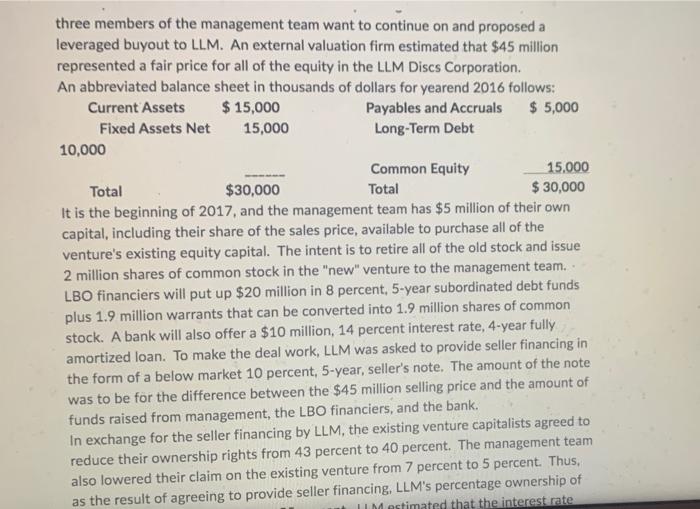

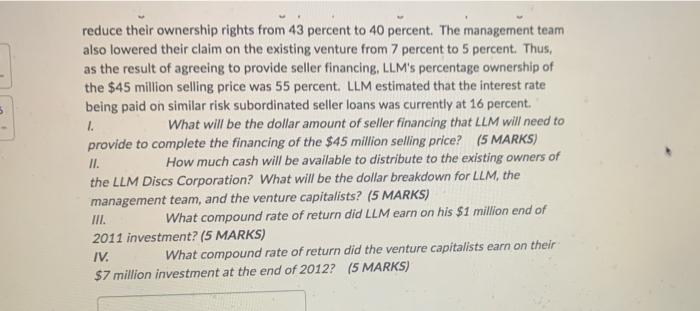

Lucas, Lucas & Matt (LLM) founded the LLM Discs Corporation at the end of 2021. After nearly one year of development, the venture produced an optical storage disk about the size of a silver dollar that could store more than 500 megabytes of data along with a mechanism allowing the device to be integrated into a variety of portable consumer electronic devices including e-books, music discs, and video games. In addition to LLM role as the venture's CEO's, Casandra Sharpe, with 6 years of prior financial management experience at two high technology ventures, was hired as the CFO. The Vice-President of Marketing was Joshua Davis and the Vice-President of Operations was Agam Chavarti. Before being hired by LLM, Davis had 12 years of marketing experience in the technology area. Chavarti worked in high tech operations for eight years before pursuing the opportunity with LLM. Leading electronic manufacturers were anxious to incorporate the LLM disk in their products. LLM obtained $7 million financing at the end of 2012 from venture investors in exchange for 43 percent of the stock in the venture. After this round of venture financing, LLM retained 50 percent ownership in LLM Discs and the other three members of the management team (Sharpe, Davis, and Chavarti) owned 7 percent of the venture. Over a four-year period (2013-2016), LLM Discs moved quickly through its start-up and survival stages and is now in the midst of its rapid growth stage. LLM has recently decided to harvest their investment by selling the firm. However, the other three members of the management team want to continue on and proposed a leveraged buyout to LLM. An external valuation firm estimated that $45 million Mircea three members of the management team want to continue on and proposed a leveraged buyout to LL.M. An external valuation firm estimated that $45 million represented a fair price for all of the equity in the LLM Discs Corporation An abbreviated balance sheet in thousands of dollars for yearend 2016 follows: Current Assets $ 15,000 Payables and Accruals $ 5,000 Fixed Assets Net 15,000 Long-Term Debt 10,000 Common Equity 15,000 Total $30,000 Total $ 30,000 It is the beginning of 2017, and the management team has $5 million of their own capital, including their share of the sales price, available to purchase all of the venture's existing equity capital. The intent is to retire all of the old stock and issue 2 million shares of common stock in the "new" venture to the management team. LBO financiers will put up $20 million in 8 percent, 5-year subordinated debt funds plus 1.9 million warrants that can be converted into 1.9 million shares of common stock. A bank will also offer a $10 million, 14 percent interest rate, 4-year fully amortized loan. To make the deal work, LLM was asked to provide seller financing in the form of a below market 10 percent, 5-year, seller's note. The amount of the note was to be for the difference between the $45 million selling price and the amount of funds raised from management, the LBO financiers, and the bank. In exchange for the seller financing by LLM, the existing venture capitalists agreed to reduce their ownership rights from 43 percent to 40 percent. The management team also lowered their claim on the existing venture from 7 percent to 5 percent. Thus, as the result of agreeing to provide seller financing, LLM's percentage ownership of IM estimated that the interest rate reduce their ownership rights from 43 percent to 40 percent. The management team also lowered their claim on the existing venture from 7 percent to 5 percent. Thus, as the result of agreeing to provide seller financing, LLM's percentage ownership of the $45 million selling price was 55 percent. LLM estimated that the interest rate being paid on similar risk subordinated seller loans was currently at 16 percent. 1. What will be the dollar amount of seller financing that LLM will need to provide to complete the financing of the $45 million selling price? (5 MARKS) II. How much cash will be available to distribute to the existing owners of the LLM Discs Corporation? What will be the dollar breakdown for LLM, the management team, and the venture capitalists? (5 MARKS) III. What compound rate of return did LLM earn on his $1 million end of 2011 investment? (5 MARKS) IV. What compound rate of return did the venture capitalists earn on their $7 million investment at the end of 2012? (5 MARKS) Lucas, Lucas & Matt (LLM) founded the LLM Discs Corporation at the end of 2021. After nearly one year of development, the venture produced an optical storage disk about the size of a silver dollar that could store more than 500 megabytes of data along with a mechanism allowing the device to be integrated into a variety of portable consumer electronic devices including e-books, music discs, and video games. In addition to LLM role as the venture's CEO's, Casandra Sharpe, with 6 years of prior financial management experience at two high technology ventures, was hired as the CFO. The Vice-President of Marketing was Joshua Davis and the Vice-President of Operations was Agam Chavarti. Before being hired by LLM, Davis had 12 years of marketing experience in the technology area. Chavarti worked in high tech operations for eight years before pursuing the opportunity with LLM. Leading electronic manufacturers were anxious to incorporate the LLM disk in their products. LLM obtained $7 million financing at the end of 2012 from venture investors in exchange for 43 percent of the stock in the venture. After this round of venture financing, LLM retained 50 percent ownership in LLM Discs and the other three members of the management team (Sharpe, Davis, and Chavarti) owned 7 percent of the venture. Over a four-year period (2013-2016), LLM Discs moved quickly through its start-up and survival stages and is now in the midst of its rapid growth stage. LLM has recently decided to harvest their investment by selling the firm. However, the other three members of the management team want to continue on and proposed a leveraged buyout to LLM. An external valuation firm estimated that $45 million Mircea three members of the management team want to continue on and proposed a leveraged buyout to LL.M. An external valuation firm estimated that $45 million represented a fair price for all of the equity in the LLM Discs Corporation An abbreviated balance sheet in thousands of dollars for yearend 2016 follows: Current Assets $ 15,000 Payables and Accruals $ 5,000 Fixed Assets Net 15,000 Long-Term Debt 10,000 Common Equity 15,000 Total $30,000 Total $ 30,000 It is the beginning of 2017, and the management team has $5 million of their own capital, including their share of the sales price, available to purchase all of the venture's existing equity capital. The intent is to retire all of the old stock and issue 2 million shares of common stock in the "new" venture to the management team. LBO financiers will put up $20 million in 8 percent, 5-year subordinated debt funds plus 1.9 million warrants that can be converted into 1.9 million shares of common stock. A bank will also offer a $10 million, 14 percent interest rate, 4-year fully amortized loan. To make the deal work, LLM was asked to provide seller financing in the form of a below market 10 percent, 5-year, seller's note. The amount of the note was to be for the difference between the $45 million selling price and the amount of funds raised from management, the LBO financiers, and the bank. In exchange for the seller financing by LLM, the existing venture capitalists agreed to reduce their ownership rights from 43 percent to 40 percent. The management team also lowered their claim on the existing venture from 7 percent to 5 percent. Thus, as the result of agreeing to provide seller financing, LLM's percentage ownership of IM estimated that the interest rate reduce their ownership rights from 43 percent to 40 percent. The management team also lowered their claim on the existing venture from 7 percent to 5 percent. Thus, as the result of agreeing to provide seller financing, LLM's percentage ownership of the $45 million selling price was 55 percent. LLM estimated that the interest rate being paid on similar risk subordinated seller loans was currently at 16 percent. 1. What will be the dollar amount of seller financing that LLM will need to provide to complete the financing of the $45 million selling price? (5 MARKS) II. How much cash will be available to distribute to the existing owners of the LLM Discs Corporation? What will be the dollar breakdown for LLM, the management team, and the venture capitalists? (5 MARKS) III. What compound rate of return did LLM earn on his $1 million end of 2011 investment? (5 MARKS) IV. What compound rate of return did the venture capitalists earn on their $7 million investment at the end of 2012