Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Notes: This question and answer is already from the chegg. It is not mine. why divided in 3/12 in part B? why divided in 4/12

Notes: This question and answer is already from the chegg. It is not mine.

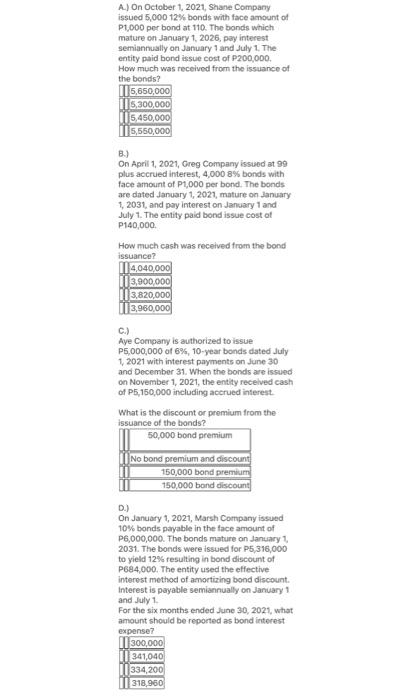

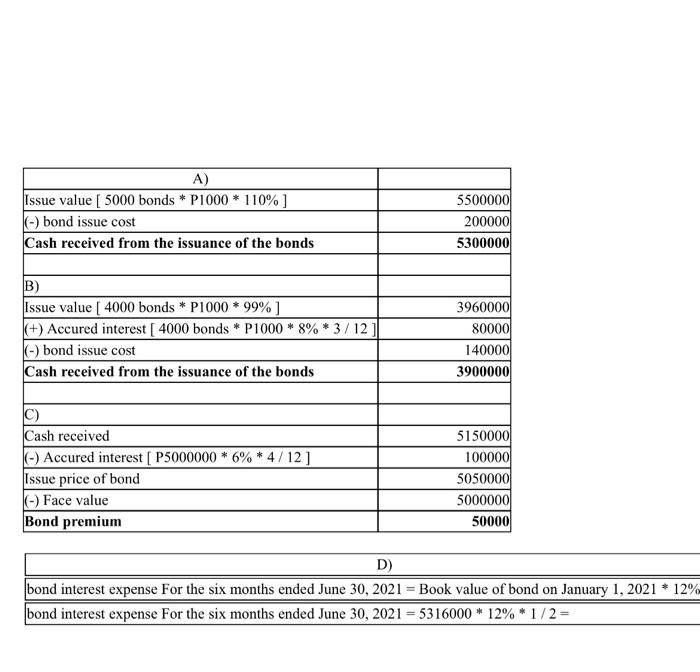

why divided in 3/12 in part B?

why divided in 4/12 in part C?

why divided in 1/2 in part D?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Employee Motivation Audit

Authors: Jane Weightman

1st Edition

0955970709, 978-0955970702