Answered step by step

Verified Expert Solution

Question

1 Approved Answer

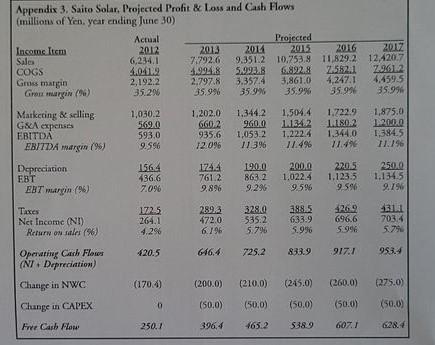

Number 1 and 2, plea Use the following assumptions to value Saito Solar based on the discounted cash flow method. Assume the Actual 2012 numbers

Number 1 and 2, plea

Use the following assumptions to value Saito Solar based on the discounted cash flow method. Assume the Actual 2012 numbers given in Appendix 3.

- For the next 5 years (2013-2017), the companys sales is expected to grow by 25% per year.

- All expenses (except depreciation) are expected to grow by 20% per year.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Best Retirement Guides For Adults Successful Techniques To Make Your Money Last A Lifetime

Authors: Rebecca W. Anderson

1st Edition

979-8865146025