Law 505

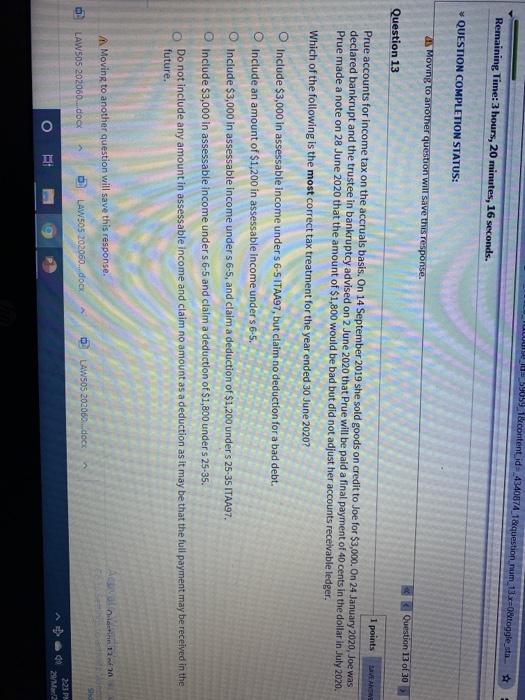

10 = 59059_1&content id=4340874_1&question num 13xO&toggle_sta Remaining Time: 3 hours, 20 minutes, 16 seconds. * QUESTION COMPLETION STATUS: AS Moving to another question will save this response. Question 13 of 30 Question 13 1 points Prue accounts for income tax on the accruals basis. On 14 September 2019 she sold goods on credit to Joe for $3,000. On 24 January 2020, Joe was declared bankrupt and the trustee in bankruptcy advised on 2 June 2020 that Prue will be paid a final payment of 40 cents in the dollar in July 2020. Prue made a note on 28 June 2020 that the amount of $1,800 would be bad but did not adjust her accounts receivable ledger. Which of the following is the most correct tax treatment for the year ended 30 June 2020? Include $3,000 in assessable Income under s 6-5 ITAA97, but claim no deduction for a bad debt. Include an amount of $1,200 in assessable income under s 6-5. Include $3,000 in assessable income under s 6-5, and claim a deduction of $1,200 unders 25-35 ITAA97. Include $3,000 in assessable income under s 6-5 and claim a deduction of $1,800 unders 25-35. Do not include any amount in assessable income and claim no amount as a deduction as it may be that the full payment may be received in the future. di 220 Moving to another question will save this response. D LAW505 202060...docx TAW505 202060..docx LAW 505 202060...docx O 29/ M2 RI 10 = 59059_1&content id=4340874_1&question num 13xO&toggle_sta Remaining Time: 3 hours, 20 minutes, 16 seconds. * QUESTION COMPLETION STATUS: AS Moving to another question will save this response. Question 13 of 30 Question 13 1 points Prue accounts for income tax on the accruals basis. On 14 September 2019 she sold goods on credit to Joe for $3,000. On 24 January 2020, Joe was declared bankrupt and the trustee in bankruptcy advised on 2 June 2020 that Prue will be paid a final payment of 40 cents in the dollar in July 2020. Prue made a note on 28 June 2020 that the amount of $1,800 would be bad but did not adjust her accounts receivable ledger. Which of the following is the most correct tax treatment for the year ended 30 June 2020? Include $3,000 in assessable Income under s 6-5 ITAA97, but claim no deduction for a bad debt. Include an amount of $1,200 in assessable income under s 6-5. Include $3,000 in assessable income under s 6-5, and claim a deduction of $1,200 unders 25-35 ITAA97. Include $3,000 in assessable income under s 6-5 and claim a deduction of $1,800 unders 25-35. Do not include any amount in assessable income and claim no amount as a deduction as it may be that the full payment may be received in the future. di 220 Moving to another question will save this response. D LAW505 202060...docx TAW505 202060..docx LAW 505 202060...docx O 29/ M2 RI