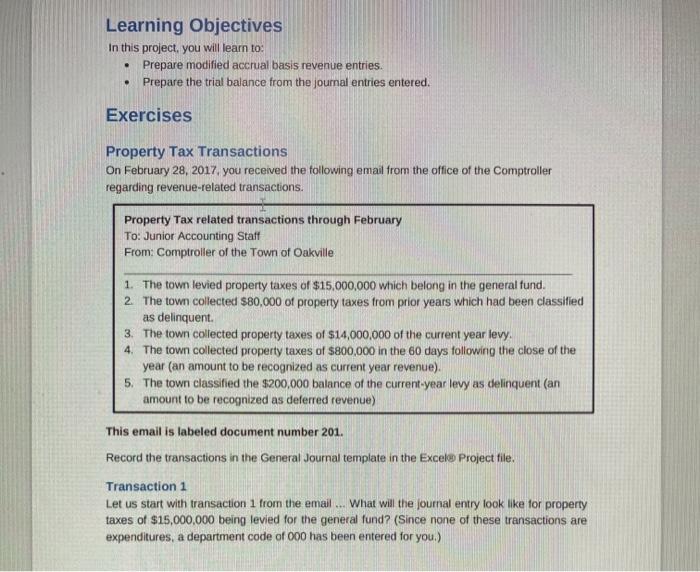

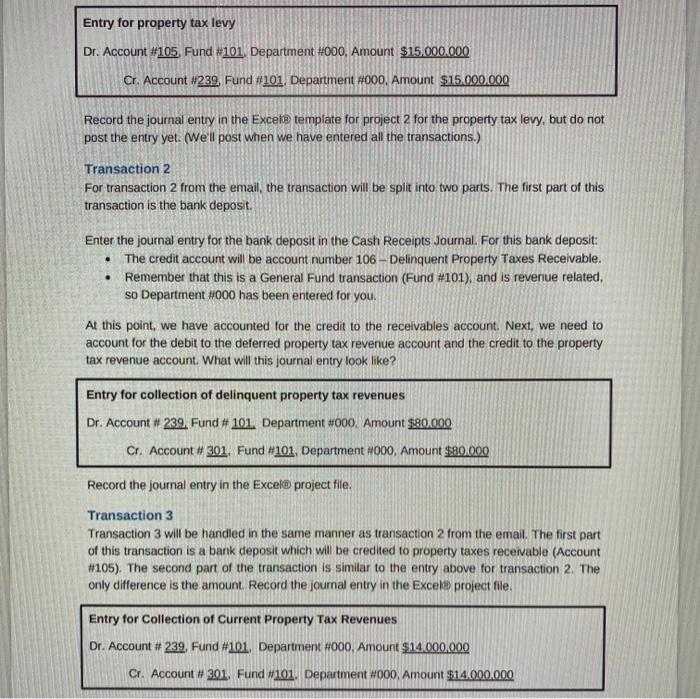

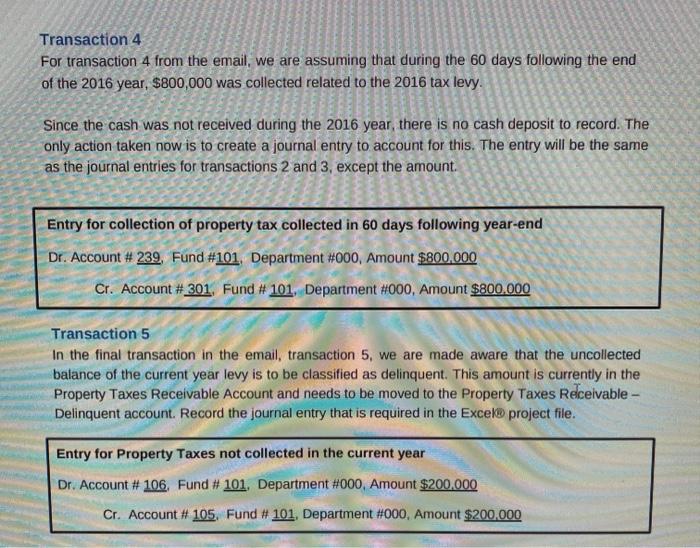

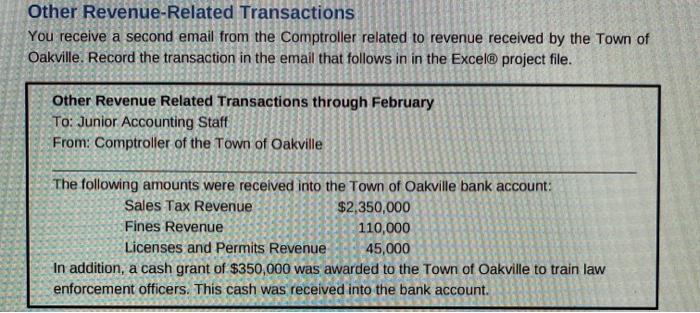

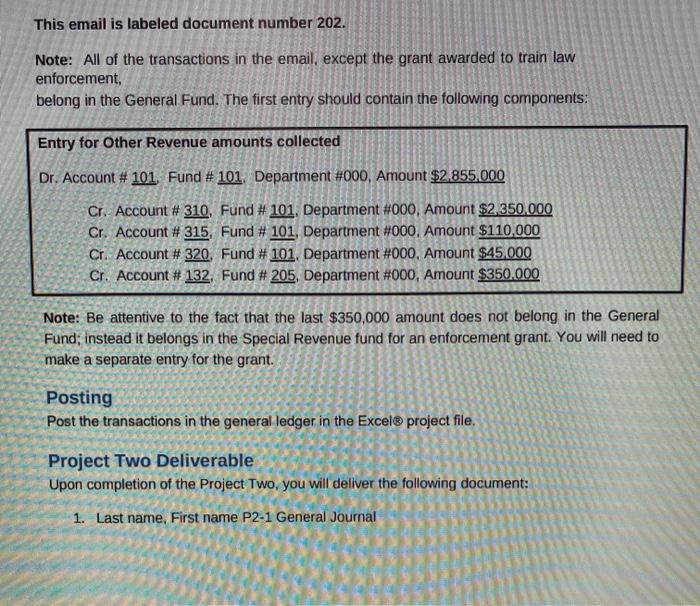

Learning Objectives In this project, you will learn to Prepare modified accrual basis revenue entries. Prepare the trial balance from the journal entries entered. Exercises Property Tax Transactions On February 28, 2017. you received the following email from the office of the Comptroller regarding revenue-related transactions. Property Tax related transactions through February To: Junior Accounting Staff From: Comptroller of the Town of Oakville 1. The town levied property taxes of $15,000,000 which belong in the general fund. 2. The town collected $80,000 of property taxes from prior years which had been classified as delinquent. 3. The town collected property taxes of $14,000,000 of the current year levy. 4. The town collected property taxes of $800,000 in the 60 days following the close of the year (an amount to be recognized as current year revenue). 5. The town classified the $200,000 balance of the current year levy as delinquent (an amount to be recognized as deferred revenue) This email is labeled document number 201. Record the transactions in the General Journal template in the Excel Project file. Transaction 1 Let us start with transaction 1 from the email... What will the journal entry look like for property taxes of $15,000,000 being levied for the general fund? (Since none of these transactions are expenditures, a department code of 000 has been entered for you.) Entry for property tax levy Dr. Account #105 Fund #101, Department #000, Amount $15.000.000 Cr. Account #239. Fund #101, Department #000, Amount $15.000.000 Record the journal entry in the Excele template for project 2 for the property tax levy, but do not post the entry yet. (We'll post when we have entered all the transactions.) Transaction 2 For transaction 2 from the email, the transaction will be split into two parts. The first part of this transaction is the bank deposit. . Enter the journal entry for the bank deposit in the Cash Receipts Journal. For this bank deposit: The credit account will be account number 106 - Delinquent Property Taxes Receivable. Remember that this is a General Fund transaction (Fund #101), and is revenue related, so Department w000 has been entered for you. . At this point, we have accounted for the credit to the receivables account. Next, we need to account for the debit to the deferred property tax revenue account and the credit to the property tax revenue account. What will this journal entry look like? Entry for collection of delinquent property tax revenues Dr. Account # 239. Fund# 101. Department #000. Amount $80.000 Cr. Account # 301. Fund #101, Department #000, Amount $80.000 Record the journal entry in the Excel project file. Transaction 3 Transaction 3 will be handled in the same manner as transaction 2 from the email. The first part of this transaction is a bank deposit which will be credited to property taxes receivable (Account #105). The second part of the transaction is similar to the entry above for transaction 2. The only difference is the amount. Record the journal entry in the Excel project file. Entry for Collection of Current Property Tax Revenues Dr. Account # 239, Fund #101, Department #000. Amount $14.000.000 Cr. Account #301, Fund #101. Department #000, Amount $14.000.000, Transaction 4 For transaction 4 from the email, we are assuming that during the 60 days following the end of the 2016 year, $800,000 was collected related to the 2016 tax levy. Since the cash was not received during the 2016 year, there is no cash deposit to record. The only action taken now is to create a journal entry to account for this. The entry will be the same as the journal entries for transactions 2 and 3, except the amount. Entry for collection of property tax collected in 60 days following year-end Dr. Account # 239, Fund #101, Department #000, Amount $800,000 Cr. Account # 301, Fund # 101, Department #000, Amount $800.000 Transaction 5 In the final transaction in the email, transaction 5, we are made aware that the uncollected balance of the current year levy is to be classified as delinquent. This amount is currently in the Property Taxes Receivable Account and needs to be moved to the Property Taxes Receivable - Delinquent account. Record the journal entry that is required in the Excel project file. Entry for Property Taxes not collected in the current year Dr. Account # 106, Fund # 101, Department #000, Amount $200,000 Cr. Account # 105, Fund # 101, Department #000, Amount $200,000 Other Revenue-Related Transactions You receive a second email from the Comptroller related to revenue received by the Town of Oakville. Record the transaction in the email that follows in in the Excel project file. Other Revenue Related Transactions through February To: Junior Accounting Staff From: Comptroller of the Town of Oakville The following amounts were received into the Town of Oakville bank account: Sales Tax Revenue $2,350,000 Fines Revenue 110,000 Licenses and Permits Revenue 45,000 In addition, a cash grant of $350,000 was awarded to the Town of Oakville to train law enforcement officers. This cash was received into the bank account. This email is labeled document number 202. Note: All of the transactions in the email, except the grant awarded to train law enforcement, belong in the General Fund. The first entry should contain the following components: Entry for Other Revenue amounts collected Dr. Account # 101 Fund # 101 Department #000, Amount $2.855.000 Cr. Account # 310, Fund # 101, Department #000, Amount $2.350.000 Cr. Account # 315, Fun 101, Department #000, Amount $110,000 Cr. Account # 320, Fund # 101, Department #000. Amount $45.000 Cr. Account # 132. Fund #205, Department #000, Amount $350.000 Note: Be attentive to the fact that the last $350,000 amount does not belong in the General Fund; instead it belongs in the Special Revenue fund for an enforcement grant. You will need to make a separate entry for the grant. Posting Post the transactions in the general ledger in the Excel project file. Project Two Deliverable Upon completion of the Project Two, you will deliver the following document: 1. Last name, First name P2-1 General Journal Learning Objectives In this project, you will learn to Prepare modified accrual basis revenue entries. Prepare the trial balance from the journal entries entered. Exercises Property Tax Transactions On February 28, 2017. you received the following email from the office of the Comptroller regarding revenue-related transactions. Property Tax related transactions through February To: Junior Accounting Staff From: Comptroller of the Town of Oakville 1. The town levied property taxes of $15,000,000 which belong in the general fund. 2. The town collected $80,000 of property taxes from prior years which had been classified as delinquent. 3. The town collected property taxes of $14,000,000 of the current year levy. 4. The town collected property taxes of $800,000 in the 60 days following the close of the year (an amount to be recognized as current year revenue). 5. The town classified the $200,000 balance of the current year levy as delinquent (an amount to be recognized as deferred revenue) This email is labeled document number 201. Record the transactions in the General Journal template in the Excel Project file. Transaction 1 Let us start with transaction 1 from the email... What will the journal entry look like for property taxes of $15,000,000 being levied for the general fund? (Since none of these transactions are expenditures, a department code of 000 has been entered for you.) Entry for property tax levy Dr. Account #105 Fund #101, Department #000, Amount $15.000.000 Cr. Account #239. Fund #101, Department #000, Amount $15.000.000 Record the journal entry in the Excele template for project 2 for the property tax levy, but do not post the entry yet. (We'll post when we have entered all the transactions.) Transaction 2 For transaction 2 from the email, the transaction will be split into two parts. The first part of this transaction is the bank deposit. . Enter the journal entry for the bank deposit in the Cash Receipts Journal. For this bank deposit: The credit account will be account number 106 - Delinquent Property Taxes Receivable. Remember that this is a General Fund transaction (Fund #101), and is revenue related, so Department w000 has been entered for you. . At this point, we have accounted for the credit to the receivables account. Next, we need to account for the debit to the deferred property tax revenue account and the credit to the property tax revenue account. What will this journal entry look like? Entry for collection of delinquent property tax revenues Dr. Account # 239. Fund# 101. Department #000. Amount $80.000 Cr. Account # 301. Fund #101, Department #000, Amount $80.000 Record the journal entry in the Excel project file. Transaction 3 Transaction 3 will be handled in the same manner as transaction 2 from the email. The first part of this transaction is a bank deposit which will be credited to property taxes receivable (Account #105). The second part of the transaction is similar to the entry above for transaction 2. The only difference is the amount. Record the journal entry in the Excel project file. Entry for Collection of Current Property Tax Revenues Dr. Account # 239, Fund #101, Department #000. Amount $14.000.000 Cr. Account #301, Fund #101. Department #000, Amount $14.000.000, Transaction 4 For transaction 4 from the email, we are assuming that during the 60 days following the end of the 2016 year, $800,000 was collected related to the 2016 tax levy. Since the cash was not received during the 2016 year, there is no cash deposit to record. The only action taken now is to create a journal entry to account for this. The entry will be the same as the journal entries for transactions 2 and 3, except the amount. Entry for collection of property tax collected in 60 days following year-end Dr. Account # 239, Fund #101, Department #000, Amount $800,000 Cr. Account # 301, Fund # 101, Department #000, Amount $800.000 Transaction 5 In the final transaction in the email, transaction 5, we are made aware that the uncollected balance of the current year levy is to be classified as delinquent. This amount is currently in the Property Taxes Receivable Account and needs to be moved to the Property Taxes Receivable - Delinquent account. Record the journal entry that is required in the Excel project file. Entry for Property Taxes not collected in the current year Dr. Account # 106, Fund # 101, Department #000, Amount $200,000 Cr. Account # 105, Fund # 101, Department #000, Amount $200,000 Other Revenue-Related Transactions You receive a second email from the Comptroller related to revenue received by the Town of Oakville. Record the transaction in the email that follows in in the Excel project file. Other Revenue Related Transactions through February To: Junior Accounting Staff From: Comptroller of the Town of Oakville The following amounts were received into the Town of Oakville bank account: Sales Tax Revenue $2,350,000 Fines Revenue 110,000 Licenses and Permits Revenue 45,000 In addition, a cash grant of $350,000 was awarded to the Town of Oakville to train law enforcement officers. This cash was received into the bank account. This email is labeled document number 202. Note: All of the transactions in the email, except the grant awarded to train law enforcement, belong in the General Fund. The first entry should contain the following components: Entry for Other Revenue amounts collected Dr. Account # 101 Fund # 101 Department #000, Amount $2.855.000 Cr. Account # 310, Fund # 101, Department #000, Amount $2.350.000 Cr. Account # 315, Fun 101, Department #000, Amount $110,000 Cr. Account # 320, Fund # 101, Department #000. Amount $45.000 Cr. Account # 132. Fund #205, Department #000, Amount $350.000 Note: Be attentive to the fact that the last $350,000 amount does not belong in the General Fund; instead it belongs in the Special Revenue fund for an enforcement grant. You will need to make a separate entry for the grant. Posting Post the transactions in the general ledger in the Excel project file. Project Two Deliverable Upon completion of the Project Two, you will deliver the following document: 1. Last name, First name P2-1 General Journal

![For Mowen/hansen/heitgers Cornerstones Of Managerial Accounting, 6th Edition, [instant Access]](https://dsd5zvtm8ll6.cloudfront.net/si.question.images/book_images/2022/04/6257c87e3025b_1256257c87dcfa77.jpg)