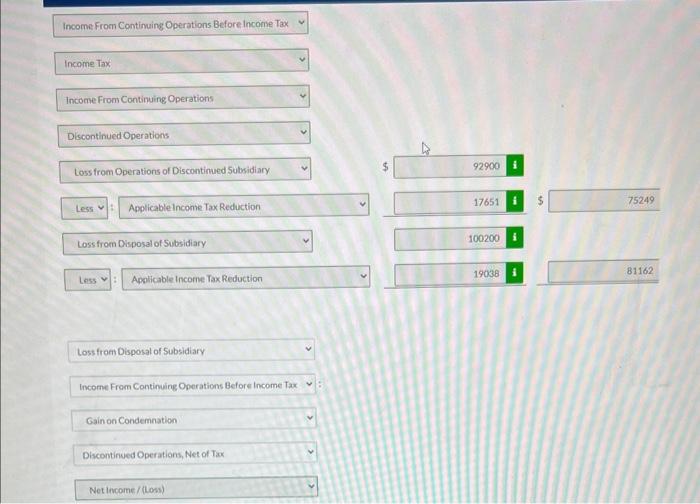

Kingbird Corp. has 149,380 shares of common stock outstanding. In 2020, the company reports income from continuing operations. before income tax of $1,222,500. Additional transactions

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Design Implementation And Audit Of Occupational Health And Safety Management Systems

Authors: Ron C. McKinnon

1st Edition

1032571039, 978-1032571034