Answered step by step

Verified Expert Solution

Question

1 Approved Answer

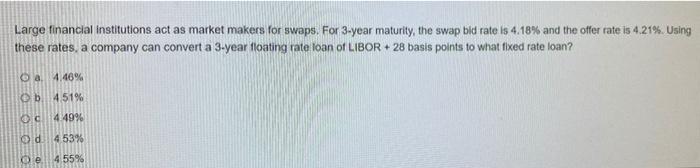

Large financial institutions act as market makers for swaps. For 3-year maturity, the swap bid rate is 4.18% and the offer rate is 4.21%. Using

Large financial institutions act as market makers for swaps. For 3-year maturity, the swap bid rate is 4.18% and the offer rate is 4.21%. Using these rates, a company can convert a 3-year floating rate loan of LIBOR + 28 basis points to what fixed rate loan? a 4.46% 4.51% Od 4.4996 Od 4539 Oe 4 55%

Large financial institutions act as market makers for swaps. For 3-year maturity, the swap bid rate is 4.18% and the offer rate is 4.21%. Using these rates, a company can convert a 3-year floating rate loan of LIBOR + 28 basis points to what fixed rate loan? a 4.46% 4.51% Od 4.4996 Od 4539 Oe 4 55%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management In Forex How To Minimize Losses And Maximize Returns

Authors: Eunice Loar

1st Edition

979-8388778864