Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need help solving 8) and 9) using the following info below percentages used for 8) Question 8) and 9) to be solved below Garden Sales,

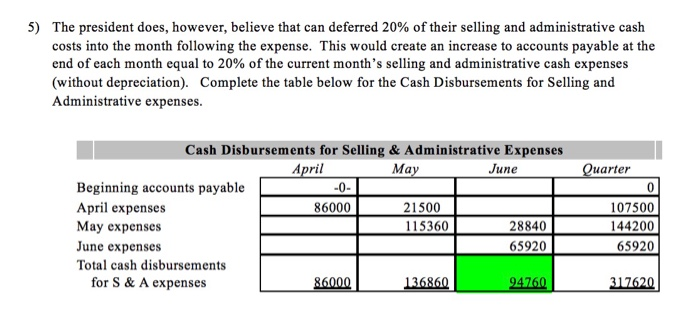

need help solving 8) and 9) using the following info below

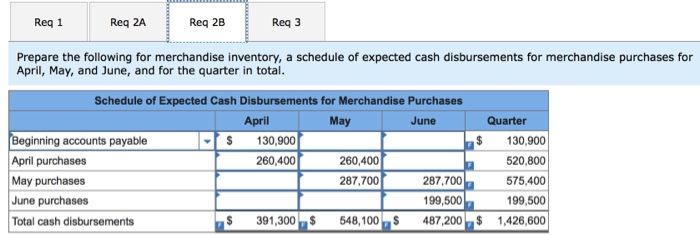

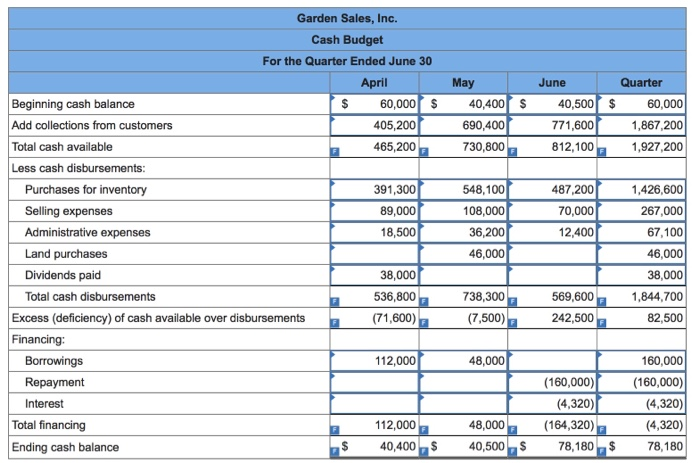

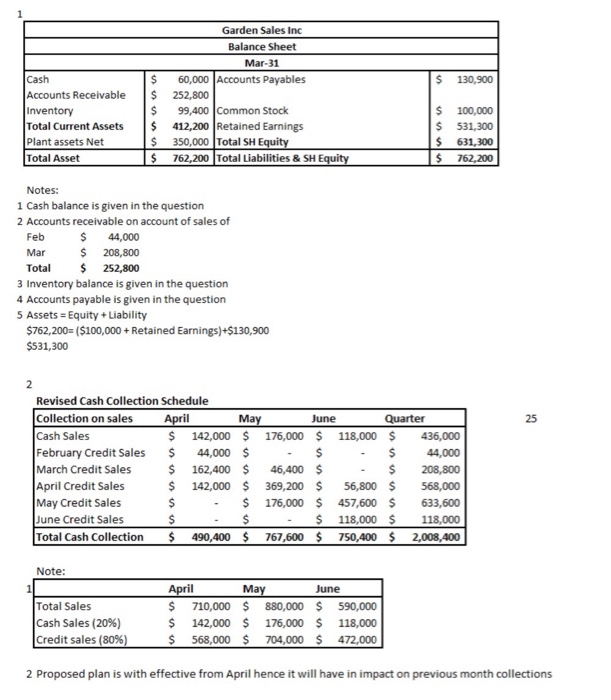

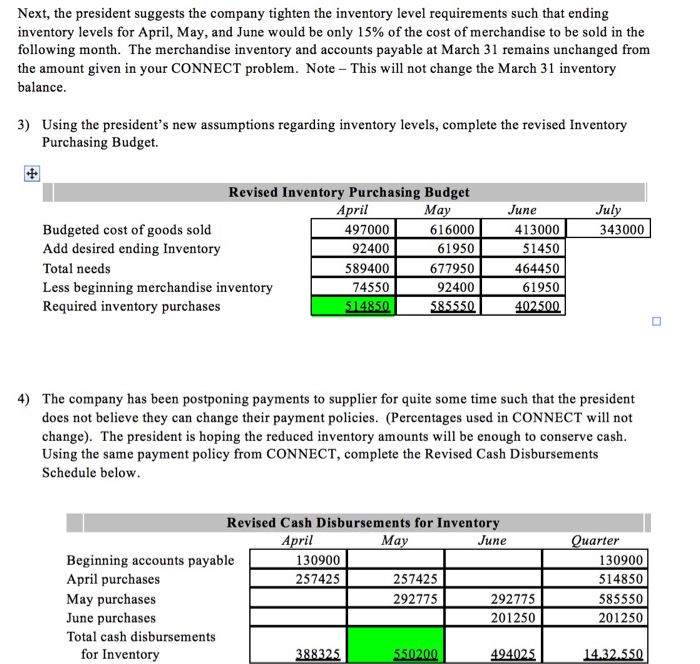

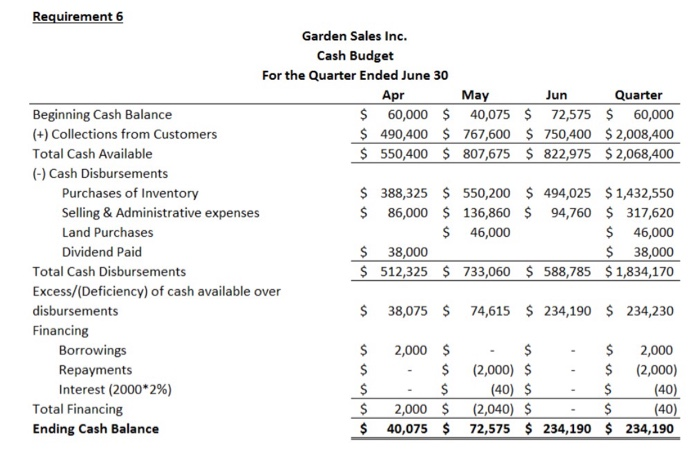

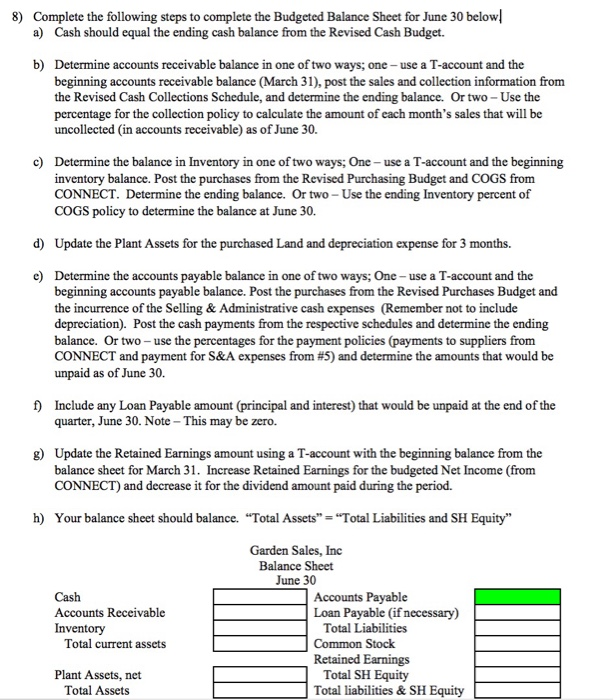

Garden Sales, Inc., sells garden supplies. Management is planning its cash needs for the second quarter. The company usually has to borrow money during this quarter to support peak sales of lawn care equipment, which occur during May. The following information has been assembled to assist in preparing a cash budget for the quarter: a. Budgeted monthly absorption costing income statements for April-July are: April May June July $ 710,000 $ 880,000 $ 590,000 $ 490,000 497,000 616,000 413,000 343,000 213,000 264,000 177,000 147,000 Sales Cost of goods sold Gross margin Selling and administrative expenses : Selling expense Administrative expense* Total selling and administrative expenses Net operating income 89,000 108,000 70,000 49,000 49,500 67,200 43,400 47,000 138,500 175,200 113,400 96,000 $ 74,500 $ 88,800 $ 63,600 $ 51,000 *Includes $31,000 of depreciation each month. b. Sales are 20% for cash and 80% on account. c. Sales on account are collected over a three-month period with 10% collected in the month of sale; 70% collected in the first month following the month of sale; and the remaining 20% collected in the second month following the month of sale. February's sales totaled $275,000, and March's sales totaled $290,000. d. Inventory purchases are paid for within 15 days. Therefore, 50% of a month's inventory purchases are paid for in the month of purchase. The remaining 50% is paid in the following month. Accounts payable at March 31 for inventory purchases during March total $130,900. e. Each month's ending inventory must equal 20% of the cost of the merchandise to be sold in the following month. The merchandise inventory at March 31 is $99,400. f. Dividends of $38,000 will be declared and paid in April. g. Land costing $46,000 will be purchased for cash in May. h. The cash balance at March 31 is $60,000; the company must maintain a cash balance of at least $40,000 at the end of each month. 1. The company has an agreement with a local bank that allows the company to borrow in increments of $1,000 at the beginning of each month, up to a total loan balance of $200,000. The interest rate on these loans is 1% per month and for simplicity we will assume that interest is not compounded. The company would, as far as it is able, repay the loan plus accumulated interest at the end of the quarter. Req 1 Req 2A Req 2B Req3 Prepare a schedule of expected cash collections for April, May, and June, and for the quarter in total. Schedule of Expected Cash Collections April May June Quarter $ 142,000 $ 176,000 $ 118,000 $ 436,000 Cash sales Sales on account: February March April May June Total cash collections 44,000 162,400 56,800 46,400 397,600 70,400 44,000 208,800 113,600 568,000 492,800 563,200 47,200 47,200 771,600$ 1,867,200 405,200 $ 690,400$ Req 1 Reg 2A Req 2B Req3 Prepare the following for merchandise inventory, a merchandise purchases budget for April, May, and June. Merchandise Purchases Budget April May June Budgeted cost of goods sold $ 497,000 $ 616,000 $ 413,000 Add: Desired ending merchandise inventory 123,2001 82,600 68,600 Total needs 620,200 698,600 481,600 Less: Beginning merchandise inventory 99,400 123,200 82,600 Required inventory purchases $ 520,800 $ 575,400$ 399,000 Reg 1 Req 2A Req 2B Req3 Prepare the following for merchandise inventory, a schedule of expected cash disbursements for merchandise purchases for April, May, and June, and for the quarter in total. Schedule of Expected Cash Disbursements for Merchandise Purchases April May June Quarter Beginning accounts payable 130,900 130,900 April purchases 260,400 260,400 520,800 May purchases 287,700 287,700 575,400 June purchases 199,500 199,500 Total cash disbursements 391,300 $ 548,100 $ 487,200 $ 1,426,600 May 40,400 $ 690,400 730,800 June Quarter 40,500 $ 60,000 771,600 1,867,200 812,100 1,927,200 Garden Sales, Inc. Cash Budget For the Quarter Ended June 30 April Beginning cash balance $ 60,000 $ Add collections from customers 405,200 Total cash available 465,200 Less cash disbursements: Purchases for inventory 391,300 Selling expenses 89,000 Administrative expenses 18,500 Land purchases Dividends paid 38,000 Total cash disbursements 536,800 Excess deficiency) of cash available over disbursements (71,600) Financing: Borrowings 112,000 Repayment Interest Total financing 112,000 Ending cash balance $ 40,400$ 548,100 108,000 36,200 46,000 487,200 70,000 12,400 1,426,600 267,000 67,100 46,000 38,000 1,844,700 82,500 738,300 (7,500) 569,600 242,500 48,000 (160,000) (4,320) (164,320) 78,180$ 160,000 (160,000) (4,320) (4,320) 78,180 48,000 40,500$ $ 130,900 Cash Accounts Receivable Inventory Total Current Assets Plant assets Net Total Asset Garden Sales Inc Balance Sheet Mar-31 $ 60,000 Accounts Payables $ 252,800 $ 99,400 Common Stock $ 412,200 Retained Earnings $ 350,000 Total SH Equity $ 762,200 Total Liabilities & SH Equity $ $ 100,000 531,300 631,300 762,200 $ $ Notes: 1 Cash balance is given in the question 2 Accounts receivable on account of sales of Feb $ 44,000 Mar $ 208,800 Total $ 252,800 3 Inventory balance is given in the question 4 Accounts payable is given in the question 5 Assets = Equity + Liability $762,200=($100,000 + Retained Earnings)+$130,900 $531,300 2 June 25 $ $ Revised Cash Collection Schedule Collection on sales April May Quarter Cash Sales $ 142,000 $ 176,000 $ 118,000 $ 436,000 February Credit Sales 44,000 $ $ 44,000 March Credit Sales $ 162,400 $ 46,400 $ $ 208,800 April Credit Sales $ 142,000 $ 369,200 $ 56,800 $ 568,000 May Credit Sales $ $ 176,000 $ 457,600 $ 633,600 June Credit Sales $ $ $ 118,000 $ 118,000 Total Cash Collection $ 490,400 $ 767,600 $ 750,400 $ 2,008,400 Note: Total Sales Cash Sales (20%) Credit sales (80%) April May June $ 710,000 $ 880,000 $ 590,000 $ 142,000 $ 176,000 $ 118,000 $ 568,000 $ 704,000 $ 472,000 2 Proposed plan is with effective from April hence it will have in impact on previous month collections Next, the president suggests the company tighten the inventory level requirements such that ending inventory levels for April, May, and June would be only 15% of the cost of merchandise to be sold in the following month. The merchandise inventory and accounts payable at March 31 remains unchanged from the amount given in your CONNECT problem. Note - This will not change the March 31 inventory balance. 3) Using the president's new assumptions regarding inventory levels, complete the revised Inventory Purchasing Budget. July 343000 Revised Inventory Purchasing Budget April May Budgeted cost of goods sold 497000 616000 Add desired ending Inventory 92400 61950 Total needs 589400 677950 Less beginning merchandise inventory 74550 92400 Required inventory purchases 514850 585550 June 413000 51450 464450 61950 402.500 4) The company has been postponing payments to supplier for quite some time such that the president does not believe they can change their payment policies. (Percentages used in CONNECT will not change). The president is hoping the reduced inventory amounts will be enough to conserve cash. Using the same payment policy from CONNECT, complete the Revised Cash Disbursements Schedule below. Revised Cash Disbursements for Inventory April May June Beginning accounts payable 130900 April purchases 257425 257425 May purchases 292775 292775 June purchases 201250 Total cash disbursements for Inventory 388325 550200 494025 Quarter 130900 514850 585550 201250 14.32.550 5) The president does, however, believe that can deferred 20% of their selling and administrative cash costs into the month following the expense. This would create an increase to accounts payable at the end of each month equal to 20% of the current month's selling and administrative cash expenses (without depreciation). Complete the table below for the Cash Disbursements for Selling and Administrative expenses. Cash Disbursements for Selling & Administrative Expenses April May June Beginning accounts payable -0- April expenses 86000 21500 May expenses 115360 28840 June expenses 65920 Total cash disbursements for S & A expenses 86000 136860 94760 Quarter 0 107500 144200 65920 317620 Jun Requirement 6 Garden Sales Inc. Cash Budget For the Quarter Ended June 30 Apr May Quarter Beginning Cash Balance $ 60,000 $ 40,075 $ 72,575 $ 60,000 (+) Collections from Customers $ 490,400 $ 767,600 $ 750,400 $ 2,008,400 Total Cash Available $ 550,400 $ 807,675 $ 822,975 $ 2,068,400 (-) Cash Disbursements Purchases of Inventory $ 388,325 $ 550,200 $ 494,025 $1,432,550 Selling & Administrative expenses $ 86,000 $ 136,860 $ 94,760 $ 317,620 Land Purchases $ 46,000 $ 46,000 Dividend Paid $ 38,000 $ 38,000 Total Cash Disbursements $ 512,325 $ 733,060 $ 588,785 $1,834,170 Excess/(Deficiency) of cash available over disbursements $ 38,075 $ 74,615 $ 234,190 $ 234,230 Financing Borrowings $ 2,000 $ $ $ 2,000 Repayments $ $ (2,000) $ $ (2,000) Interest (2000*2%) $ $ (40) $ $ (40) Total Financing $ 2,000 $ (2,040) $ $ (40) Ending Cash Balance $ 40,075 $ 72,575 $ 234,190 $ 234,190 8) Complete the following steps to complete the Budgeted Balance Sheet for June 30 below! a) Cash should equal the ending cash balance from the Revised Cash Budget. b) Determine accounts receivable balance in one of two ways; one - use a T-account and the beginning accounts receivable balance (March 31), post the sales and collection information from the Revised Cash Collections Schedule, and determine the ending balance. Or two-Use the percentage for the collection policy to calculate the amount of each month's sales that will be uncollected in accounts receivable) as of June 30. c) Determine the balance in Inventory in one of two ways; One - use a T-account and the beginning inventory balance. Post the purchases from the Revised Purchasing Budget and COGS from CONNECT. Determine the ending balance. Or two - Use the ending Inventory percent of COGS policy to determine the balance at June 30. d) Update the Plant Assets for the purchased Land and depreciation expense for 3 months. e) Determine the accounts payable balance in one of two ways: One - use a T-account and the beginning accounts payable balance. Post the purchases from the Revised Purchases Budget and the incurrence of the Selling & Administrative cash expenses (Remember not to include depreciation). Post the cash payments from the respective schedules and determine the ending balance. Or two - use the percentages for the payment policies (payments to suppliers from CONNECT and payment for S&A expenses from #5) and determine the amounts that would be unpaid as of June 30. 1) Include any Loan Payable amount (principal and interest) that would be unpaid at the end of the quarter, June 30. Note - This may be zero. g) Update the Retained Earnings amount using a T-account with the beginning balance from the balance sheet for March 31. Increase Retained Earnings for the budgeted Net Income (from CONNECT) and decrease it for the dividend amount paid during the period. h) Your balance sheet should balance. "Total Assets" = "Total Liabilities and SH Equity" Cash Accounts Receivable Inventory Total current assets Garden Sales, Inc Balance Sheet June 30 Accounts Payable Loan Payable (if necessary) Total Liabilities Common Stock Retained Earnings Total SH Equity Total liabilities & SH Equity Plant Assets, net Total Assets 9) The production manager confides to the president that estimating ending inventories in the budget is sometimes difficult and he is concerned about the impact of reduced inventory levels on the company's ability to meet sales. He explains that the sale manager sometimes adjusts the sales numbers before passing them on. When questioned by the president, the sales manager admits that she doesn't want the company to fall short of its sales projections, so she generally gives a little bit of "breathing room by lowering the initial sales projection anywhere from 5% to 10%. Should the president be concerned about the budgetary slack being used by the sales manager? Explain in 30 to 50 words percentages used for 8)

Question 8) and 9) to be solved below

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Implementing And Auditing The Internal Control System

Authors: D. Chorafas

2001edition

0333929365, 978-0333929360