Answered step by step

Verified Expert Solution

Question

1 Approved Answer

No excel please show your work. Thanks. Problem # 4: [This problem is from notes of Professor Michael Gibbons and Professor Haluk Unal?.] Today is

No excel please show your work. Thanks.

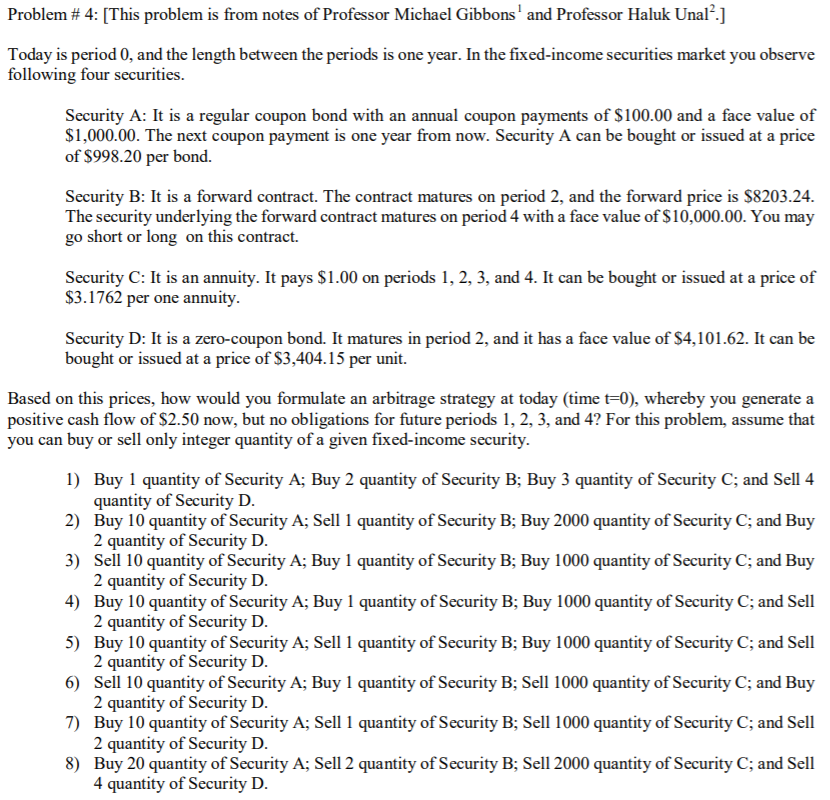

Problem # 4: [This problem is from notes of Professor Michael Gibbons and Professor Haluk Unal?.] Today is period 0, and the length between the periods is one year. In the fixed-income securities market you observe following four securities. Security A: It is a regular coupon bond with an annual coupon payments of $100.00 and a face value of $1,000.00. The next coupon payment is one year from now. Security A can be bought or issued at a price of $998.20 per bond. Security B: It is a forward contract. The contract matures on period 2, and the forward price is $8203.24. The security underlying the forward contract matures on period 4 with a face value of $10,000.00. You may go short or long on this contract. Security C: It is an annuity. It pays $1.00 on periods 1, 2, 3, and 4. It can be bought or issued at a price of $3.1762 per one annuity. Security D: It is a zero-coupon bond. It matures in period 2, and it has a face value of $4,101.62. It can be bought or issued at a price of $3,404.15 per unit. Based on this prices, how would you formulate an arbitrage strategy at today (time t=0), whereby you generate a positive cash flow of $2.50 now, but no obligations for future periods 1, 2, 3, and 4? For this problem, assume that you can buy or sell only integer quantity of a given fixed-income security. 1) Buy 1 quantity of Security A; Buy 2 quantity of Security B; Buy 3 quantity of Security C; and Sell 4 quantity of Security D. 2) Buy 10 quantity of Security A; Sell 1 quantity of Security B; Buy 2000 quantity of Security C; and Buy 2 quantity of Security D. 3) Sell 10 quantity of Security A; Buy 1 quantity of Security B; Buy 1000 quantity of Security C; and Buy 2 quantity of Security D. 4) Buy 10 quantity of Security A; Buy 1 quantity of Security B; Buy 1000 quantity of Security C; and Sell 2 quantity of Security D. 5) Buy 10 quantity of Security A; Sell 1 quantity of Security B; Buy 1000 quantity of Security C; and Sell 2 quantity of Security D. 6) Sell 10 quantity of Security A; Buy 1 quantity of Security B; Sell 1000 quantity of Security C; and Buy 2 quantity of Security D. 7) Buy 10 quantity of Security A; Sell 1 quantity of Security B; Sell 1000 quantity of Security C; and Sell 2 quantity of Security D. Buy 20 quantity of Security A; Sell 2 quantity of Security B; Sell 2000 quantity of Security C; and Sell 4 quantity of Security D. Problem # 4: [This problem is from notes of Professor Michael Gibbons and Professor Haluk Unal?.] Today is period 0, and the length between the periods is one year. In the fixed-income securities market you observe following four securities. Security A: It is a regular coupon bond with an annual coupon payments of $100.00 and a face value of $1,000.00. The next coupon payment is one year from now. Security A can be bought or issued at a price of $998.20 per bond. Security B: It is a forward contract. The contract matures on period 2, and the forward price is $8203.24. The security underlying the forward contract matures on period 4 with a face value of $10,000.00. You may go short or long on this contract. Security C: It is an annuity. It pays $1.00 on periods 1, 2, 3, and 4. It can be bought or issued at a price of $3.1762 per one annuity. Security D: It is a zero-coupon bond. It matures in period 2, and it has a face value of $4,101.62. It can be bought or issued at a price of $3,404.15 per unit. Based on this prices, how would you formulate an arbitrage strategy at today (time t=0), whereby you generate a positive cash flow of $2.50 now, but no obligations for future periods 1, 2, 3, and 4? For this problem, assume that you can buy or sell only integer quantity of a given fixed-income security. 1) Buy 1 quantity of Security A; Buy 2 quantity of Security B; Buy 3 quantity of Security C; and Sell 4 quantity of Security D. 2) Buy 10 quantity of Security A; Sell 1 quantity of Security B; Buy 2000 quantity of Security C; and Buy 2 quantity of Security D. 3) Sell 10 quantity of Security A; Buy 1 quantity of Security B; Buy 1000 quantity of Security C; and Buy 2 quantity of Security D. 4) Buy 10 quantity of Security A; Buy 1 quantity of Security B; Buy 1000 quantity of Security C; and Sell 2 quantity of Security D. 5) Buy 10 quantity of Security A; Sell 1 quantity of Security B; Buy 1000 quantity of Security C; and Sell 2 quantity of Security D. 6) Sell 10 quantity of Security A; Buy 1 quantity of Security B; Sell 1000 quantity of Security C; and Buy 2 quantity of Security D. 7) Buy 10 quantity of Security A; Sell 1 quantity of Security B; Sell 1000 quantity of Security C; and Sell 2 quantity of Security D. Buy 20 quantity of Security A; Sell 2 quantity of Security B; Sell 2000 quantity of Security C; and Sell 4 quantity of Security DStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Jeff Madura

10th Edition

1439038333, 9781439038338