Answered step by step

Verified Expert Solution

Question

1 Approved Answer

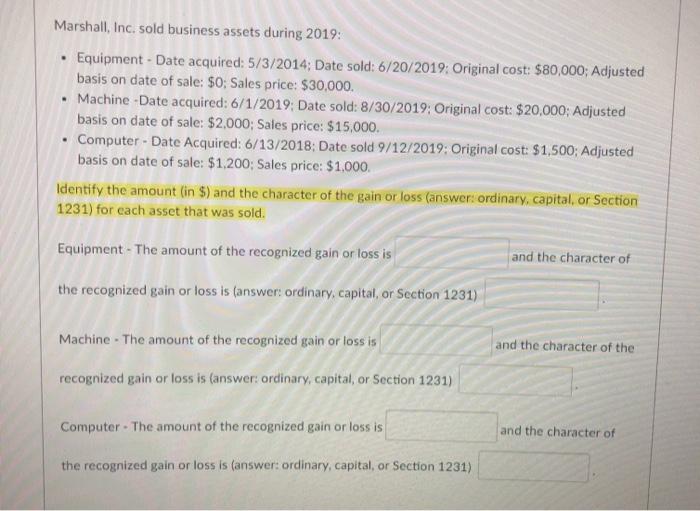

Marshall, Inc. sold business assets during 2019: Equipment - Date acquired: 5/3/2014: Date sold: 6/20/2019: Original cost: $80,000; Adjusted basis on date of sale: $0;

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Donald E. Kieso, Jerry J. Weygandt, and Terry D. Warfield

15th edition

978-1118159644, 9781118562185, 1118159640, 1118147294, 978-1118147290