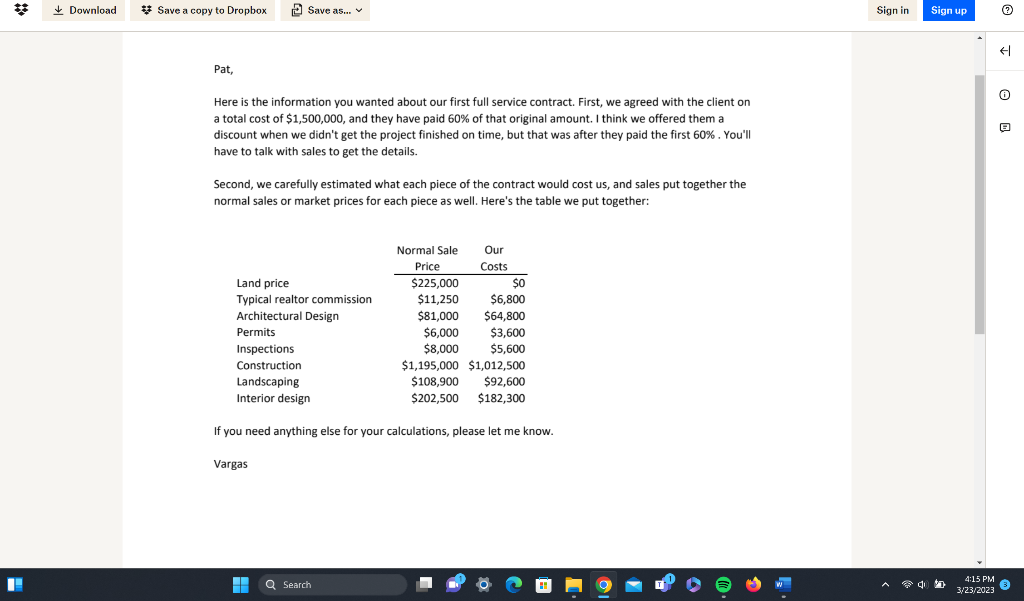

"Maybe because we haven't actually delivered the final home to the client?" "Yeah, I do. My read of GAAP suggests that we have to fully complete an obligation, and in this case I think that means the house being ready to go for the client. We can't just be done with Vargas waived a hand dismissively. "Whatever. That's just a technicality. We've delivered what we normally do and have a contract in place. We've agreed, in the contract, to provide a everything we promised. Our obligation is done." house that is completely finished, including the landscaping and the interior design. Those pieces Pat started to disagree, but Vargas continued. "Don't lecture me about it. I know FASB has laid aren't done, so the obligation isn't complete and we can't recognize the revenue." out some specific rules. I don't agree with their logic, but that's nothing new. There are several Pat nodded. "Makes sense. You think we need to wait on the whole project, then?" places in GAAP that I disagree with. The important thing now is that we figure out a way to recognize the revenue on not only the current project, but on all future projects. I don't ever want Sam shook a hand back and forth, indicating maybe. "I don't know about that. I strongly believe to have to stop and argue about this again. that we can't recognize all of the revenue before the house is ready for the client, but I'm not as confident that we can't recognize any of the revenue. If we meet the conditions in the ASC, then "And that's where you come in, Pat. I'm assigning you to work with the sales team to figure out maybe we can recognize some of it. I guess that's where you come in." the process for recording these full-service contracts. Use the current project as an example so that we have specific methods and numbers. Oh, and we'll need enough documentation to "Thanks a lot," Pat said sarcastically. convince the auditors that we're following GAAP. Don't forget that part." And that was the end of the meeting with Vargas. Meeting with Kansas, Sales Director "Kansas," Pat said, peeking in the Sales Director's office. "Do you have a minute?" Meeting with Sam, Head of Internal Audit "Sure, Pat," Kansas waived Pat in. "What can I help you with?" Pat sighed, but Kansas "Pat! Great to see you!" continued before Pat could say anything. "Never mind. You're here about the full-service contract, aren't you? I recognize that sigh. I hear it all the time from you accounting types when "Thanks, Sam. Its good to see you, too." we start a new project. You know, I really don't know how you guys manage to deal with this "So, what brings you to the basement?" Sam laughed. financial stuff. all the time. It would drive me nuts!" "I just finished a breakfast meeting with Vargas..." Pat nodded. "I'm feeling a bit of that myself at the moment. Anyway, can I ask you a few questions?" "On the full-service thing." "Sure. What do you need to know?" "Yup. Can you get me up to speed a bit more?" "I need to know more about the contract we have with the client." Kansas nodded for Pat to "Sure. Do you remember the basic rules for the new revenue recognition process?" continue. "First, is the contract going to change for each client? And second, what exactly do we promise to do for the client?" Pat nodded. "I think so. We can't recognize revenue until we complete the deliverables, right?" Kansas took a deep breath while looking at the window, nodding slightly as the details came "Performance obligations, actually, but that's close enough. There are some situations where you back. "Let's start with the contract. The specific terms will change, but not the main details. can recognize revenue mid-obligation, but as you said, the big issue is making sure that revenue matches up with specific obligations and then recognizing the revenue as each obligation to the More specifically, what we have promised to provide won't change. We are going to provide a home to the client that is fully designed, built, decoratated and landscaped for an agreed upon client is completed." price. However, the client can change the colors, location, number of bedrooms, etc., which will "And you disagree with Wei's interpretation for the full-service contract?" in turn change the exact price. We set up the basics to be consistent on purpose so that we wouldn't have to keep paying lawyers to set up specific contracts." Pat nodded. "It will also save us a bunch of hassle in accounting, since that means we can set up end. Oh, and we've collected some of the cash from the client." one system for recognizing the revenue." "If you say so. I just wanted to minimize the need to work with lawyers." Meeting with Riley, Project Manager Pat laughed. "So, what exactly do we agree to provide?" "Pat, I figured I'd be seeing you sometime today." "Well, subject to the preferences of the clients, we promise to provide the following: "Hey, Riley. Sorry to interrupt you on the job." They were standing off to the side of a construction project, under a tree that provided a little shade. 1. Help finding and purchasing a piece of land in a location the client is comfortable with. 2. An approved architectural design for a home on that piece of land. "That's okay. I understand that paperwork has to be done, and Kansas called me to let me know 3. Construction of the home on that piece of land, following the architectural design. This includes you were coming. I think I'm ready." He pulled out his phone and tapped a button. "There you all of the necessary permits and inspections required by the municipality where the land is located. go. That's my spreadsheet from the project. It includes everything we spent and the market 4. Appropriate landscaping and interior decoration of the house." estimates we gathered for everything." "Do we actually purchase the land for them?" Pat asked. "Thanks," Pat's phone buzzed as the message arrived. "But why didn't you just send this to me and save me the drive out here?" "No. We act as their real estate agent, essentially, but they buy the property." Riley smiled. "So you could see the actual job site." Riley gestured around at the groups of Pat nodded. "Okay, and what did we agree on with this first contract?" workers. "You need to know that everything in this process flows together. Once the land is purchased and we have the design and initial permits, we jump right in with the construction. Kansas shuffled through some papers. "We helped them secure land in Neskowin, OR and built a With this project, we're just waiting for the inspector to verify that the construction is up to code. 4 bedroom, 3 bath house." Over there is the landscaping crew. They're not really one of my teams; we hired a subcontractor "Which isn't done yet." to do the work, but they have been working on the yard while we have been working on the house. The landscapers couldn't finish their work until the construction was done and our "Oh, the house is done and ready for its final inspection, but the landscaping is still going in. We equipment moved out of way, but they are moving fairly quickly now now." Riley turned around, have a subcontractor from the area taking care of that." then gestured again. "And that's the decorator there on the sidewalk. We make sure that their "What about the decorating?" Pat asked. team can see what we are doing every step of the way so that the owner doesn't have to wait for them to do their design after we are done. Now that the construction is finished, they can come in "The design is done, as is our part. The designer still needs to finish buying the furniture, then and finish decorating the home, choosing furniture, and so on. It's all an integrated process, and I once the landscaping is done they will clean the house from top to bottom and will place figured you needed to know that before you start your work." everything. That's it." Pat nodded. "You're right. That's really.good to know." Pat watched for a few minutes, then "Good. I think I only need one more thing." shook Riley's hand. "I'll let you get back to it." "Just one?" Kansas asked in mock surprised. "Are you sure?" Riley smiled. "Oh, I don't work here. I have four other job sites to check out. I'm the project manager, not a foreman." Pat frowned, but went on. "I just need to know what the costs were for each part of the project and the market values for the services we rendered." "My apologies," Pat said. "I guess I don't even really know what you do." "That's not me, I'm afraid," Kansas replied. "You'll need to talk with Riley, the project manager. "Don't worry about it. You'll get there." All I can tell you is that we offered a 3\% discount if we didn't get the project finished by year 8 Getting to work Pat leaned back and looked at the notes all over the desk. It had been a busy couple of days, but finally Pat understood the process for these new full-service construction contracts and could get to work figuring out how the company should recognize revenue. That was Vargas' big issue, after all. How much revenue could they recognize on this first project this year, and how will they break down revenue recognition on future full-service contracts. Pat took another look at the revenue recognition rules from ASC 606 that had been provided by their auditor at a special training, then back at the notes on the desk. I can do this, Pat thought. I just have to remember to look at it step-by-step and document each decision. Case Questions Answer all of the following questions: - Based on your understanding of PCC's processes and the revenue recognition standards in ASC 606, how many distinct obligations are included in the company's new fullservice contract? Your answer should include a breakdown of which goods or services are included in each distinct obligation bundle. - How much of the transaction price (i.e., customer price) should be allocated to each of the distinct obligations you identified in question 1 ? - How much revenue can PCC recognize in the current year on their first full-service contract? Here is the information you wanted about our first full service contract. First, we agreed with the client on a total cost of $1,500,000, and they have paid 60% of that original amount. I think we offered them a discount when we didn't get the project finished on time, but that was after they paid the first 60%. You'll have to talk with sales to get the details. Second, we carefully estimated what each piece of the contract would cost us, and sales put together the normal sales or market prices for each piece as well. Here's the table we put together: If you need anything else for your calculations, please let me know. Vargas Getting to work Pat leaned back and looked at the notes all over the desk. It had been a busy couple of days, but finally Pat understood the process for these new full-service construction contracts and could get to work figuring out how the company should recognize revenue. That was Vargas' big issue, after all. How much revenue could they recognize on this first project this year, and how will they break down revenue recognition on future full-service contracts. Pat took another look at the revenue recognition rules from ASC 606 that had been provided by their auditor at a special training, then back at the notes on the desk. I can do this, Pat thought. I just have to remember to look at it step-by-step and document each decision. Case Questions Answer all of the following questions: - Based on your understanding of PCC's processes and the revenue recognition standards in ASC 606, how many distinct obligations are included in the company's new fullservice contract? Your answer should include a breakdown of which goods or services are included in each distinct obligation bundle. - How much of the transaction price (i.e., customer price) should be allocated to each of the distinct obligations you identified in question 1 ? - How much revenue can PCC recognize in the current year on their first full-service contract? "Maybe because we haven't actually delivered the final home to the client?" "Yeah, I do. My read of GAAP suggests that we have to fully complete an obligation, and in this case I think that means the house being ready to go for the client. We can't just be done with Vargas waived a hand dismissively. "Whatever. That's just a technicality. We've delivered what we normally do and have a contract in place. We've agreed, in the contract, to provide a everything we promised. Our obligation is done." house that is completely finished, including the landscaping and the interior design. Those pieces Pat started to disagree, but Vargas continued. "Don't lecture me about it. I know FASB has laid aren't done, so the obligation isn't complete and we can't recognize the revenue." out some specific rules. I don't agree with their logic, but that's nothing new. There are several Pat nodded. "Makes sense. You think we need to wait on the whole project, then?" places in GAAP that I disagree with. The important thing now is that we figure out a way to recognize the revenue on not only the current project, but on all future projects. I don't ever want Sam shook a hand back and forth, indicating maybe. "I don't know about that. I strongly believe to have to stop and argue about this again. that we can't recognize all of the revenue before the house is ready for the client, but I'm not as confident that we can't recognize any of the revenue. If we meet the conditions in the ASC, then "And that's where you come in, Pat. I'm assigning you to work with the sales team to figure out maybe we can recognize some of it. I guess that's where you come in." the process for recording these full-service contracts. Use the current project as an example so that we have specific methods and numbers. Oh, and we'll need enough documentation to "Thanks a lot," Pat said sarcastically. convince the auditors that we're following GAAP. Don't forget that part." And that was the end of the meeting with Vargas. Meeting with Kansas, Sales Director "Kansas," Pat said, peeking in the Sales Director's office. "Do you have a minute?" Meeting with Sam, Head of Internal Audit "Sure, Pat," Kansas waived Pat in. "What can I help you with?" Pat sighed, but Kansas "Pat! Great to see you!" continued before Pat could say anything. "Never mind. You're here about the full-service contract, aren't you? I recognize that sigh. I hear it all the time from you accounting types when "Thanks, Sam. Its good to see you, too." we start a new project. You know, I really don't know how you guys manage to deal with this "So, what brings you to the basement?" Sam laughed. financial stuff. all the time. It would drive me nuts!" "I just finished a breakfast meeting with Vargas..." Pat nodded. "I'm feeling a bit of that myself at the moment. Anyway, can I ask you a few questions?" "On the full-service thing." "Sure. What do you need to know?" "Yup. Can you get me up to speed a bit more?" "I need to know more about the contract we have with the client." Kansas nodded for Pat to "Sure. Do you remember the basic rules for the new revenue recognition process?" continue. "First, is the contract going to change for each client? And second, what exactly do we promise to do for the client?" Pat nodded. "I think so. We can't recognize revenue until we complete the deliverables, right?" Kansas took a deep breath while looking at the window, nodding slightly as the details came "Performance obligations, actually, but that's close enough. There are some situations where you back. "Let's start with the contract. The specific terms will change, but not the main details. can recognize revenue mid-obligation, but as you said, the big issue is making sure that revenue matches up with specific obligations and then recognizing the revenue as each obligation to the More specifically, what we have promised to provide won't change. We are going to provide a home to the client that is fully designed, built, decoratated and landscaped for an agreed upon client is completed." price. However, the client can change the colors, location, number of bedrooms, etc., which will "And you disagree with Wei's interpretation for the full-service contract?" in turn change the exact price. We set up the basics to be consistent on purpose so that we wouldn't have to keep paying lawyers to set up specific contracts." Pat nodded. "It will also save us a bunch of hassle in accounting, since that means we can set up end. Oh, and we've collected some of the cash from the client." one system for recognizing the revenue." "If you say so. I just wanted to minimize the need to work with lawyers." Meeting with Riley, Project Manager Pat laughed. "So, what exactly do we agree to provide?" "Pat, I figured I'd be seeing you sometime today." "Well, subject to the preferences of the clients, we promise to provide the following: "Hey, Riley. Sorry to interrupt you on the job." They were standing off to the side of a construction project, under a tree that provided a little shade. 1. Help finding and purchasing a piece of land in a location the client is comfortable with. 2. An approved architectural design for a home on that piece of land. "That's okay. I understand that paperwork has to be done, and Kansas called me to let me know 3. Construction of the home on that piece of land, following the architectural design. This includes you were coming. I think I'm ready." He pulled out his phone and tapped a button. "There you all of the necessary permits and inspections required by the municipality where the land is located. go. That's my spreadsheet from the project. It includes everything we spent and the market 4. Appropriate landscaping and interior decoration of the house." estimates we gathered for everything." "Do we actually purchase the land for them?" Pat asked. "Thanks," Pat's phone buzzed as the message arrived. "But why didn't you just send this to me and save me the drive out here?" "No. We act as their real estate agent, essentially, but they buy the property." Riley smiled. "So you could see the actual job site." Riley gestured around at the groups of Pat nodded. "Okay, and what did we agree on with this first contract?" workers. "You need to know that everything in this process flows together. Once the land is purchased and we have the design and initial permits, we jump right in with the construction. Kansas shuffled through some papers. "We helped them secure land in Neskowin, OR and built a With this project, we're just waiting for the inspector to verify that the construction is up to code. 4 bedroom, 3 bath house." Over there is the landscaping crew. They're not really one of my teams; we hired a subcontractor "Which isn't done yet." to do the work, but they have been working on the yard while we have been working on the house. The landscapers couldn't finish their work until the construction was done and our "Oh, the house is done and ready for its final inspection, but the landscaping is still going in. We equipment moved out of way, but they are moving fairly quickly now now." Riley turned around, have a subcontractor from the area taking care of that." then gestured again. "And that's the decorator there on the sidewalk. We make sure that their "What about the decorating?" Pat asked. team can see what we are doing every step of the way so that the owner doesn't have to wait for them to do their design after we are done. Now that the construction is finished, they can come in "The design is done, as is our part. The designer still needs to finish buying the furniture, then and finish decorating the home, choosing furniture, and so on. It's all an integrated process, and I once the landscaping is done they will clean the house from top to bottom and will place figured you needed to know that before you start your work." everything. That's it." Pat nodded. "You're right. That's really.good to know." Pat watched for a few minutes, then "Good. I think I only need one more thing." shook Riley's hand. "I'll let you get back to it." "Just one?" Kansas asked in mock surprised. "Are you sure?" Riley smiled. "Oh, I don't work here. I have four other job sites to check out. I'm the project manager, not a foreman." Pat frowned, but went on. "I just need to know what the costs were for each part of the project and the market values for the services we rendered." "My apologies," Pat said. "I guess I don't even really know what you do." "That's not me, I'm afraid," Kansas replied. "You'll need to talk with Riley, the project manager. "Don't worry about it. You'll get there." All I can tell you is that we offered a 3\% discount if we didn't get the project finished by year 8 Getting to work Pat leaned back and looked at the notes all over the desk. It had been a busy couple of days, but finally Pat understood the process for these new full-service construction contracts and could get to work figuring out how the company should recognize revenue. That was Vargas' big issue, after all. How much revenue could they recognize on this first project this year, and how will they break down revenue recognition on future full-service contracts. Pat took another look at the revenue recognition rules from ASC 606 that had been provided by their auditor at a special training, then back at the notes on the desk. I can do this, Pat thought. I just have to remember to look at it step-by-step and document each decision. Case Questions Answer all of the following questions: - Based on your understanding of PCC's processes and the revenue recognition standards in ASC 606, how many distinct obligations are included in the company's new fullservice contract? Your answer should include a breakdown of which goods or services are included in each distinct obligation bundle. - How much of the transaction price (i.e., customer price) should be allocated to each of the distinct obligations you identified in question 1 ? - How much revenue can PCC recognize in the current year on their first full-service contract? Here is the information you wanted about our first full service contract. First, we agreed with the client on a total cost of $1,500,000, and they have paid 60% of that original amount. I think we offered them a discount when we didn't get the project finished on time, but that was after they paid the first 60%. You'll have to talk with sales to get the details. Second, we carefully estimated what each piece of the contract would cost us, and sales put together the normal sales or market prices for each piece as well. Here's the table we put together: If you need anything else for your calculations, please let me know. Vargas Getting to work Pat leaned back and looked at the notes all over the desk. It had been a busy couple of days, but finally Pat understood the process for these new full-service construction contracts and could get to work figuring out how the company should recognize revenue. That was Vargas' big issue, after all. How much revenue could they recognize on this first project this year, and how will they break down revenue recognition on future full-service contracts. Pat took another look at the revenue recognition rules from ASC 606 that had been provided by their auditor at a special training, then back at the notes on the desk. I can do this, Pat thought. I just have to remember to look at it step-by-step and document each decision. Case Questions Answer all of the following questions: - Based on your understanding of PCC's processes and the revenue recognition standards in ASC 606, how many distinct obligations are included in the company's new fullservice contract? Your answer should include a breakdown of which goods or services are included in each distinct obligation bundle. - How much of the transaction price (i.e., customer price) should be allocated to each of the distinct obligations you identified in question 1 ? - How much revenue can PCC recognize in the current year on their first full-service contract