Question

Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes. For each item below, indicate

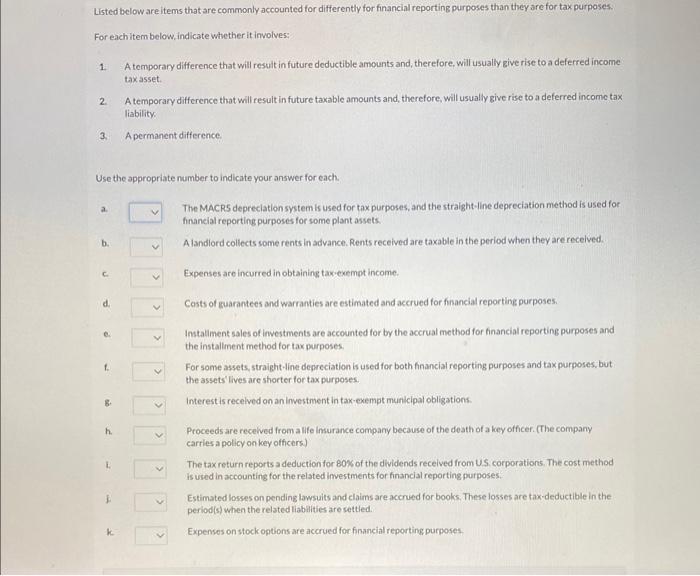

Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.

For each item below, indicate whether it involves:

1. A temporary difference that will result in future deductible amounts and, therefore, will usually give rise to a deferred income tax asset.

2. A temporary difference that will result in future taxable amounts and, therefore, will usually give rise to a deferred income tax

liability.

3. A permanent difference.

Use the appropriate number to indicate your answer for each.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting For Management

Authors: N Ramachandran

3rd Edition

1259004694, 978-1259004698