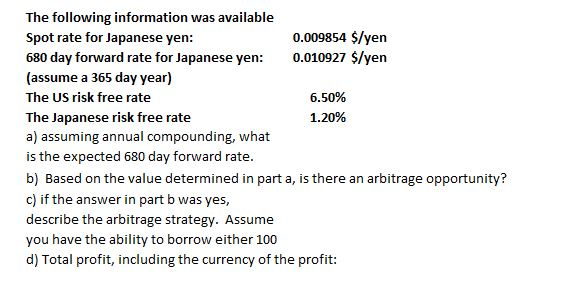

Question

Looking for some final help on this HW question I have...really stuck on this one! Any help I could get would be great!! If you

Looking for some final help on this HW question I have...really stuck on this one! Any help I could get would be great!!

If you can please show your steps. i am trying to study for a test, and want to understand how the problem works, and not just the answer.

BIG THUMBS UP to who can help!!!

Thank you!!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Social Media Handbook For Financial Advisors

Authors: Matthew Halloran

1st Edition

1118208013, 978-1118208014