Question

Negative interest rates are real, but don't expect to get paid... by James Peltz Negative interest rates are a real thing. But dont expect your

Negative interest rates are real, but don't expect to get paid...

by James Peltz

Negative interest rates are a real thing. But don’t expect your local bank to start paying you to borrow money.

President Trump kicked a hornet’s nest this week when he tweeted that the Federal Reserve should cut interest rates “to zero, or less.” He was reacting to the growing volume of foreign government bonds and other debt instruments — now totaling $15 trillion — that carry negative yields. Most have been issued by governments in Western Europe and Asia in hopes of kick-starting their stagnant economies.

Trump apparently believes that the United States, thanks to “boneheads” at the Fed, is missing a chance to refinance its debt at ultra-low cost. Citing possibly severe reaction by markets, some financial experts called his suggestion “a recipe for disaster.”

When bond rates go negative, the trickle-down effect on consumers can be jarring. Two Scandinavian banks recently offered fixed-rate mortgages that charge either no interest or a negative 0.5% interest, meaning that — if you don’t count various fees — the mortgage holders would pay back less than they originally borrowed.

But in the United States, rates remain well above zero on mortgages and other debt and probably will stay that way, analysts said.

“It’s just not relevant here in the U.S.; this is much ado about nothing,” said Greg McBride, chief financial analyst at Bankrate.com. “We’re a long, long way from this” in the United States, he said.

To be sure, interest rates also are generally falling in the United States, spurred in part by concern about the U.S. economy’s growth slowing and the Federal Reserve’s decision in July to cut its benchmark short-term lending rate for the first time since the severe recession a decade ago.

The Fed had kept its rate near zero to help pull the nation out of that recession, then lifted the rate nine times starting in late 2015. The Fed’s most recent quarter-point cut lowered the rate to a range of 2.25% to 2.5%, and many expect another cut next week as the central bank tries to keep the long-running U.S. economic expansion intact.

But concerns about the economy’s outlook persist while inflation remains low, two reasons Treasury bond prices have risen and their yields have dropped in recent months as investors sought alternatives to riskier investments such as stocks. The yield on a 10-year Treasury bond, for instance, has tumbled to 1.90% on Friday from nearly 3% a year ago.

In turn, rates on home mortgages and new-car loans have moved lower this year. The average rate on a 30-year, fixed-rate mortgage is 3.56%, down from 4.51% at the start of the year, according to Freddie Mac. The rate on a five-year loan for a new car has dropped to 4.62% from 4.96%, Bankrate data show.

“Those rates are still a long way from zero,” said David Ely, associate dean at San Diego State’s Fowler College of Business. Even if lending costs keep slipping, “I would not expect negative rates,” he said.

The spread of negative rates overseas and lower U.S. rates is little comfort for Americans with credit-card balances: The average interest rate on the cards is 17.8%, and it hasn’t budged much in the last year, according to Bankrate. Credit-card rates are that high in part because card issuers are lending money that’s unsecured — meaning it doesn’t require collateral — and because credit-card balances often are among the debts first nullified when people file for bankruptcy, McBride said.

The low-rate environment also has kept a lid on earnings for American savers for the last few years. A one-year certificate of deposit now yields an average of 0.85%, Bankrate figures show. (Some online-only banks pay more.) Still, that’s up from 0.30% three years ago.

“It’s a terrible time to be a saver,” Ely said.

Countries such as Germany, Denmark and Japan are among those who have issued debt securities in recent years that now carry a negative yield, usually because the securities’ prices have been bid higher and that sent their low coupon rates below zero. Bond prices move inversely to their yields, so when a bond’s price goes up, its yield falls.

Then last month, Germany sold 30-year bonds with a zero-interest coupon. And because there was ample demand for the bonds, the bonds’ prices rose and thereby pushed their yields into negative territory.

Germany and the other countries have issued such debt in hopes of keeping lending costs so low that it sparks growth in their struggling economies.

Trump took notice of the negative rates overseas to buttress his argument that the Federal Reserve should further lower U.S. interest rates to boost the U.S. economy and keep America competitive in trade. “Germany is actually ‘getting paid’ to borrow money,” he tweeted last month after the G-7 summit. But unlike Germany, the United States has an economy that’s still growing.

Regardless, why would anyone buy a government bond that’s yielding negative interest, much less bid its price higher?

“Because it’s the ultimate safe haven, where you’re willing to pay the government to store your money” if you’re skittish about riskier investments such as stocks, McBride said. “You’re willing to pay that to minimize your losses.”

In addition, institutional investors such as pension funds and insurance companies often have policies requiring them to keep a portion of their investment portfolios in government bonds, even if those investments are carrying a negative yield, analysts said.

Peter Heilbron, chief executive of Trace Wealth Advisors in Sherman Oaks, said there also are reasons those investors don’t shift a lot of their assets from bonds to other so-called havens such as gold and short-term money-market funds.

Even if they’re trading with a negative yield, the bonds provide a locked-in principal amount and coupon interest rate for an extended period, whereas gold prices and money-market yields constantly fluctuate, he said.

That certainty is key for pension funds and insurers, Heilbron said. “If I know I have to fund a future liability, and I can lose a little bit of money along the way [with negative yields] to be able to fund it, I’m going to buy the safer asset versus speculating on a riskier asset like gold that does not have a known outcome at a specified date,” he said.

For American consumers, meanwhile, the trend toward lower rates means “it’s a great time to go into a mortgage or borrow for a car, especially if you have a good credit rating,” Ely said.

But Americans should hope U.S. rates never drop so low that they go negative, because negative rates would mean that the U.S. economy has run into severe problems, McBride said.

“The idea of negative interest rates sounds quirky, and to borrowers it sounds like fun, but the economic backdrop that would create such a scenario is not something we want to wish for,” he said.

Part 1

Suppose that inflation is 2%. According to the data given in the article, what is the new real rate of interest on a 5-year car loan? Give your answer to two decimals. _____ %

Part 3

It may seem odd, but why would anyone buy bonds if they have a negative interest rate?

Choose one or more:

A. Some pension funds are required to keep a portion of their portfolios in government bonds.

B. Government bonds are almost riskless.

C. The prices of alternative "safe" assets like gold do not change very much.

D. People who buy these bonds wish to help the government pay down debt at a lower cost.

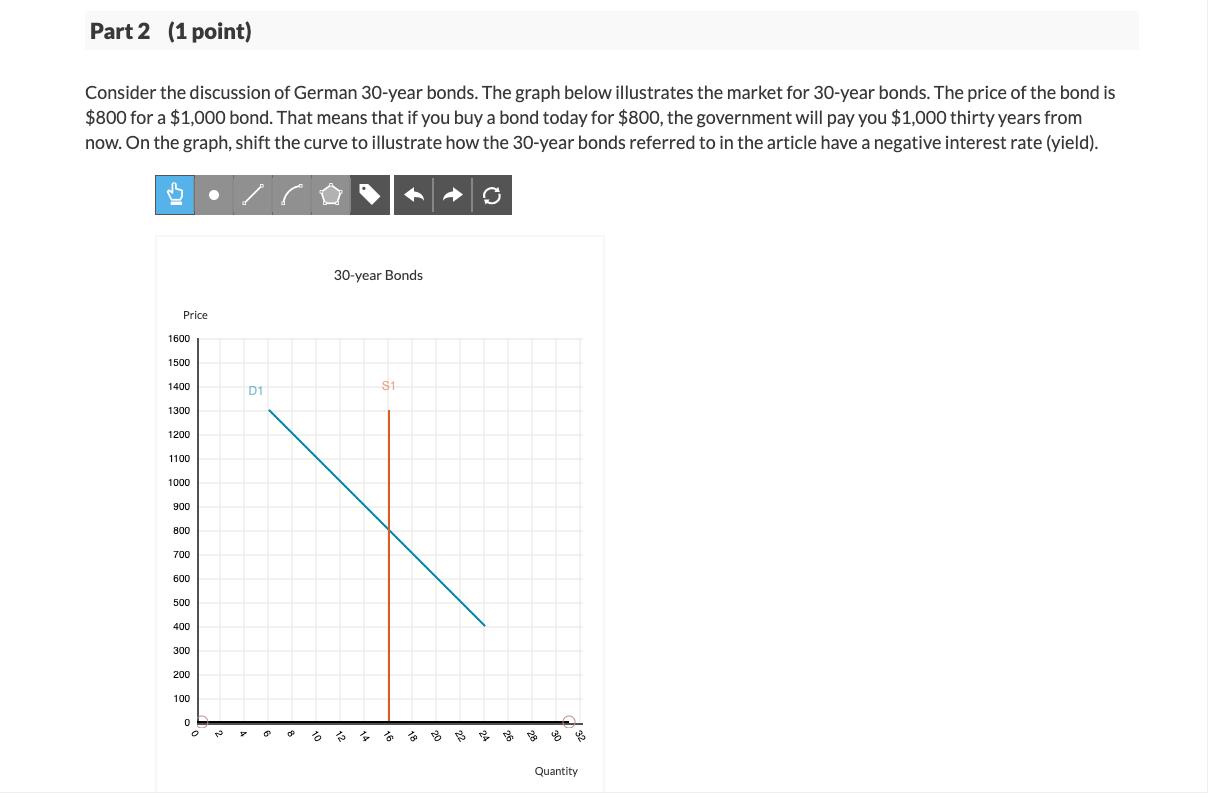

Part 2 (1 point) Consider the discussion of German 30-year bonds. The graph below illustrates the market for 30-year bonds. The price of the bond is $800 for a $1,000 bond. That means that if you buy a bond today for $800, the government will pay you $1,000 thirty years from now. On the graph, shift the curve to illustrate how the 30-year bonds referred to in the article have a negative interest rate (yield). 30-year Bonds Price 1600 1500 1400 S1 D1 1300 1200 1100 1000 900 800 700 600 500 400 300 200 100 Quantity

Step by Step Solution

There are 3 Steps involved in it

Step: 1

part 1 An inflation rate is just the percentage change in a price index An inflation rate can be computed for any price index using the general equation for percentage changes between two years whethe...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

10th edition

978-0077511388, 78034779, 9780077511340, 77511387, 9780078034770, 77511344, 978-0077861759