Answered step by step

Verified Expert Solution

Question

1 Approved Answer

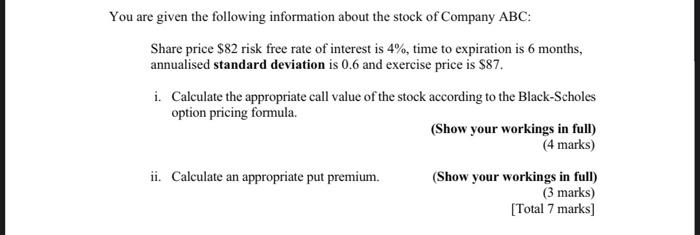

NO EXCEL PLEASE, NEED TO SHOW WORKINGS WITH FINANCE FORMULAS IN WORD OR HANDWRITTEN You are given the following information about the stock of Company

NO EXCEL PLEASE, NEED TO SHOW WORKINGS WITH FINANCE FORMULAS IN WORD OR HANDWRITTEN

You are given the following information about the stock of Company ABC: Share price $82 risk free rate of interest is 4%, time to expiration is 6 months, annualised standard deviation is 0.6 and exercise price is $87. i. Calculate the appropriate call value of the stock according to the Black-Scholes option pricing formula (Show your workings in full) (4 marks) ii. Calculate an appropriate put premium. (Show your workings in full) (3 marks) [Total 7 marks] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Business Finance

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

13th edition

132743469, 978-0132743464