Answered step by step

Verified Expert Solution

Question

1 Approved Answer

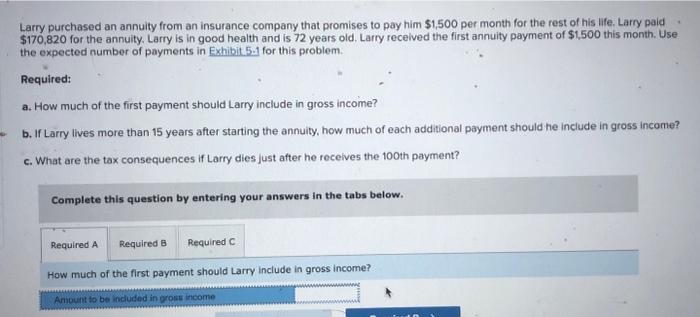

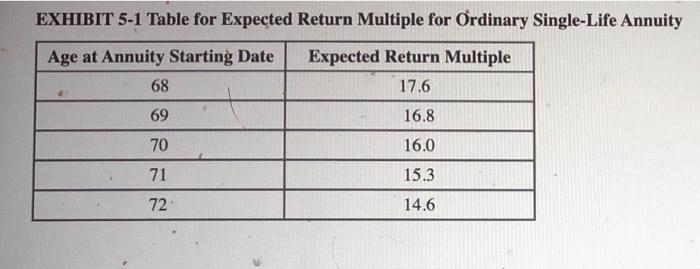

Larry purchased an annuity from an insurance company that promises to pay him $1,500 per month for the rest of his life. Larry paid $170,820

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Privacy In Practice Establish And Operationalize A Holistic Data Privacy Program Security Audit Leadership Series

Authors: Alan Tang

1st Edition

1032125470, 978-1032125473