Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Need question 5 for this post. Questions 4 to 6 are based on the following information: Suppose currently there are three banks offering the following

Need question 5 for this post.

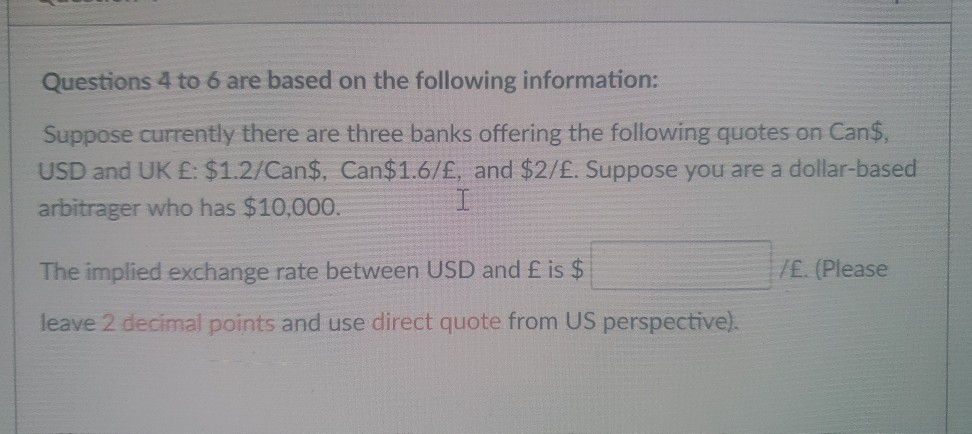

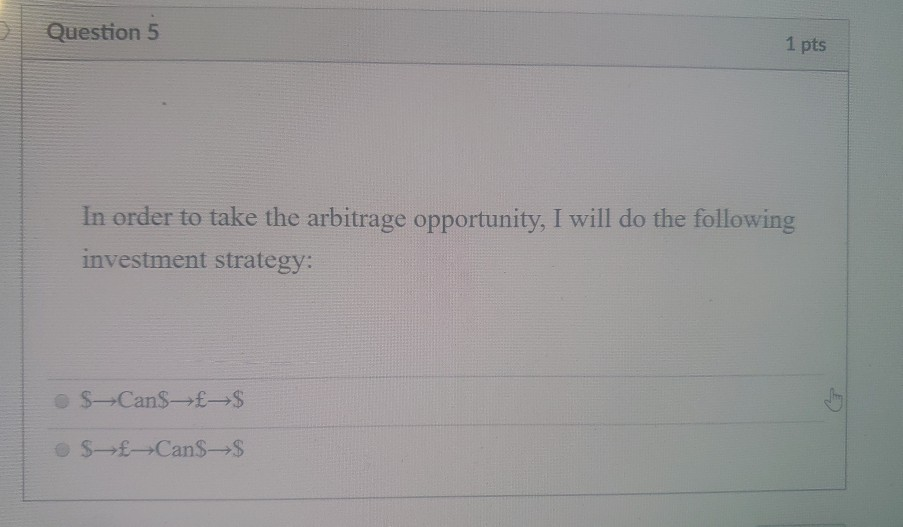

Questions 4 to 6 are based on the following information: Suppose currently there are three banks offering the following quotes on Can$, USD and UK : $1.2/Can$, Can$1.6/, and $2/. Suppose you are a dollar-based arbitrager who has $10,000. The implied exchange rate between USD and E is$ /E. (Please leave 2 decimal points and use direct quote from US perspective). Question 5 1 pts In order to take the arbitrage opportunity, I will do the following investment strategy

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

15th edition

77861612, 1259194078, 978-0077861612, 978-1259194078