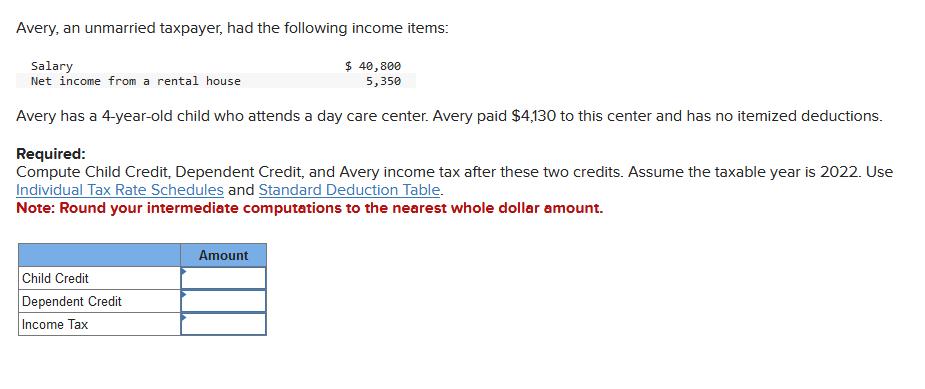

Avery, an unmarried taxpayer, had the following income items: $ 40,800 5,350 Salary Net income from a rental house Avery has a 4-year-old child

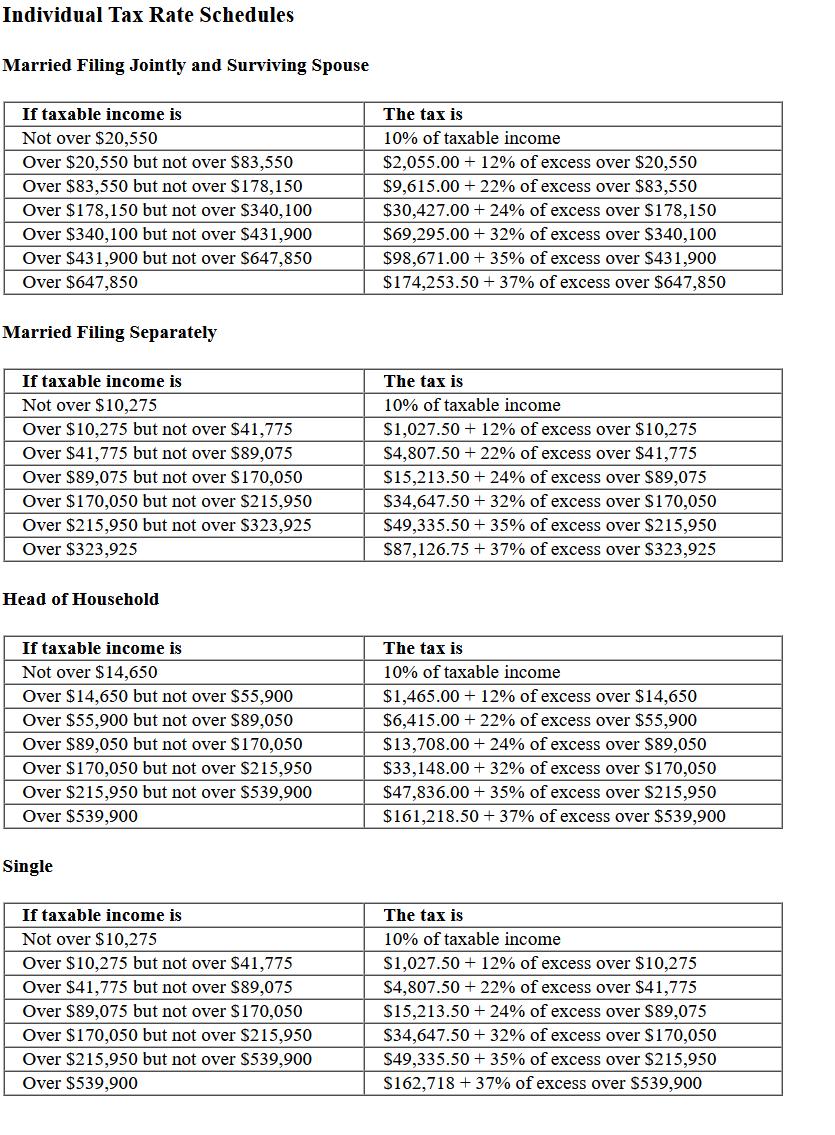

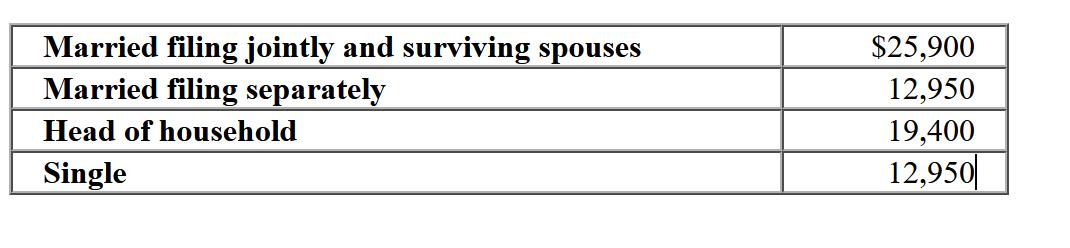

Avery, an unmarried taxpayer, had the following income items: $ 40,800 5,350 Salary Net income from a rental house Avery has a 4-year-old child who attends a day care center. Avery paid $4,130 to this center and has no itemized deductions. Required: Compute Child Credit, Dependent Credit, and Avery income tax after these two credits. Assume the taxable year is 2022. Use Individual Tax Rate Schedules and Standard Deduction Table. Note: Round your intermediate computations to the nearest whole dollar amount. Child Credit Dependent Credit Income Tax Amount Individual Tax Rate Schedules Married Filing Jointly and Surviving Spouse If taxable income is Not over $20,550 Over $20,550 but not over $83,550 Over $83,550 but not over $178,150 Over $178,150 but not over $340,100 Over $340,100 but not over $431,900 Over $431,900 but not over $647,850 Over $647,850 Married Filing Separately If taxable income is Not over $10,275 Over $10,275 but not over $41,775 Over $41,775 but not over $89,075 Over $89,075 but not over $170,050 Over $170,050 but not over $215,950 Over $215,950 but not over $323,925 Over $323,925 Head of Household If taxable income is Not over $14,650 Over $14,650 but not over $55,900 Over $55,900 but not over $89,050 Over $89,050 but not over $170,050 Over $170,050 but not over $215,950 Over $215,950 but not over $539,900 Over $539,900 Single If taxable income is Not over $10,275 Over $10,275 but not over $41,775 Over $41,775 but not over $89,075 Over $89,075 but not over $170,050 Over $170,050 but not over $215,950 Over $215,950 but not over $539,900 Over $539,900 The tax is 10% of taxable income $2,055.00 +12% of excess over $20,550 $9,615.00 +22% of excess over $83,550 $30,427.00 +24% of excess over $178,150 $69,295.00+ 32% of excess over $340,100 $98,671.00 + 35% of excess over $431,900 $174,253.50 +37% of excess over $647,850 The tax is 10% of taxable income $1,027.50 +12% of excess over $10,275 $4,807.50 +22% of excess over $41,775 $15,213.50 +24% of excess over $89,075 $34,647.50+ 32% of excess over $170,050 $49,335.50 +35% of excess over $215,950 $87,126.75 +37% of excess over $323,925 The tax is 10% of taxable income $1,465.00+12% of excess over $14,650 $6,415.00 +22% of excess over $55,900 $13,708.00 +24% of excess over $89,050 $33,148.00+ 32% of excess over $170,050 $47,836.00+ 35% of excess over $215,950 $161,218.50 +37% of excess over $539,900 The tax is 10% of taxable income $1,027.50 +12% of excess over $10,275 $4,807.50 +22% of excess over $41,775 $15,213.50 +24% of excess over $89,075 $34,647.50+32% of excess over $170,050 $49,335.50 + 35% of excess over $215,950 $162,718 +37% of excess over $539,900 Married filing jointly and surviving spouses Married filing separately Head of household Single $25,900 12,950 19,400 12,950

Step by Step Solution

3.51 Rating (175 Votes )

There are 3 Steps involved in it

Step: 1

To compute Averys child credit dependent credit and income tax after these two credits for the taxable year 2022 as an unmarried taxpayer we will foll...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Richard A. Mann, Barry S. Roberts

15th Edition

1285141903, 1285141903, 9781285141909, 978-0538473637