Answered step by step

Verified Expert Solution

Question

1 Approved Answer

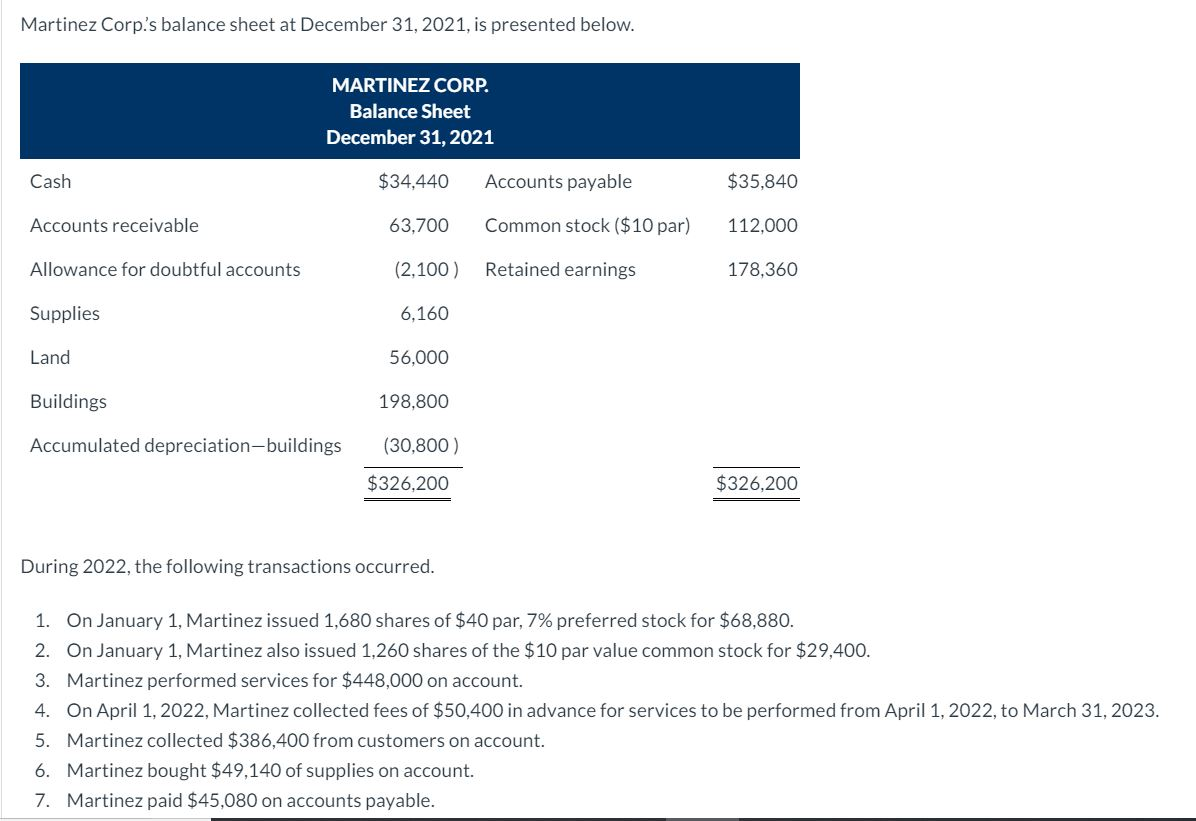

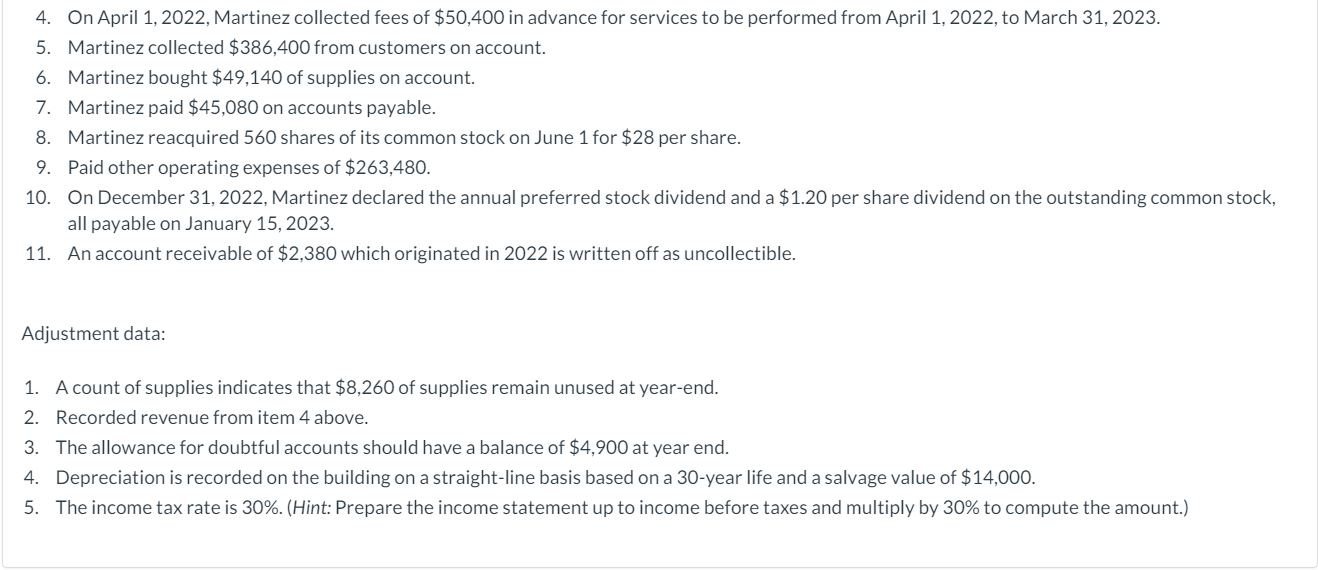

Martinez Corp.'s balance sheet at December 31, 2021, is presented below. MARTINEZ CORP. Balance Sheet December 31, 2021 Cash $34,440 Accounts payable $35,840 Accounts receivable

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Purchasing Audit

Authors: ISMAIL LAMHAMDI

1st Edition

6203507563, 978-6203507560