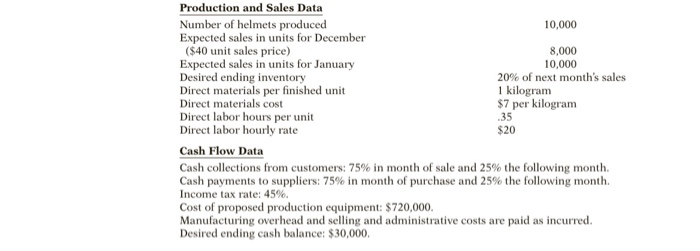

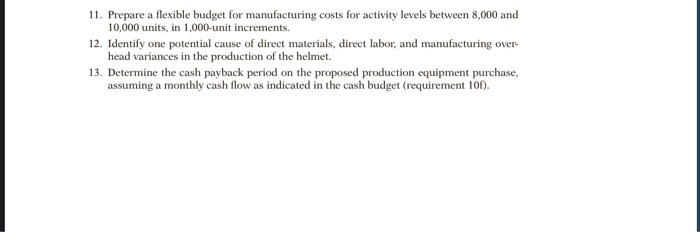

MAET COM SW NEN Armstrong Helmet Company Developed by Dick Wasson, Southwester College The Business Situation Armstrong Helmet Company manufactures a unique model of bicycle helmet. The company began operations December 1, 2013. Its accountant quit the second week of operations, and the company is searching for a replacement. The com- pany has decided to test the knowledge and ability of all candidates interviewing for the position. Each candidate will be provided with the information below and then asked to prepare a series of reports, schedules, budgets, and recommenda- tions based on that information. The information provided to each candidate is as follows: Cost Items and Account Balances Administrative salaries $15.500 Advertising for helmets 11.000 Cash, December 1 Depreciation on factory building 1.500 Depreciation on office equipment 800 Insurance on factory building 1.500 Miscellaneous expenses-factory 1.000 Office supplies expense 300 Professional fees 500 Property taxes on factory building Raw materials used 70,000 Rent on production equipment 6.000 Research and development 10,000 Sales commissions 40.000 Utility costs-factory 900 Wages-factory 70,000 Work in process, December 1 Work in process, December 31 -0- Raw materials inventory, December 1 Raw materials inventory, December 31 Raw material purchases 70,000 Finished goods inventory, December 1 100 Production and Sales Data Number of helmets produced 10,000 Expected sales in units for December ($40 unit sales price) 8,000 Expected sales in units for January 10,000 Desired ending inventory 20% of next month's sales Direct materials per finished unit 1 kilogram Direct materials cost $7 per kilogram Direct labor hours per unit Direct labor hourly rate $20 Cash Flow Data Cash collections from customers: 75% in month of sale and 25% the following month Cash payments to suppliers: 75% in month of purchase and 25% the following month. Income tax rate: 45%. Cost of proposed production equipment: $720,000. Manufacturing overhead and selling and administrative costs are paid as incurred. Desired ending cash balance: $30,000, .35 11. Prepare a flexible budget for manufacturing costs for activity levels between 8,000 and 10,000 units, in 1,000-unit increments. 12. Identify one potential cause of direct materials, direct labor, and manufacturing over head variances in the production of the helmet. 13. Determine the cash payback period on the proposed production equipment purchase, assuming a monthly cash flow as indicated in the cash budget (requirement 101). MAET COM SW NEN Armstrong Helmet Company Developed by Dick Wasson, Southwester College The Business Situation Armstrong Helmet Company manufactures a unique model of bicycle helmet. The company began operations December 1, 2013. Its accountant quit the second week of operations, and the company is searching for a replacement. The com- pany has decided to test the knowledge and ability of all candidates interviewing for the position. Each candidate will be provided with the information below and then asked to prepare a series of reports, schedules, budgets, and recommenda- tions based on that information. The information provided to each candidate is as follows: Cost Items and Account Balances Administrative salaries $15.500 Advertising for helmets 11.000 Cash, December 1 Depreciation on factory building 1.500 Depreciation on office equipment 800 Insurance on factory building 1.500 Miscellaneous expenses-factory 1.000 Office supplies expense 300 Professional fees 500 Property taxes on factory building Raw materials used 70,000 Rent on production equipment 6.000 Research and development 10,000 Sales commissions 40.000 Utility costs-factory 900 Wages-factory 70,000 Work in process, December 1 Work in process, December 31 -0- Raw materials inventory, December 1 Raw materials inventory, December 31 Raw material purchases 70,000 Finished goods inventory, December 1 100 Production and Sales Data Number of helmets produced 10,000 Expected sales in units for December ($40 unit sales price) 8,000 Expected sales in units for January 10,000 Desired ending inventory 20% of next month's sales Direct materials per finished unit 1 kilogram Direct materials cost $7 per kilogram Direct labor hours per unit Direct labor hourly rate $20 Cash Flow Data Cash collections from customers: 75% in month of sale and 25% the following month Cash payments to suppliers: 75% in month of purchase and 25% the following month. Income tax rate: 45%. Cost of proposed production equipment: $720,000. Manufacturing overhead and selling and administrative costs are paid as incurred. Desired ending cash balance: $30,000, .35 11. Prepare a flexible budget for manufacturing costs for activity levels between 8,000 and 10,000 units, in 1,000-unit increments. 12. Identify one potential cause of direct materials, direct labor, and manufacturing over head variances in the production of the helmet. 13. Determine the cash payback period on the proposed production equipment purchase, assuming a monthly cash flow as indicated in the cash budget (requirement 101)