Need help with question 1:

Examine the 2011 financial statements provided by PMI and the 2010 financial statements provided by Jackson and Associates to answer the following.

a. Discuss the differences in the Financial Statements and the effect that these differences have on the Revenues and Receivables.

b. Discuss the ethical dilemma facing PMI in terms of preparing the Financial Statements.

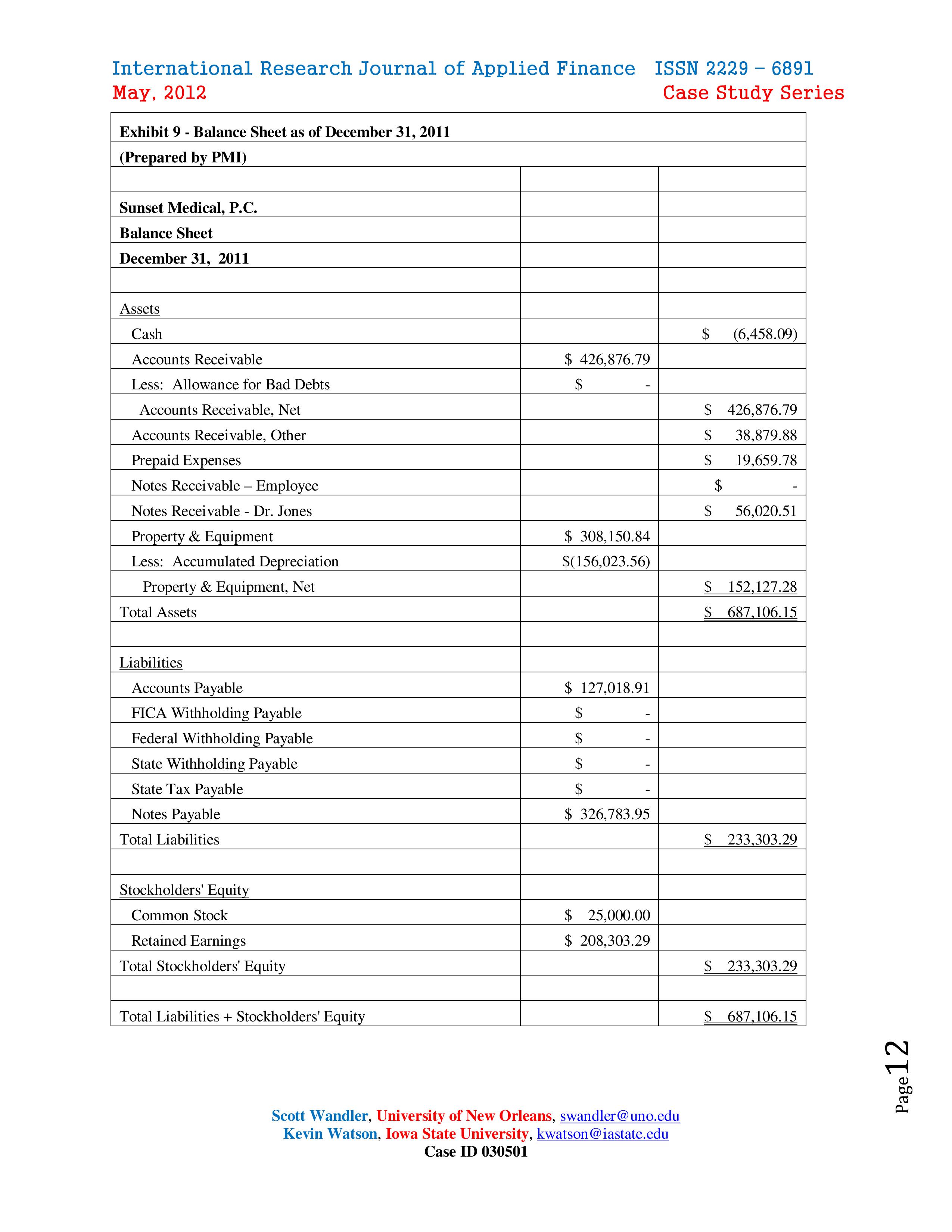

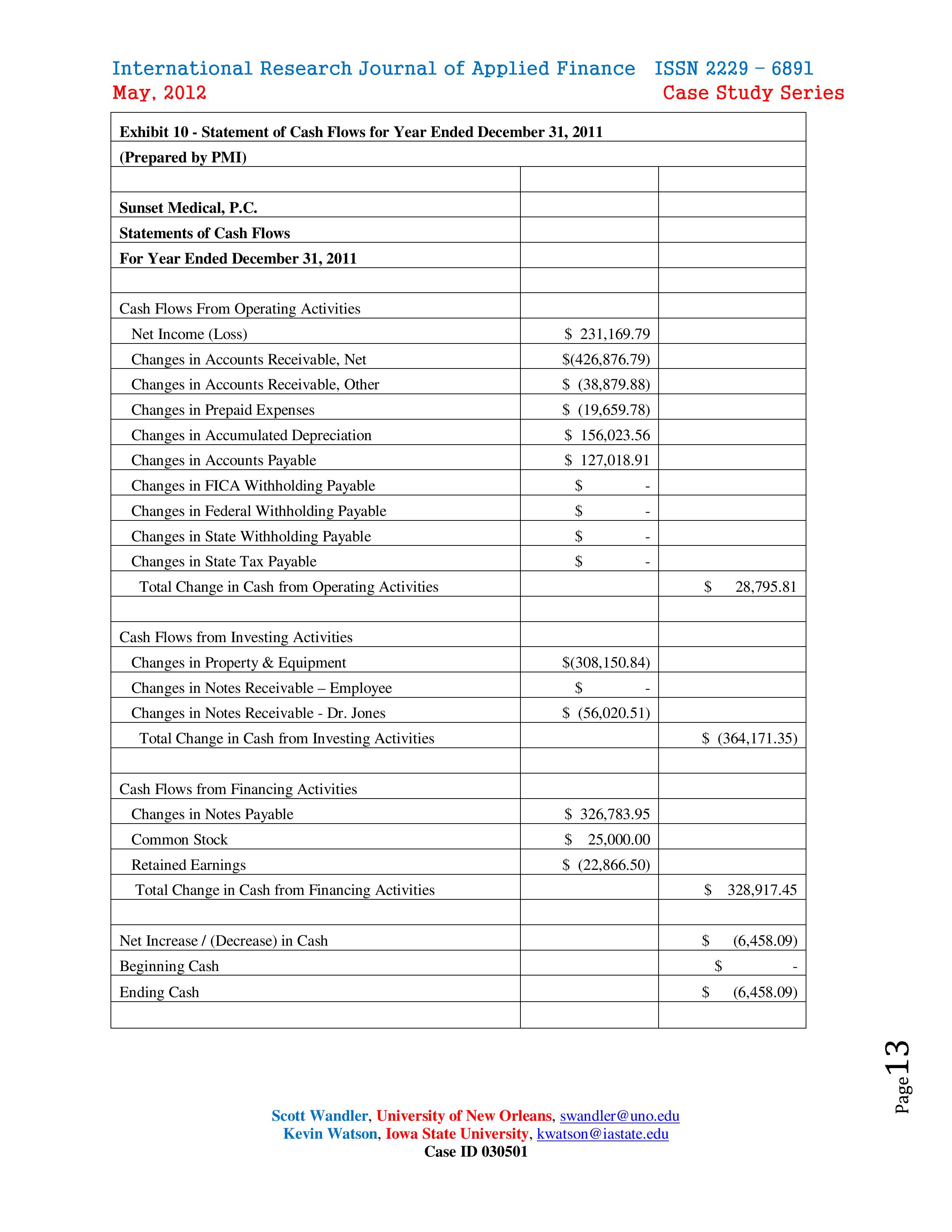

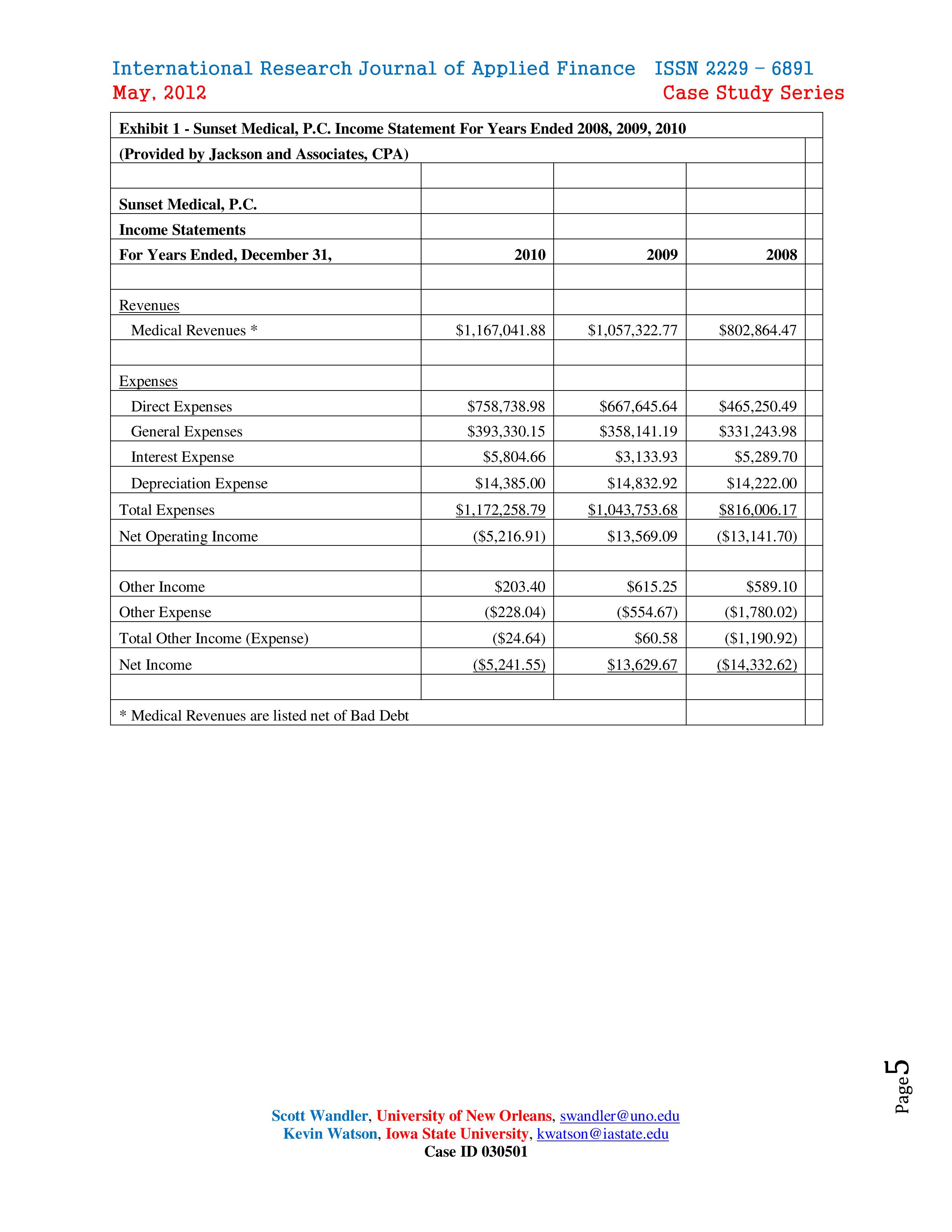

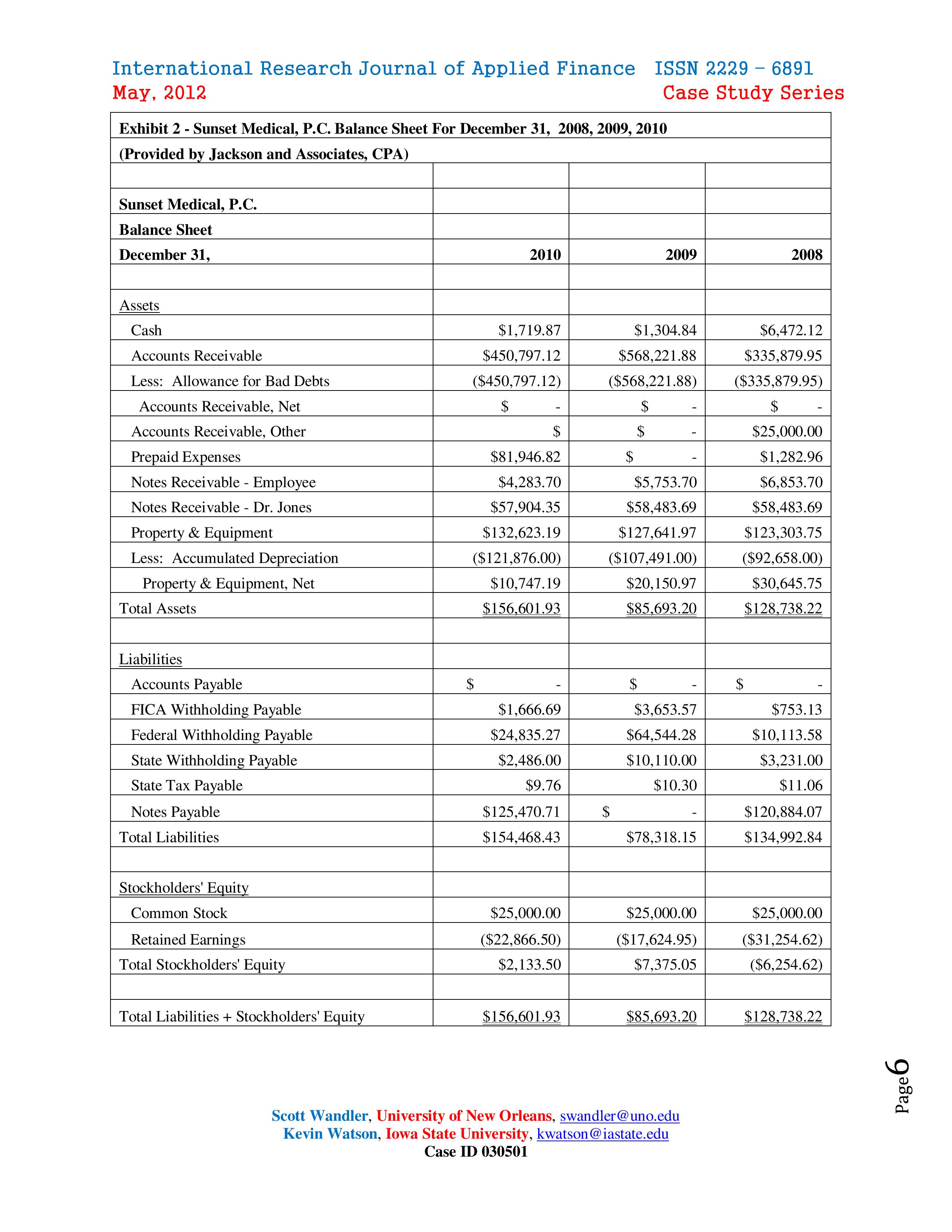

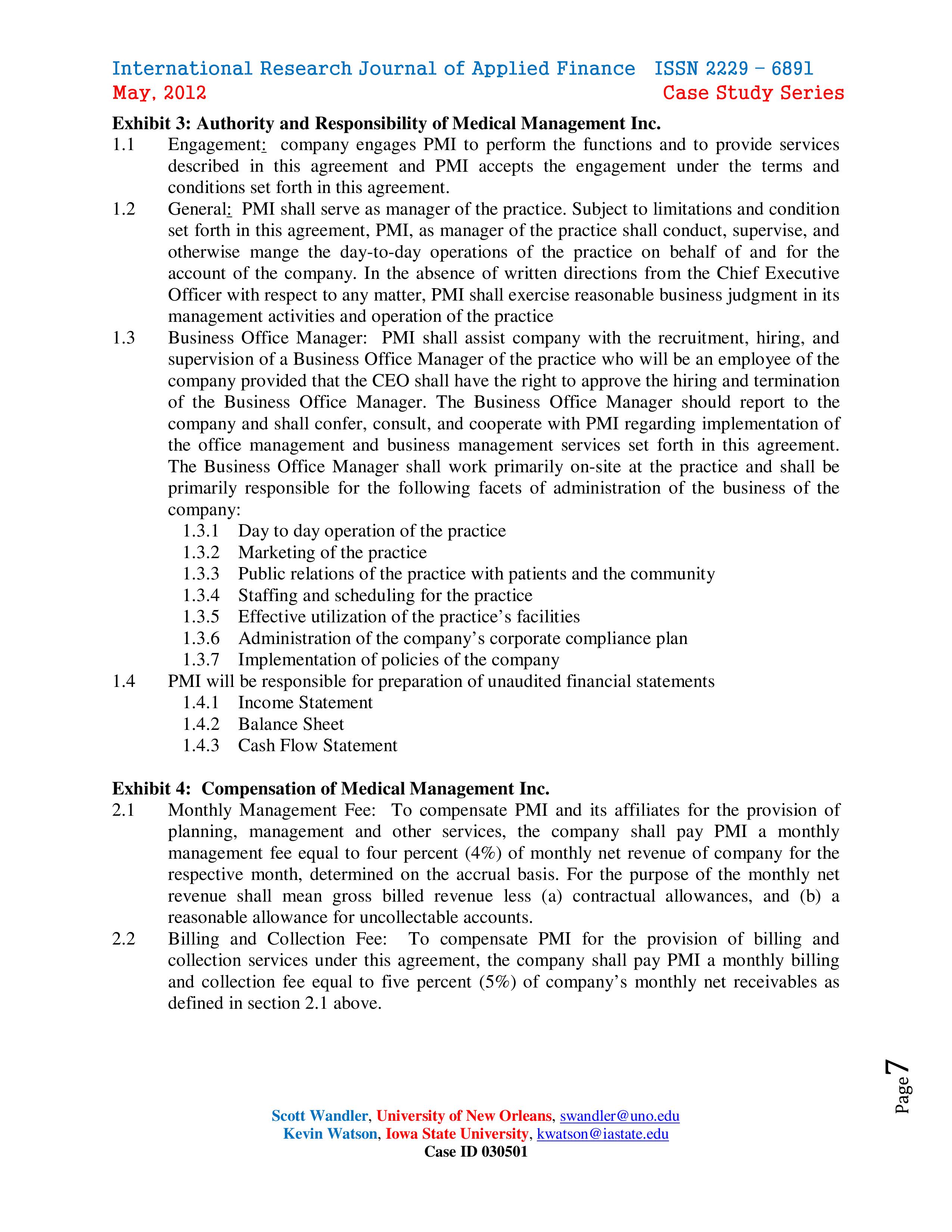

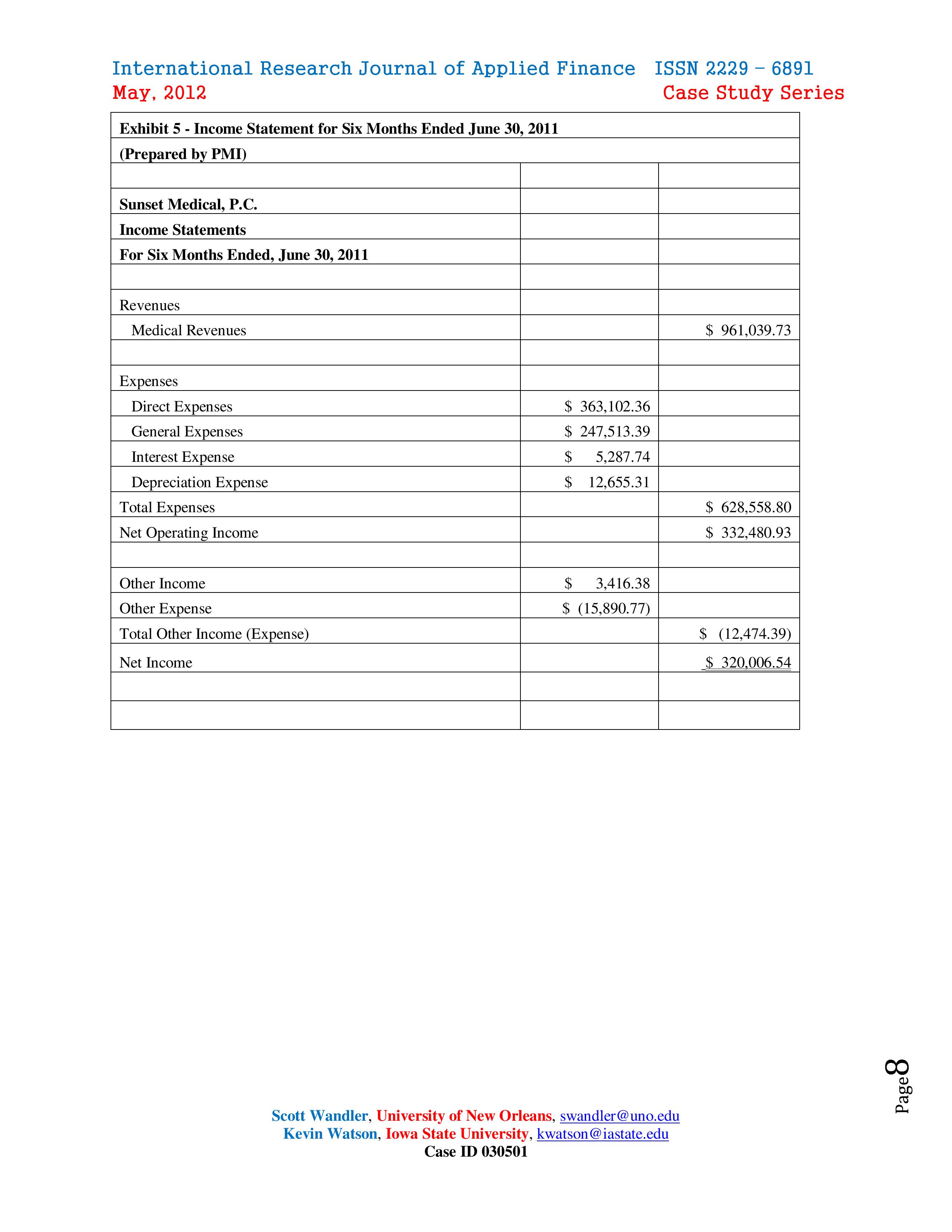

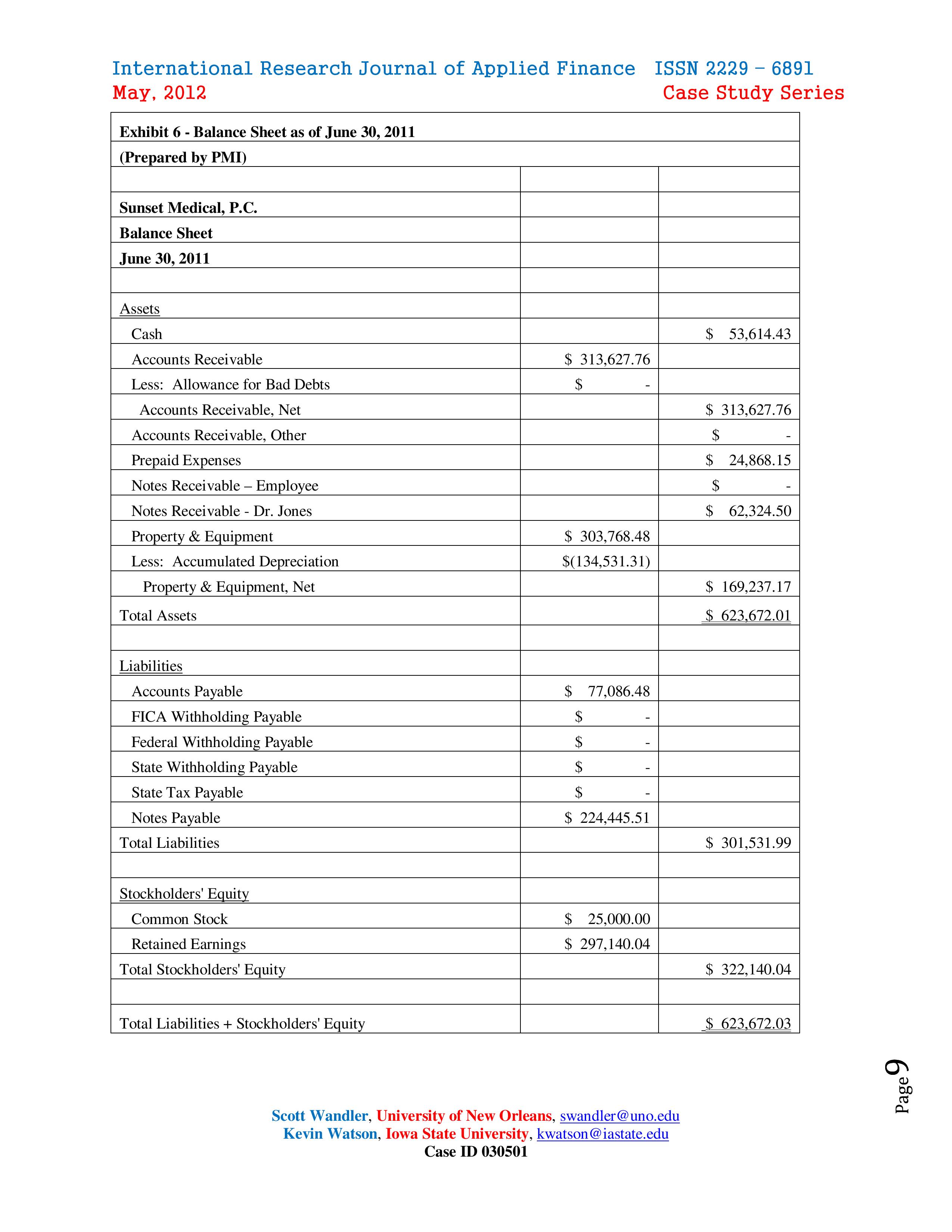

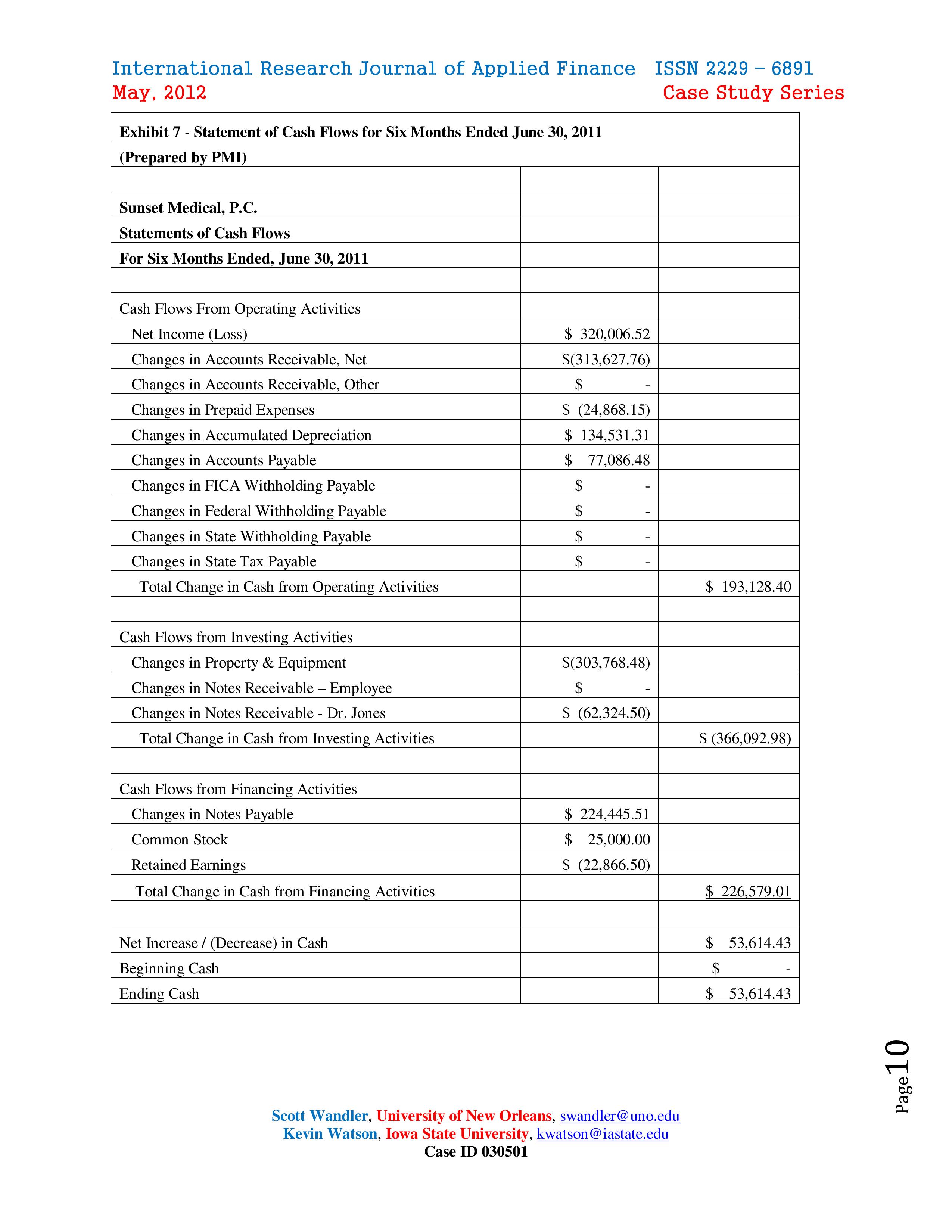

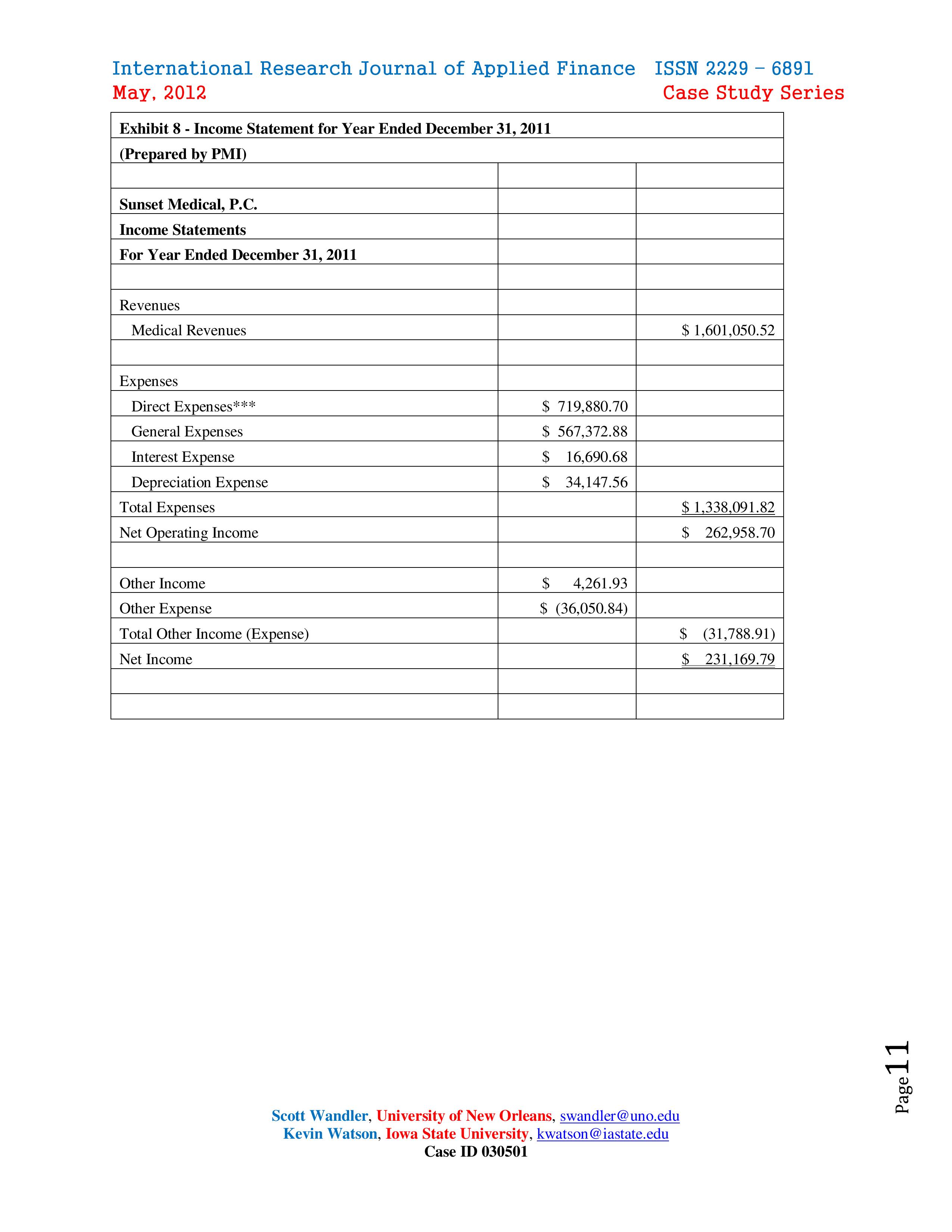

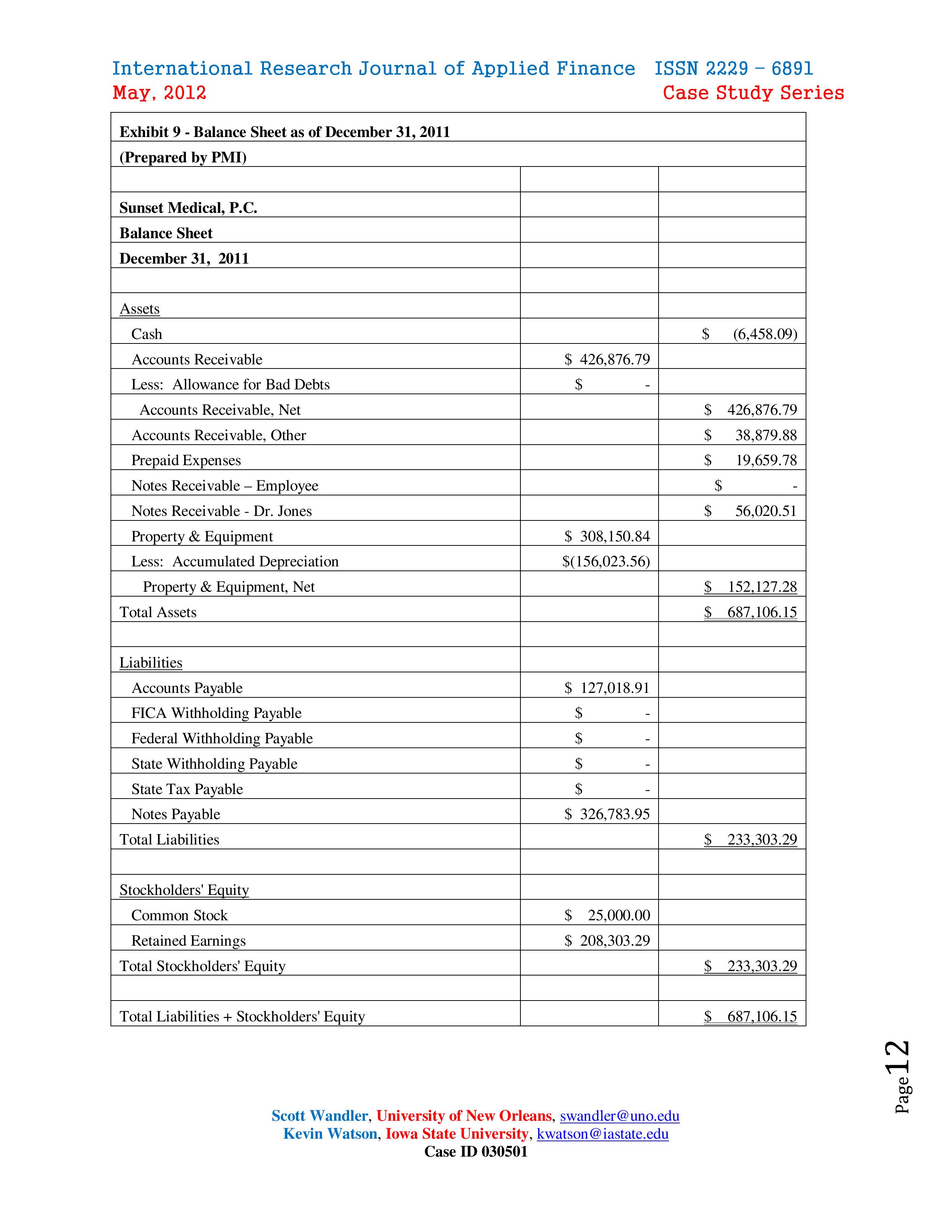

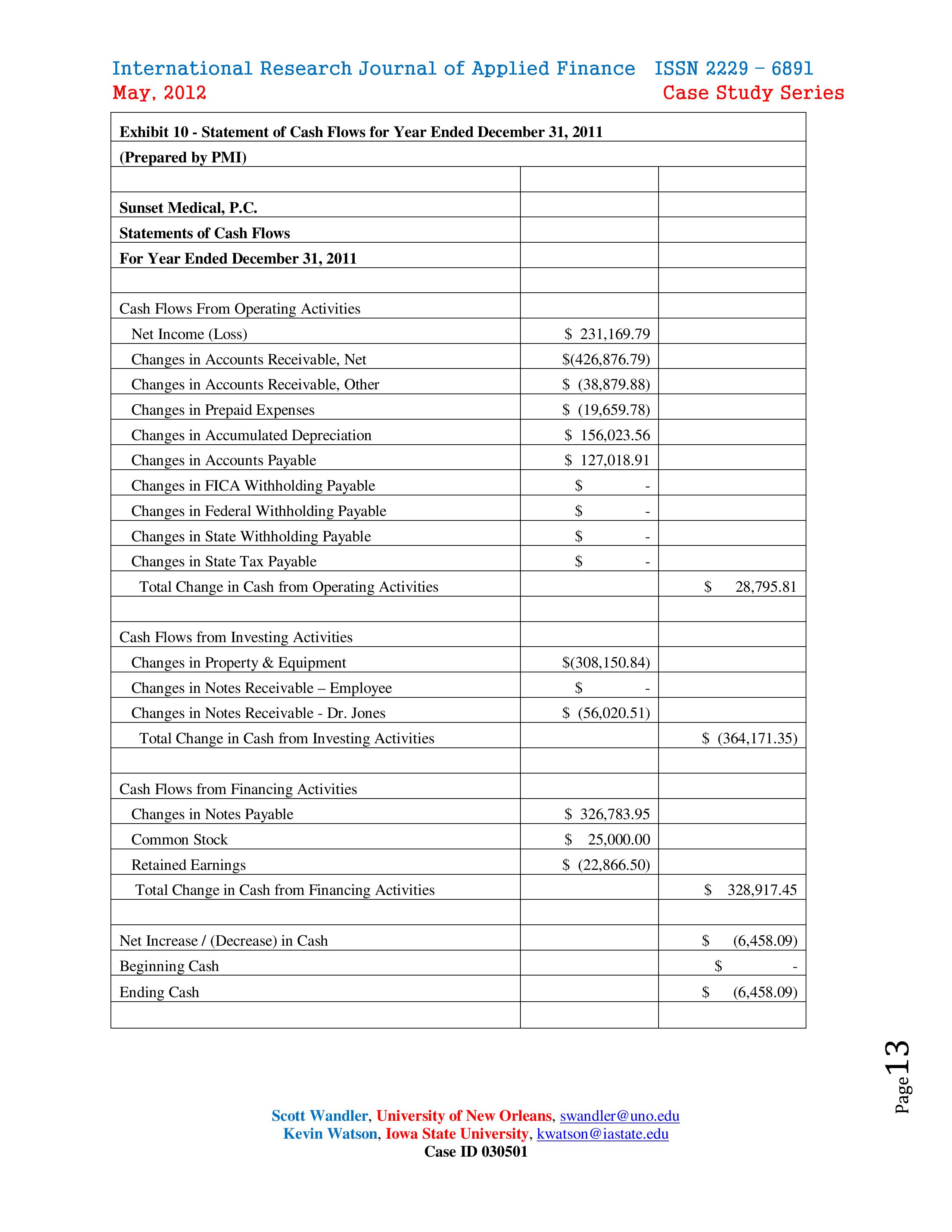

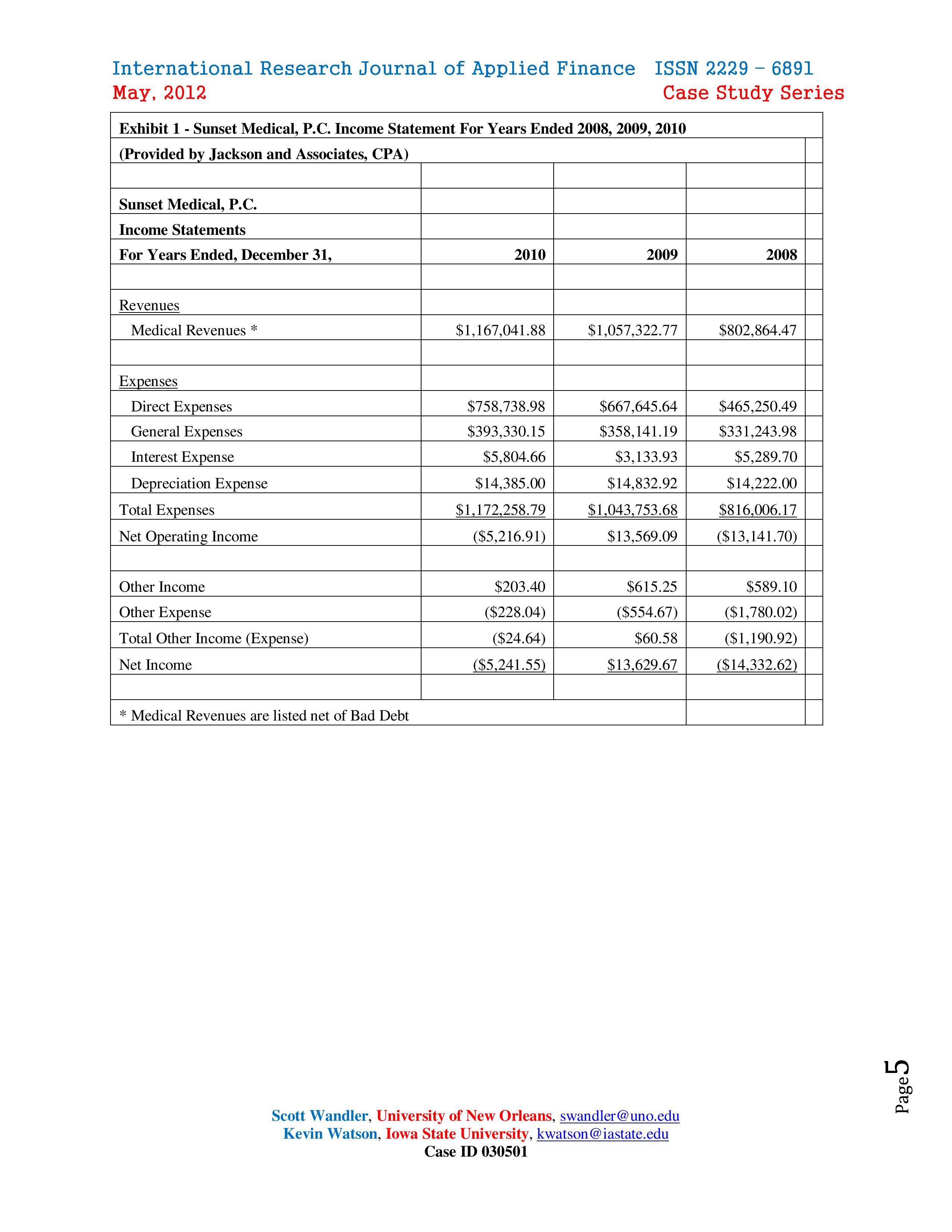

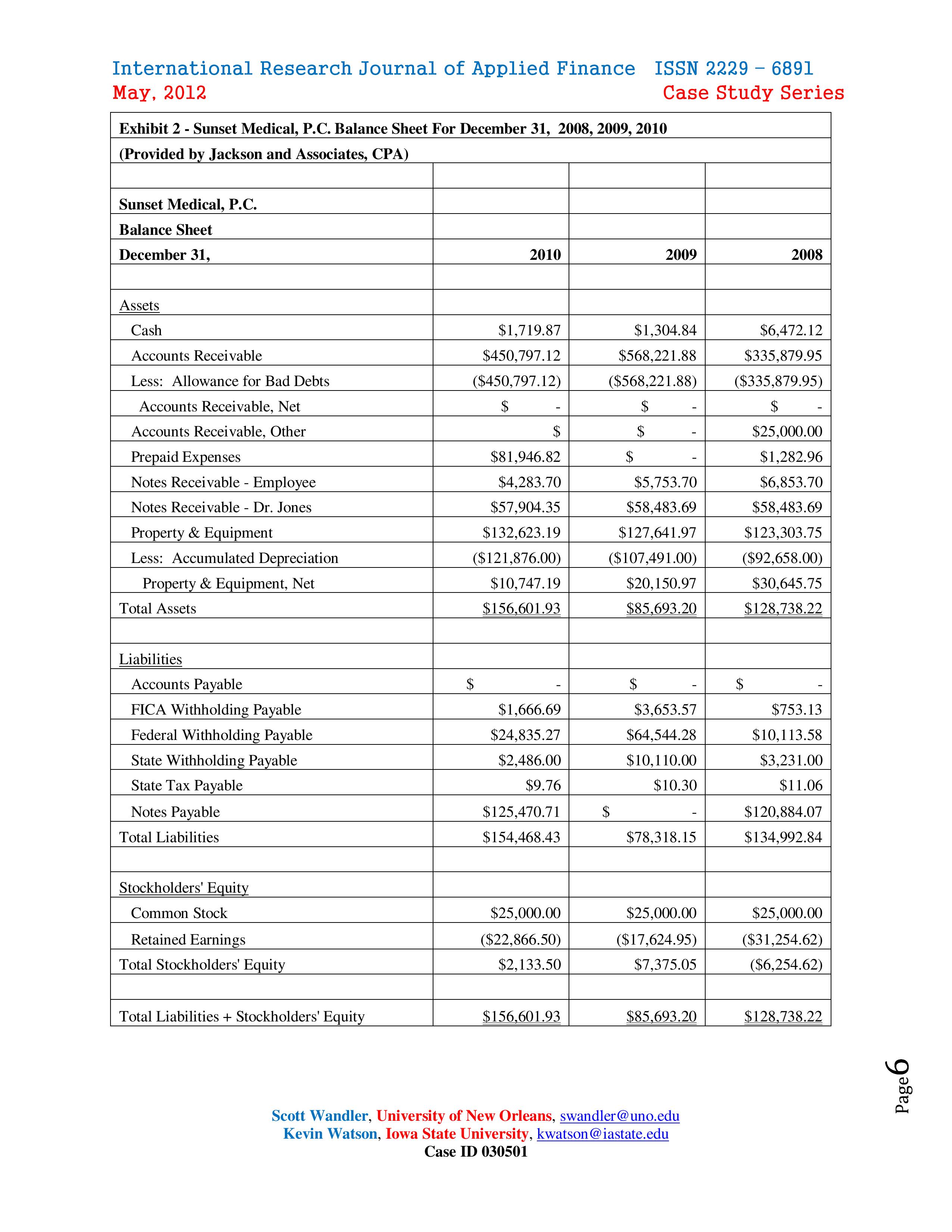

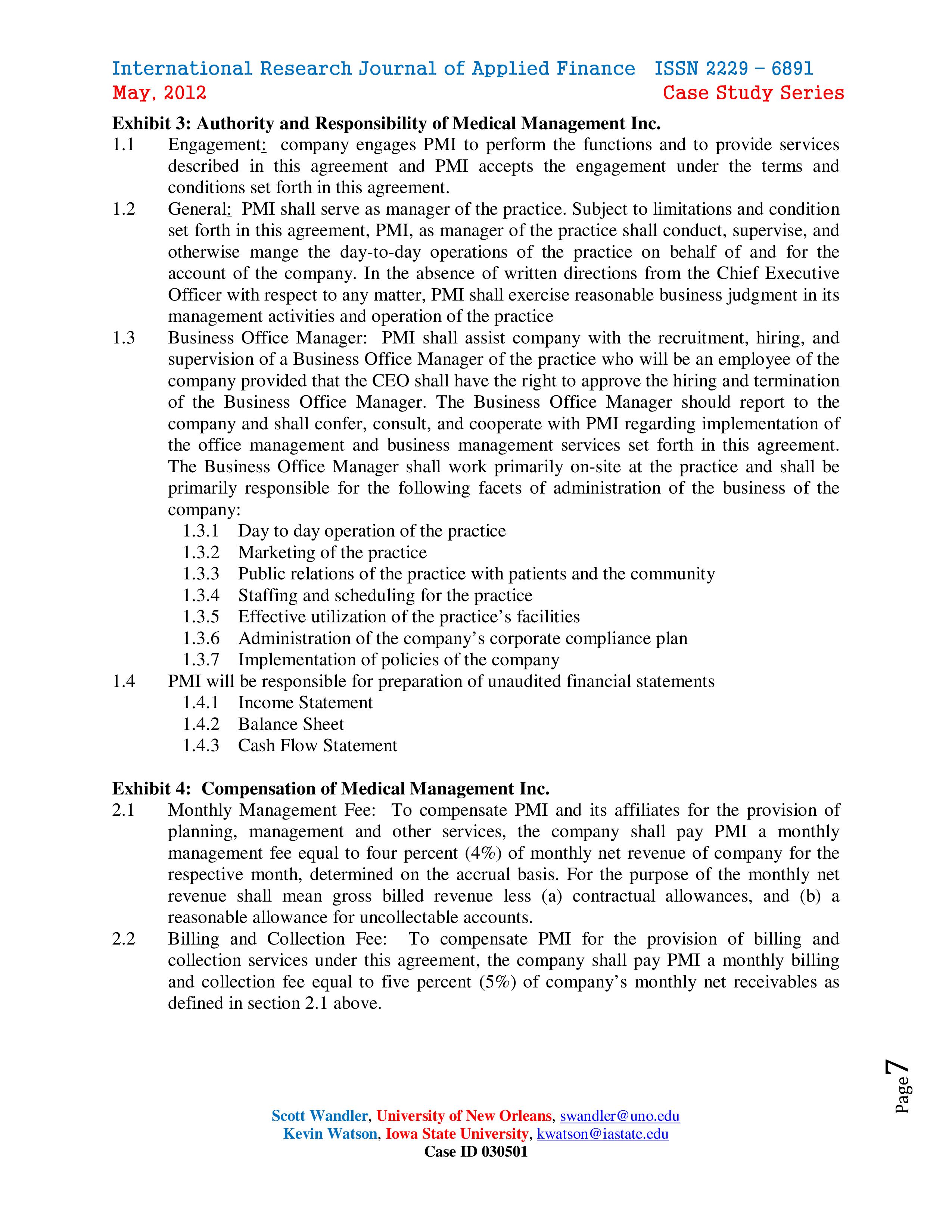

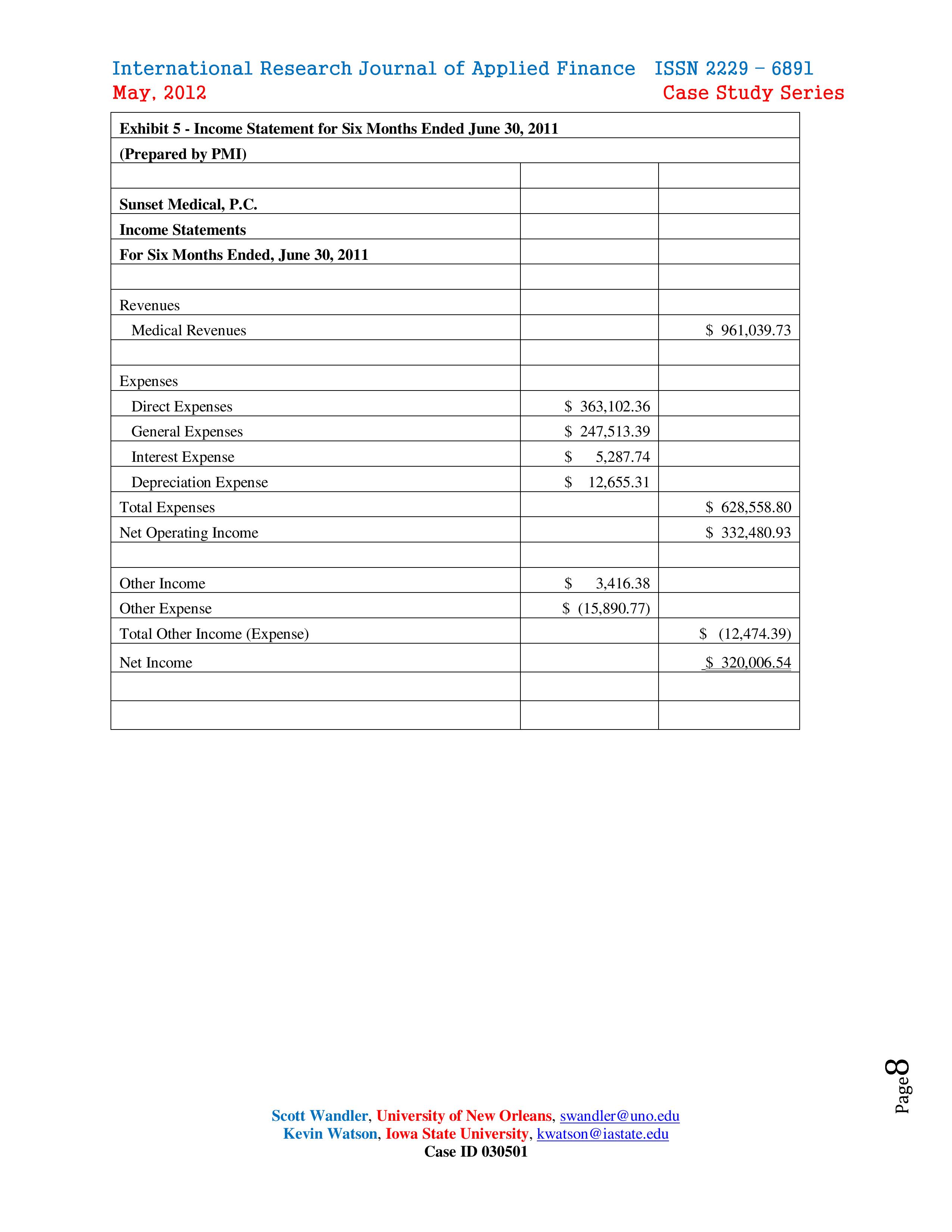

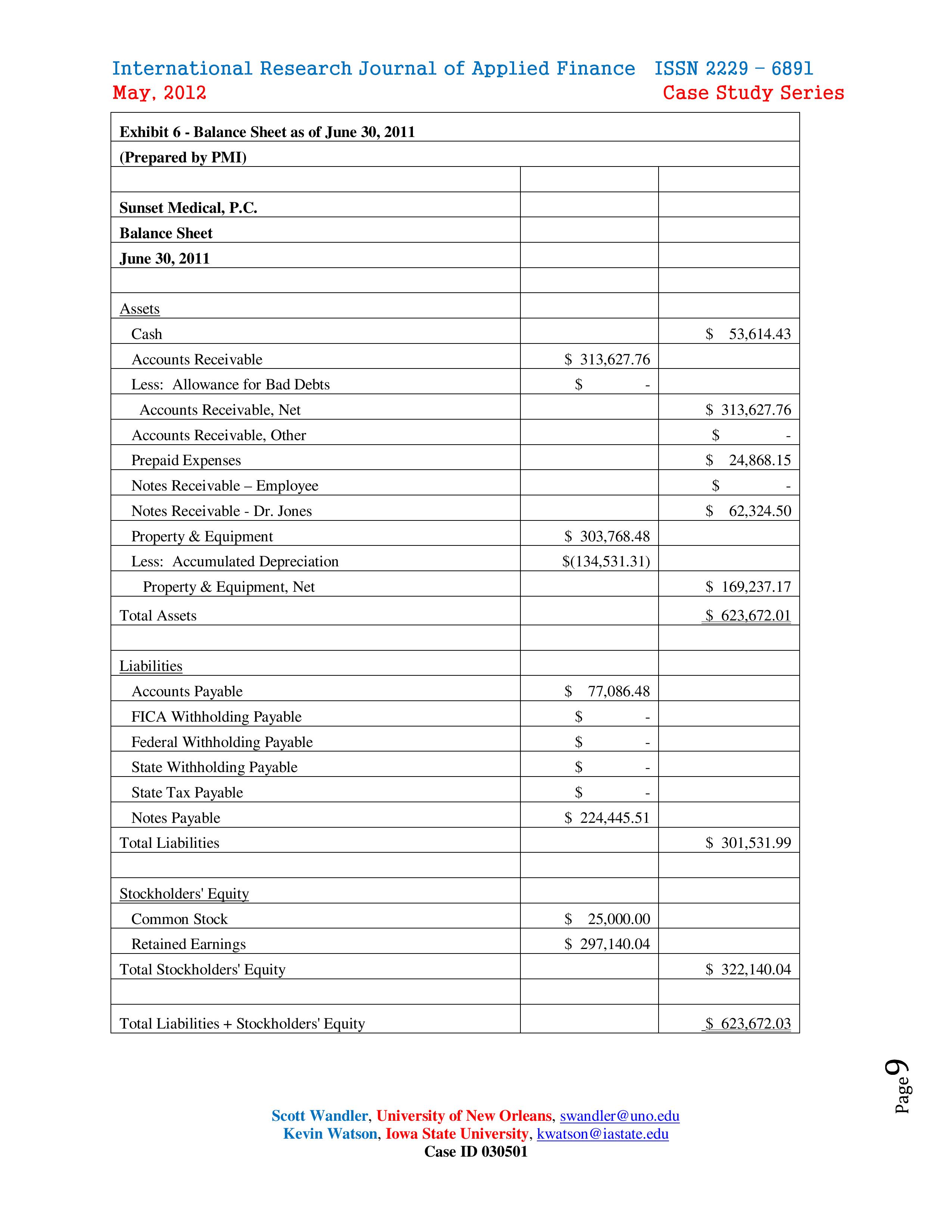

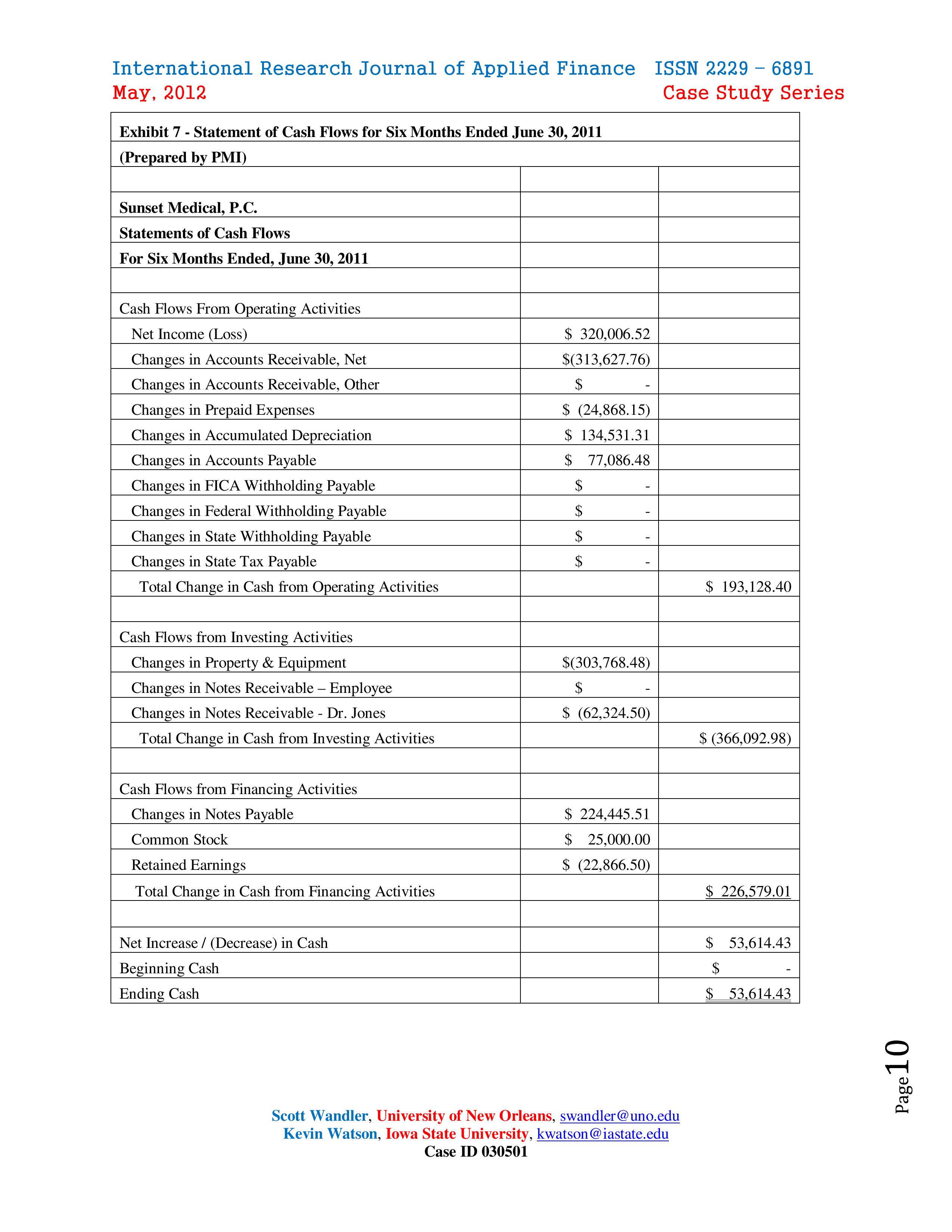

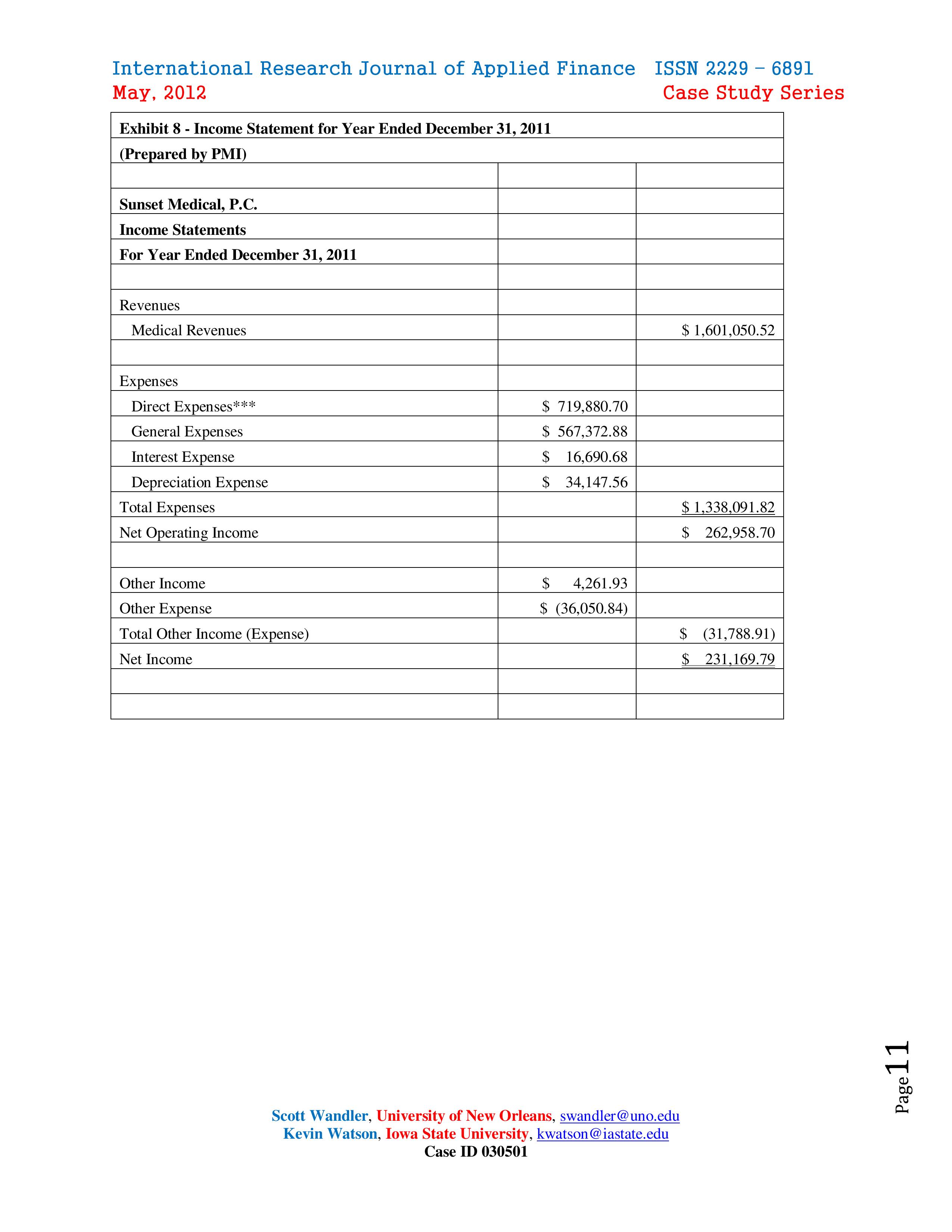

International Research Journal of Applied Finance ISSN 2229 6891 May, 2012 Case Study Series Abstract Sunset Medical is based on a real situation occurring at an Orthopedic Medical practice in Colorado. While attending a trade show Dr. Jones, the managing partner at Sunset Medical, was approached by a medical consulting firm, Physicians Medical Inc. (PMI), to provide the practice billing and administrative services. Dr. Jones decided to hire PMI and signed a contract in February of 2011. Based on the interim financial statements that were released in June of 2011, Dr. Jones gave PMI control of the overall day to day operations of the practice. PMI immediately relieved the office manager of her duties and took over all operations of the practice. In early 2012, the 2011 nancial statements were released and were not as impressive as the mid-year results. Dr. Jones is now worried that the increased power given to PMI may have been a mistake and has asked you to give a full assessment of the situation. The case is suitable for an introductory Financial or Managerial Accounting class at the MBA. level once the students have a working knowledge of the financial statements. The students must critically evaluate contract language and financial statements to examine ethical dilemmas that face businesses. I. Introduction Dr. Sally Jones, a practicing Orthopedic Surgeon, is the managing partner at Sunset Medicall, a professional corporation located in Colorado. Sunset, which has been in business for approximately 10 years, is a small medical practice with 2010 revenues of just over $1,000,000. The practice employs a support staff that includes an office manager, billing secretary, nurse, and radiology technician. In addition to the staff, Sunset retains Jackson and Associates, a CPA firm, to provide financial statements and tax documents. As a small, privately held corporation, Sunset is only required to submit an Income Statement and Balance Sheet using cash basis accounting, which Jackson and Associates prepares. Most of the staff and the CPA rm have been with Sunset Medical for all ten years of Sunset's operation. Exhibits 1 and 2 show the Income Statements and Balance Sheets provided by Jackson and Associates for the years 2008, 2009, and 2010. In January 2011, Sunset was considering the purchase of a new X-Ray machine and attended a trade show to do some research. While attending the trade show, Dr. Jones was approached by Ron Wilson of Physicians Management Inc. (PMI) with a proposal to provide management and billing services to Sunset Medical. Mr. Wilson is the founder and CEO of PMI, a twoyear old medical billing and administrative service company serving the southwest United States. PMI based its value proposition on increasing revenues, decreasing administrative expenses, and helping manage cash flows. Since administrative paperwork and billing averages between 4 and 9 percent of the expenses for most healthcare providers, not including lost revenue from billing errors, Dr. Jones decided to hire PMI to manage the practice. On February 3, 2011, a contract was signed, effectively turning over management duties of Sunset Medical to PMI. II. The Physicians Management Contract A few key points from the contract between Sunset Medical and PMI include the scope of the engagement, party responsibility, and compensation of PMI. Exhibits 3 and 4 contain excerpts from the contract discussing authority, responsibility, and compensation. Under the initial contract, PMI was to serve as the manager of the practice and assist the Business Office Manager 1 While this case uses actual data from an Orthopedic practice, all names have been changed and any resemblance to actual persons or companies is purely coincidental. Scott Wandler, University of New Orleans, swandler@uno.edu Kevin Watson, Iowa State University, kwatson@iastate.edu Case 1]) 030501 Pagez International Research Journal of Applied Finance ISSN 2229 - 6891 May, 2012 Case Study Series Exhibit 9 - Balance Sheet as of December 31, 2011 (Prepared by PMI) Sunset Medical, P.C. Balance Sheet December 31, 2011 Assets Cash $ (6,458.09) Accounts Receivable $ 426,876.79 Less: Allowance for Bad Debts $ Accounts Receivable, Net $ 426,876.79 Accounts Receivable, Other $ 38,879.88 Prepaid Expenses $ 19,659.78 Notes Receivable - Employee $ Notes Receivable - Dr. Jones $ 56,020.51 Property & Equipment $ 308, 150.84 Less: Accumulated Depreciation $(156,023.56) Property & Equipment, Net $ 152,127.28 Total Assets $ 687,106.15 Liabilities Accounts Payable $ 127,018.91 FICA Withholding Payable $ Federal Withholding Payable $ State Withholding Payable $ State Tax Payable $ Notes Payable $ 326,783.95 Total Liabilities $ 233,303.29 Stockholders' Equity Common Stock $ 25,000.00 Retained Earnings $ 208,303.29 Total Stockholders' Equity $ 233,303.29 Total Liabilities + Stockholders' Equity $ 687,106.15 Scott Wandler, University of New Orleans, swandler @uno.edu Page 1 2 Kevin Watson, Iowa State University, kwatson @ iastate.edu Case ID 030501International Research Journal of Applied Finance ISSN 2229 6891 Case Study Series May, 2012 Exhibit 10 - Statement of Cash Flows for Year Ended December 31, 2011 (Prepared by PMI) Sunset Medical, P.C. Statements of Cash Flows For Year Ended December 31, 2011 Cash Flows From Operating Activities Net Income (Loss) $ 23|,l69.79 Changes in Accounts Receivable, Net $(426,876.79) Changes in Accounts Receivable, Other $ (38,879.88) Changes in Prepaid Expenses $ (19,659.78) Changes in Accumulated Depreciation $ 156,023.56 Changes in Accounts Payable $ 127,018.91 Changes in FICA Withholding Payable $ - Changes in Federal Withholding Payable $ - Changes in State Withholding Payable $ Changes in State Tax Payable $ - Total Change in Cash from Operating Activities 8 28,795.81 Cash Flows from Investing Activities Changes in Property & Equipment $(308,150.84) Changes in Notes Receivable Employee $ - Changes in Notes Receivable - Dr. Jones $ (56,020.51) Total Change in Cash from Investing Activities $ (364,171.35) Cash Flows from Financing Activities Changes in Notes Payable $ 326,783.95 Common Stock $ 25,000.00 Retained Earnings $ (22,866.50) Total Change in Cash from Financing Activities 8 328,917.45 Net Increase/ (Decrease) in Cash 25 (6,458.09) Beginning Cash 53 - Ending Cash 8 (6,458.09) Page 1 3 Scott Wandler, University of New Orleans, swandler@uno.cdu Kevin Watson, Iowa State University, kwatson@iastate.edu Case 1]) 030501 International Research Journal of Applied Finance ISSN 2229 - 6891 May, 2012 Case Study Series in the day to day operation of the practice. Specifically, PMI was responsible for marketing, public relations, staffing (including the recruitment, hiring, and supervision of the Business Office Manager), and administration of the company's corporate compliance plan, as well as for providing unaudited financial statements including an Income Statement, Balance Sheet, and Cash Flow Statement. To compensate PMI, Sunset agreed to pay a monthly management fee equal to four percent of monthly net revenue, determined on the accrual basis. Net revenue was determined based on gross billed revenue less contractual allowances and a reasonable allowance for uncollectable accounts. Additionally, Sunset agreed to pay a billing and collection fee equal to five percent of company's monthly net receivables. Physicians Management Inc. - Mid-Year Performance Review PMI began administration of Sunset in February of 2011 and immediately began making changes to the practice. Under PMI management, Sunset borrowed $100,000; using the note and cash on hand to purchase a new X-Ray machine at a cost $171,145. In accordance with the contract, Jackson and Associates was taken off retainer and PMI provided Dr. Jones with the Income Statement, Balance Sheet, and Statement of Cash flows for the six months ended June 30, 2011 (Exhibits 5, 6, and 7). With the six month financial statements in hand, Mr. Wilson informed Dr. Jones of the increased revenues and cash flows. Citing these increased revenues and cash flows, Mr. Wilson asked Dr. Jones to give PMI more control of the company, including power to terminate employees. Dr. Jones granted the additional power and PMI immediately terminated the contracts of both the office manager and the billing secretary. Within days, PMI hired Jack Johnson, Mr. Wilson's son-in-law, as the new Business Office Manager. Physicians Management Inc. - 2011 Year End Performance Review In the beginning of 2012, PMI released Sunset Medical's 2011 financial statements to Dr. Jones. The financial statements indicated that under PMI management, Sunset increased revenues from $1,167,041 in 2010 to $1,601,050 in 2011. However, despite earning more than $400,000 in additional revenue, Sunset's cash had fallen dramatically during the year. In fact, Dr. Jones had borrowed $200,000 during the year, including the $100,000 utilized to purchase the X-Ray machine. Exhibits 8, 9, and 10 show the year ended December 31, 2011 Income Statement, Balance Sheet, and Statement of Cash Flows as released by PMI. Upon receiving Sunset's financial statements from PMI in January of 2012, Dr. Jones began analysis of Sunset's business practices to determine why the company was required to borrow a significant amount of money to maintain a positive cash flow. While the X-Ray machine had cost in excess of $175,000, Dr. Jones was at a loss to explain the need to borrow an additional $200,000, especially in light of an additional $400,000 in revenue. Dr. Jones has asked you to utilize the Financial Statements prepared by Jackson and Associates and PMI as well as the contract between Sunset Medical and PMI to determine whether Sunset should retain PMI's management and billing services for 2012 or terminate the contract. Is Physicians Medical Inc. acting in the best interest of Sunset Medical, P.C.? Did actual revenues jump by over $400,000 in 2011? Are the Financial Statements prepared by PMI correct? Is there sufficient motivation for PMI to provide the services needed to support Sunset Medical, P.C.? What ethical dilemmas face PMI? Scott Wandler, University of New Orleans, swandler @uno.edu Page 3 Kevin Watson, Iowa State University, kwatson @ iastate.edu Case ID 030501International Research Journal of Applied Finance ISSN 2229 -6891 May, 2012 Case Study Series Exhibit 1 - Sunset Medical, P.C. Income Statement For Years Ended 2008, 2009, 2010 (Provided by Jackson and Associates, CPA) Sunset Medical, P.C. Income Statements For Years Ended, December 31, 2010 2009 2008 Revenues Medical Revenues * $1,167,041.88 $1,057,322.77 $802,864.47 Expenses Direct Expenses $758,738.98 $667,645.64 $465,250.49 General Expenses $393,330.15 $358,141.19 $331,243.98 Interest Expense $5,804.66 $3, 133.93 $5,289.70 Depreciation Expense $14,385.00 $14,832.92 $14,222.00 Total Expenses $1,172,258.79 $1,043,753.6 $816,006.17 Net Operating Income ($5,216.91) $13,569.09 ($13,141.70) Other Income $203.40 $615.25 $589.10 Other Expense $228.04) ($554.67) ($1,780.02) Total Other Income (Expense) ($24.64) $60.58 ($1, 190.92) Net Income ($5,241.55) $13,629.67 ($14,332.62) * Medical Revenues are listed net of Bad Debt Scott Wandler, University of New Orleans, swandler @ uno.edu Page5 Kevin Watson, Iowa State University, kwatson @ iastate.edu Case ID 030501International Research Journal of Applied Finance ISSN 2229 -6891 May, 2012 Case Study Series Exhibit 2 - Sunset Medical, P.C. Balance Sheet For December 31, 2008, 2009, 2010 (Provided by Jackson and Associates, CPA) Sunset Medical, P.C. Balance Sheet December 31, 2010 2009 2008 Assets Cash $1,719.87 $1,304.84 $6,472.12 Accounts Receivable $450,797.12 $568,221.88 $335,879.95 Less: Allowance for Bad Debts ($450,797.12) ($568,221.88) ($335,879.95) Accounts Receivable, Net $ $ $ Accounts Receivable, Other $ $25,000.00 Prepaid Expenses $81,946.82 $ $1,282.96 Notes Receivable - Employee $4,283.70 $5, 753.70 $6,853.70 Notes Receivable - Dr. Jones $57,904.35 $58,483.69 $58,483.69 Property & Equipment $132,623.19 $127,641.97 $123,303.75 Less: Accumulated Depreciation ($121,876.00) ($107,491.00) $92,658.00) Property & Equipment, Net $10,747.19 $20,150.97 $30,645.75 Total Assets $156,601.93 $85,693.20 $128,738.22 Liabilities Accounts Payable $ $ $ FICA Withholding Payable $1,666.69 $3,653.57 $753.13 Federal Withholding Payable $24,835.27 $64,544.28 $10,113.58 State Withholding Payable $2,486.00 $10,1 10.00 $3,231.00 State Tax Payable $9.76 $10.30 $11.06 Notes Payable $125,470.71 $ $120,884.07 Total Liabilities $154,468.43 $78,318.15 $134,992.84 Stockholders' Equity Common Stock $25,000.00 $25,000.00 $25,000.00 Retained Earnings ($22,866.50) $17,624.95) ($31,254.62) Total Stockholders' Equity $2, 133.50 $7,375.05 ($6,254.62) Total Liabilities + Stockholders' Equity $156,601.93 $85,693.20 $128,738.22 Scott Wandler, University of New Orleans, swandler @uno.edu Page6 Kevin Watson, Iowa State University, kwatson @ iastate.edu Case ID 030501International Research Journal of Applied Finance ISSN 2229 6891 May, 2012 Case Study Series Exhibit 3: Authority and Responsibility of Medical Management Inc. 1.1 1.2 1.3 1.4 Engagement; company engages PMI to perform the functions and to provide services described in this agreement and PMI accepts the engagement under the terms and conditions set forth in this agreement. General; PMI shall serve as manager of the practice. Subject to limitations and condition set forth in this agreement, PMI, as manager of the practice shall conduct, supervise, and otherwise mange the day-to-day operations of the practice on behalf of and for the account of the company. In the absence of written directions from the Chief Executive Officer with respect to any matter, PMI shall exercise reasonable business judgment in its management activities and operation of the practice Business Office Manager: PMI shall assist company with the recruitment, hiring, and supervision of a Business Office Manager of the practice who will be an employee of the company provided that the CEO shall have the right to approve the hiring and termination of the Business Office Manager. The Business Office Manager should report to the company and shall confer, consult, and cooperate with PMI regarding implementation of the office management and business management services set forth in this agreement. The Business Office Manager shall work primarily onsite at the practice and shall be primarily responsible for the following facets of administration of the business of the company: 1.3.1 Day to day operation of the practice 1.3.2 Marketing of the practice 1.3.3 Public relations of the practice with patients and the community 1.3.4 Staffing and scheduling for the practice 1.3.5 Effective utilization of the practice's facilities 1.3.6 Administration of the company's corporate compliance plan 1.3.7 Implementation of policies of the company PMI will be responsible for preparation of unaudited financial statements 1.4.1 Income Statement 1.4.2 Balance Sheet 1.4.3 Cash Flow Statement Exhibit 4: Compensation of Medical Management Inc. 2.1 2.2 Monthly Management Fee: To compensate PMI and its affiliates for the provision of planning, management and other services, the company shall pay PMI a monthly management fee equal to four percent (4%) of monthly net revenue of company for the respective month, determined on the accrual basis. For the purpose of the monthly net revenue shall mean gross billed revenue less (a) contractual allowances, and (b) a reasonable allowance for uncollectable accounts. Billing and Collection Fee: To compensate PMI for the provision of billing and collection services under this agreement, the company shall pay PMI a monthly billing and collection fee equal to five percent (5%) of company's monthly net receivables as defined in section 2.1 above. Scott Wandler, University of New Orleans, swandler@uno.edu Kevin Watson, Iowa State University, kwatson@iastate.edu Case 1]) 030501 Page 7 International Research Journal of Applied Finance ISSN 2229 - 6891 May, 2012 Case Study Series Exhibit 5 - Income Statement for Six Months Ended June 30, 2011 (Prepared by PMI) Sunset Medical, P.C. Income Statements For Six Months Ended, June 30, 2011 Revenues Medical Revenues $ 961,039.73 Expenses Direct Expenses $ 363, 102.36 General Expenses $ 247,513.39 Interest Expense $ 5,287.74 Depreciation Expense $ 12,655.31 Total Expense $ 628,558.80 Net Operating Income $ 332,480.93 Other Income $ 3,416.38 Other Expense $ (15,890.77) Total Other Income (Expense) $ (12,474.39) Net Income $ 320,006.54 Scott Wandler, University of New Orleans, swandler @ uno.edu Page8 Kevin Watson, Iowa State University, kwatson @ iastate.edu Case ID 030501International Research Journal of Applied Finance ISSN 2229 - 6891 May, 2012 Case Study Series Exhibit 6 - Balance Sheet as of June 30, 2011 (Prepared by PMI) Sunset Medical, P.C. Balance Sheet June 30, 2011 Assets Cash $ 53,614.43 Accounts Receivable $ 313,627.76 Less: Allowance for Bad Debts Accounts Receivable, Net $ 313,627.76 Accounts Receivable, Other $ Prepaid Expenses $ 24,868.15 Notes Receivable - Employee $ Notes Receivable - Dr. Jones $ 62,324.50 Property & Equipment $ 303,768.48 Less: Accumulated Depreciation $(134,531.31) Property & Equipment, Net $ 169,237.17 Total Assets $ 623,672.01 Liabilities Accounts Payable $ 77,086.48 FICA Withholding Payable $ Federal Withholding Payable $ State Withholding Payable $ State Tax Payable Notes Payable $ 224,445.51 Total Liabilities $ 301,531.99 Stockholders' Equity Common Stock $ 25,000.00 Retained Earnings $ 297,140.04 Total Stockholders' Equity $ 322,140.04 Total Liabilities + Stockholders' Equity $ 623,672.03 Scott Wandler, University of New Orleans, swandler @uno.edu Page Kevin Watson, Iowa State University, kwatson @iastate.edu Case ID 030501International Research Journal of Applied Finance ISSN 2229 6891 Case Study'Series May, 2012 Exhibit 7 - Statement of Cash Flows for Six Months Ended June 30, 2011 (Prepared by PMI) Sunset Medical, P.C. Statements of Cash Flows For Six Months Ended, June 30, 2011 Cash Flows From Operating Activities Net Income (Loss) $ 320,006.52 Changes in Accounts Receivable, Net $613,627.76) Changes in Accounts Receivable, Other 8 Changes in Prepaid Expenses $ (24,868.15) Changes in Accumulated Depreciation $ 134,531.31 Changes in Accounts Payable $ 77,086.48 Changes in FICA Withholding Payable $ - Changes in Federal Withholding Payable $ - Changes in State Withholding Payable $ Changes in State Tax Payable $ - Total Change in Cash from Operating Activities $ 193,128.40 Cash Flows from Investing Activities Changes in Property & Equipment $(303,768.48) Changes in Notes Receivable Employee $ - Changes in Notes Receivable - Dr. Jones $ (62,324.50) Total Change in Cash from Investing Activities $ (366,092.98) Cash Flows from Financing Activities Changes in Notes Payable $ 224,445.51 Common Stock $ 25,000.00 Retained Earnings $ (22,866.50) Total Change in Cash from Financing Activities $ 226,579.01 Net Increase / (Decrease) in Cash $ 53,614.43 Beginning Cash 39 - Ending Cash $_ 53,614.43 Page 1 0 Scott Wandler, University of New Orleans, swandler@uno.edu Kevin Watson, Iowa State University, kwatson@iastate.edu Case ID 030501 International Research Journal of Applied Finance ISSN 2229 - 6891 May, 2012 Case Study Series Exhibit 8 - Income Statement for Year Ended December 31, 2011 (Prepared by PMI) Sunset Medical, P.C. Income Statements For Year Ended December 31, 2011 Revenues Medical Revenues $ 1,601,050.52 Expenses Direct Expenses* * * $ 719,880.70 General Expenses $ 567,372.88 Interest Expense $ 16,690.68 Depreciation Expense $ 34,147.56 Total Expense $ 1,338,091.82 Net Operating Income $ 262,958.70 Other Income $ 4,261.93 Other Expense $ (36,050.84) Total Other Income (Expense) $ (31,788.91) Net Income $ 231,169.79 Scott Wandler, University of New Orleans, swandler @uno.edu Page 1 1 Kevin Watson, Iowa State University, kwatson @ iastate.edu Case ID 030501