Answered step by step

Verified Expert Solution

Question

1 Approved Answer

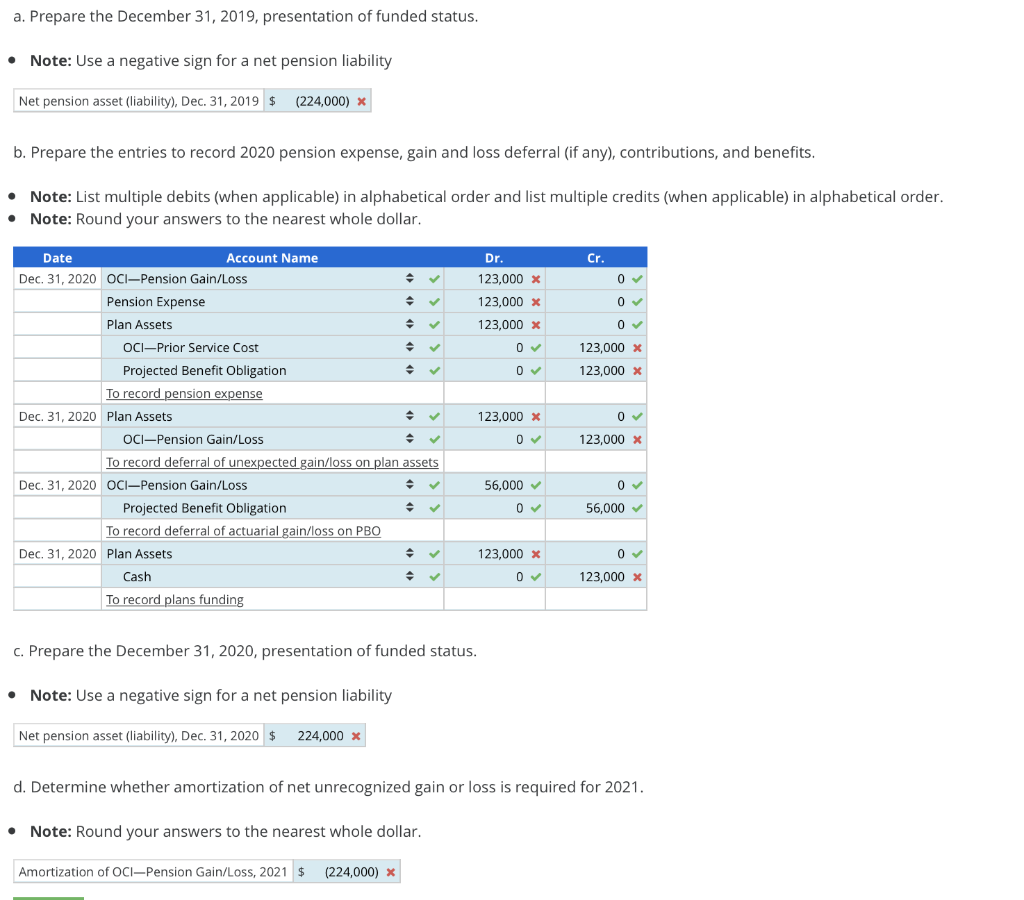

Need A, B, C and the pension gain/loss amortization on the pension worksheet. a. Prepare the December 31, 2019, presentation of funded status. Note: Use

Need A, B, C and the pension gain/loss amortization on the pension worksheet.

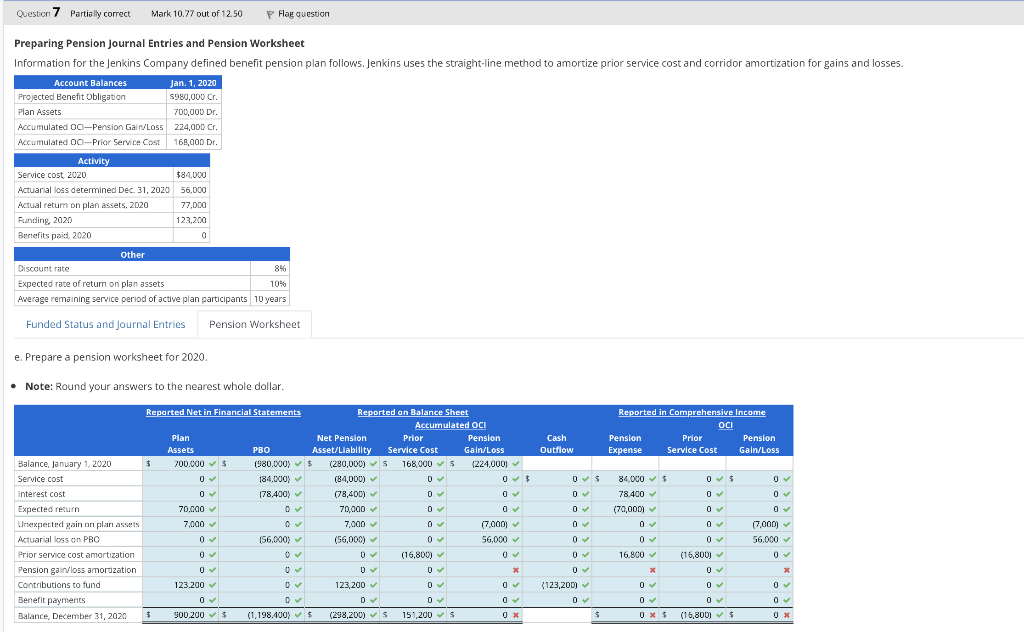

a. Prepare the December 31, 2019, presentation of funded status. Note: Use a negative sign for a net pension liability Net pension asset (liability), Dec. 31, 2019 $ (224,000) * ) b. Prepare the entries to record 2020 pension expense, gain and loss deferral (if any), contributions, and benefits. . Note: List multiple debits (when applicable) in alphabetical order and list multiple credits (when applicable) in alphabetical order. Note: Round your answers to the nearest whole dollar. . Cr. 0 0 Dr. 123,000 x 123,000 x 123,000 x 0 0 0 0 123,000 x 123,000 X 0 0 Date Account Name Dec 31, 2020 OCIPension Gain/Loss Pension Expense Plan Assets OCIPrior Service Cost Projected Benefit Obligation e To record pension expense Dec 31, 2020 Plan Assets OCI-Pension Gain/Loss To record deferral of unexpected gain/loss on plan assets Dec 31, 2020 OCIPension Gain/Loss Projected Benefit Obligation To record deferral of actuarial gain/loss on PBO Dec 31, 2020 Plan Assets Cash 123,000 X 0 0 123,000 X 0 56,000 0 0 56,000 0 123,000 x 0 123,000 X To record plans funding C. Prepare the December 31, 2020, presentation of funded status. . Note: Use a negative sign for a net pension liability Net pension asset (liability), Dec. 31, 2020 $ 224,000 * , d. Determine whether amortization of net unrecognized gain or loss is required for 2021. . Note: Round your answers to the nearest whole dollar. Amortization of OCIPension Gain/Loss, 2021 $ (224,000) Question 7 Partially correct Mark 10.77 out of 12.50 Flag question Preparing Pension Journal Entries and Pension Worksheet Information for the Jenkins Company defined benefit pension plan follows. Jenkins uses the straight-line method to amortize prior service cost and corridor amortization for gains and losses. Account Balances Jan 1, 2020 Projected Benefit obligation $980,000 Cr. Plan Assets 700,000 Dr. Accumulated OCI-Pension Gain/Loss 224,00D Cr. Accumulated OCI-Prior Service Cost 168,000 Dr. Activity Service cost, 2020 $84,000 Actuarial loss determined Dec 31, 2020 56,000 Actual return on plan assets, 2020 77,000 Funding 2020 123.200 Benefits paid, 2020 0 Other Discount rate 8% Expected rate of return on plan assets 10% % Average remaining service period of active plan participants 10 years Funded Status and Journal Entries Pension Worksheet e. Prepare a pension worksheet for 2020. a Note: Round your answers to the nearest whole dollar. Reported in Comprehensive Income OCI Pension Prior Pension Expense Service Cost Gain/Loss Cash Outflow 0$ 0$ 84,000 $ 78,400 (70,000) 0 0 0 Reported Net in Financial Statements Reported an Balance Sheet Accumulated OCI Plan Net Pension Prior Pension Assets PBO Asset/Liability Service Cost Gain/Loss $ 700.000 $ (980.000) $ (280,000) 168,000 $ 1224,000) O 184.000) (84000) 0 0$ 0 178,400) (78,400) D 70.000 70,000 0 7,000 7,000 (7,000) 0 (56,000) (56,000) 0 56,000 (16,800) 0 O D 0 123.200 123,200 0 0 D D 0 $ 900.200$ (1,198.400) (298,200) S S 151,200 $ 0* Balance, January 1, 2020 Service cost Interest cost Expected return Unexpected yain on plan assets Actuarial loss on PBO Prior service cost amortization Pension gainvloss amortization Contributions to fund Benefit payments Balance, December 31, 2020 0 0 0 (7,000) 56.000 0 O 0 16,800 (16,800) 0 D 0 x (123,200) 0 0 0 $ 0X $ (16,800) $ OX a. Prepare the December 31, 2019, presentation of funded status. Note: Use a negative sign for a net pension liability Net pension asset (liability), Dec. 31, 2019 $ (224,000) * ) b. Prepare the entries to record 2020 pension expense, gain and loss deferral (if any), contributions, and benefits. . Note: List multiple debits (when applicable) in alphabetical order and list multiple credits (when applicable) in alphabetical order. Note: Round your answers to the nearest whole dollar. . Cr. 0 0 Dr. 123,000 x 123,000 x 123,000 x 0 0 0 0 123,000 x 123,000 X 0 0 Date Account Name Dec 31, 2020 OCIPension Gain/Loss Pension Expense Plan Assets OCIPrior Service Cost Projected Benefit Obligation e To record pension expense Dec 31, 2020 Plan Assets OCI-Pension Gain/Loss To record deferral of unexpected gain/loss on plan assets Dec 31, 2020 OCIPension Gain/Loss Projected Benefit Obligation To record deferral of actuarial gain/loss on PBO Dec 31, 2020 Plan Assets Cash 123,000 X 0 0 123,000 X 0 56,000 0 0 56,000 0 123,000 x 0 123,000 X To record plans funding C. Prepare the December 31, 2020, presentation of funded status. . Note: Use a negative sign for a net pension liability Net pension asset (liability), Dec. 31, 2020 $ 224,000 * , d. Determine whether amortization of net unrecognized gain or loss is required for 2021. . Note: Round your answers to the nearest whole dollar. Amortization of OCIPension Gain/Loss, 2021 $ (224,000) Question 7 Partially correct Mark 10.77 out of 12.50 Flag question Preparing Pension Journal Entries and Pension Worksheet Information for the Jenkins Company defined benefit pension plan follows. Jenkins uses the straight-line method to amortize prior service cost and corridor amortization for gains and losses. Account Balances Jan 1, 2020 Projected Benefit obligation $980,000 Cr. Plan Assets 700,000 Dr. Accumulated OCI-Pension Gain/Loss 224,00D Cr. Accumulated OCI-Prior Service Cost 168,000 Dr. Activity Service cost, 2020 $84,000 Actuarial loss determined Dec 31, 2020 56,000 Actual return on plan assets, 2020 77,000 Funding 2020 123.200 Benefits paid, 2020 0 Other Discount rate 8% Expected rate of return on plan assets 10% % Average remaining service period of active plan participants 10 years Funded Status and Journal Entries Pension Worksheet e. Prepare a pension worksheet for 2020. a Note: Round your answers to the nearest whole dollar. Reported in Comprehensive Income OCI Pension Prior Pension Expense Service Cost Gain/Loss Cash Outflow 0$ 0$ 84,000 $ 78,400 (70,000) 0 0 0 Reported Net in Financial Statements Reported an Balance Sheet Accumulated OCI Plan Net Pension Prior Pension Assets PBO Asset/Liability Service Cost Gain/Loss $ 700.000 $ (980.000) $ (280,000) 168,000 $ 1224,000) O 184.000) (84000) 0 0$ 0 178,400) (78,400) D 70.000 70,000 0 7,000 7,000 (7,000) 0 (56,000) (56,000) 0 56,000 (16,800) 0 O D 0 123.200 123,200 0 0 D D 0 $ 900.200$ (1,198.400) (298,200) S S 151,200 $ 0* Balance, January 1, 2020 Service cost Interest cost Expected return Unexpected yain on plan assets Actuarial loss on PBO Prior service cost amortization Pension gainvloss amortization Contributions to fund Benefit payments Balance, December 31, 2020 0 0 0 (7,000) 56.000 0 O 0 16,800 (16,800) 0 D 0 x (123,200) 0 0 0 $ 0X $ (16,800) $ OXStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Susan V. Crosson, Belverd E. Needles

8th Edition

9780618777174, 618777180, 618777172, 978-0618777181