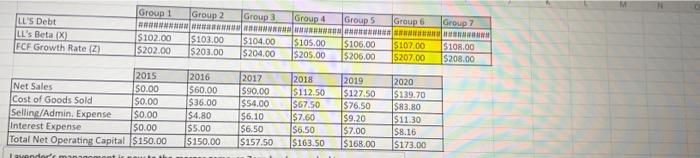

Lavender Repair Company, a regional hardware chain that specializes in "do it yourself" materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative uses for the excess funds is an acquisition. Doug Zona, Lavender's treasurer, and your boss, has been asked to place a value on a potential target, Lyons Lighting (u), a chain that operates in several adjacent states, and he has enlisted your help. The table below indicates Zona's estimates of Lil's earnings potential if it came under Lavender's management (in millions of dollars). The interest expense listed here includes the interest: (1) on L's existing debt, which is $ million at a rate of 9%, and (2) on new debt expected to be issued over time to help finance expansion within the new division, the code name given to the target firm. If acquired, LL will face a 35% tax rate. Security analysts estimate Ll's beta to be X. The acquisition would not change Lyons' capital structure, which is 22% debt. Zona realizes that Lyons Lighting's business plan also requires certain levels of operating capital and that the annual investment could be significant. The required levels of total net operating capital are listed in the table. Zona estimates the risk-free rate to be 7.2% and the market risk premium to be 4.75%. He also estimates that free cash flows after 2020 will grow at a constant rate of 2%. Group 3 Group 4 Group 5 Group 6 Group? LL'S Debt LL's Beta X) FCF Growth Rate (Z) Group 1 Group 2 HOW $102.00 $103.00 $202.00 $203.00 $104.00 $204.00 $105.00 S205.00 $106.00 $206.00 $107.00 5207.00 5108.00 $208.00 2019 2015 Net Sales $0.00 Cost of Goods Sold $0.00 Selling/Admin. Expense $0.00 Interest Expense $0.00 Total Net Operating Capital $150.00 2016 1560.00 $36.00 $4,80 $5.00 $150.00 2017 S90.00 $54.00 $6.10 $6,50 $157,50 2018 $112.50 $67.50 $7.60 $6.50 $163.50 $127.50 $76.50 $9,20 $7.00 $168.00 2020 $139.70 $83.80 $11.30 $8.16 $173.00 2 Conceptually, what is the appropriate discount rate to apply to the cash flows developed in parte? What is your actual estimate of this discount rate? F What is the estimated horizon, or continuing value of the acquisition that is, what is the estimated value of the L division's cash flows beyond 2020? What is Ll's value to Lavender's shareholders? Suppose another firm were evaluating Lt as an acquisition candidate. Would it obtain the same value? Explain. Lavender Repair Company, a regional hardware chain that specializes in "do it yourself" materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative uses for the excess funds is an acquisition. Doug Zona, Lavender's treasurer, and your boss, has been asked to place a value on a potential target, Lyons Lighting (u), a chain that operates in several adjacent states, and he has enlisted your help. The table below indicates Zona's estimates of Lil's earnings potential if it came under Lavender's management (in millions of dollars). The interest expense listed here includes the interest: (1) on L's existing debt, which is $ million at a rate of 9%, and (2) on new debt expected to be issued over time to help finance expansion within the new division, the code name given to the target firm. If acquired, LL will face a 35% tax rate. Security analysts estimate Ll's beta to be X. The acquisition would not change Lyons' capital structure, which is 22% debt. Zona realizes that Lyons Lighting's business plan also requires certain levels of operating capital and that the annual investment could be significant. The required levels of total net operating capital are listed in the table. Zona estimates the risk-free rate to be 7.2% and the market risk premium to be 4.75%. He also estimates that free cash flows after 2020 will grow at a constant rate of 2%. Group 3 Group 4 Group 5 Group 6 Group? LL'S Debt LL's Beta X) FCF Growth Rate (Z) Group 1 Group 2 HOW $102.00 $103.00 $202.00 $203.00 $104.00 $204.00 $105.00 S205.00 $106.00 $206.00 $107.00 5207.00 5108.00 $208.00 2019 2015 Net Sales $0.00 Cost of Goods Sold $0.00 Selling/Admin. Expense $0.00 Interest Expense $0.00 Total Net Operating Capital $150.00 2016 1560.00 $36.00 $4,80 $5.00 $150.00 2017 S90.00 $54.00 $6.10 $6,50 $157,50 2018 $112.50 $67.50 $7.60 $6.50 $163.50 $127.50 $76.50 $9,20 $7.00 $168.00 2020 $139.70 $83.80 $11.30 $8.16 $173.00 2 Conceptually, what is the appropriate discount rate to apply to the cash flows developed in parte? What is your actual estimate of this discount rate? F What is the estimated horizon, or continuing value of the acquisition that is, what is the estimated value of the L division's cash flows beyond 2020? What is Ll's value to Lavender's shareholders? Suppose another firm were evaluating Lt as an acquisition candidate. Would it obtain the same value? Explain