Answered step by step

Verified Expert Solution

Question

1 Approved Answer

No handwritings please. Thank you (b) You are considering to invest in three stocks listed in the Bursa Malaysia. The information about three stocks is

No handwritings please. Thank you

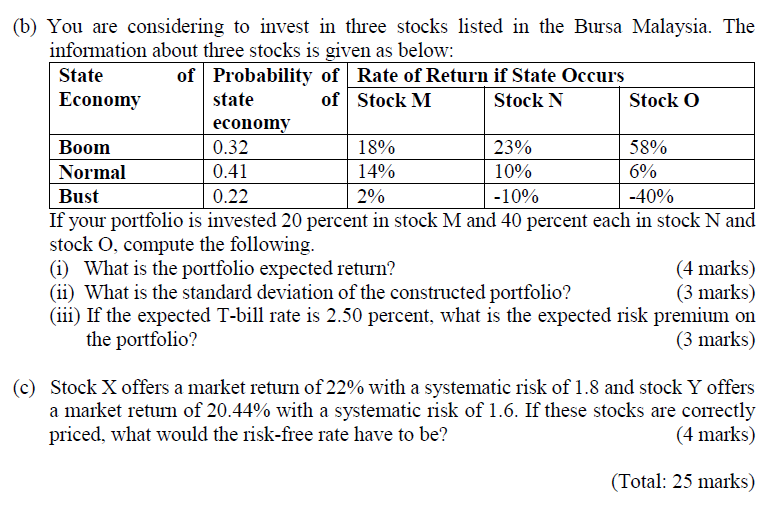

(b) You are considering to invest in three stocks listed in the Bursa Malaysia. The information about three stocks is given as below: State of Probability of Rate of Return if State Occurs Economy state of Stock M Stock N Stock O economy Boom 0.32 18% 23% 58% Normal 0.41 14% 10% 6% Bust 0.22 2% -10% -40% If your portfolio is invested 20 percent in stock M and 40 percent each in stock N and stock O, compute the following. (i) What is the portfolio expected return? (4 marks) (ii) What is the standard deviation of the constructed portfolio? (3 marks) (iii) If the expected T-bill rate is 2.50 percent, what is the expected risk premium on the portfolio? (3 marks) C) Stock X offers a market return of 22% with a systematic risk of 1.8 and stock Y offers a market return of 20.44% with a systematic risk of 1.6. If these stocks are correctly priced, what would the risk-free rate have to be? (4 marks) (Total: 25 marks) (b) You are considering to invest in three stocks listed in the Bursa Malaysia. The information about three stocks is given as below: State of Probability of Rate of Return if State Occurs Economy state of Stock M Stock N Stock O economy Boom 0.32 18% 23% 58% Normal 0.41 14% 10% 6% Bust 0.22 2% -10% -40% If your portfolio is invested 20 percent in stock M and 40 percent each in stock N and stock O, compute the following. (i) What is the portfolio expected return? (4 marks) (ii) What is the standard deviation of the constructed portfolio? (3 marks) (iii) If the expected T-bill rate is 2.50 percent, what is the expected risk premium on the portfolio? (3 marks) C) Stock X offers a market return of 22% with a systematic risk of 1.8 and stock Y offers a market return of 20.44% with a systematic risk of 1.6. If these stocks are correctly priced, what would the risk-free rate have to be? (4 marks) (Total: 25 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started