Answered step by step

Verified Expert Solution

Question

1 Approved Answer

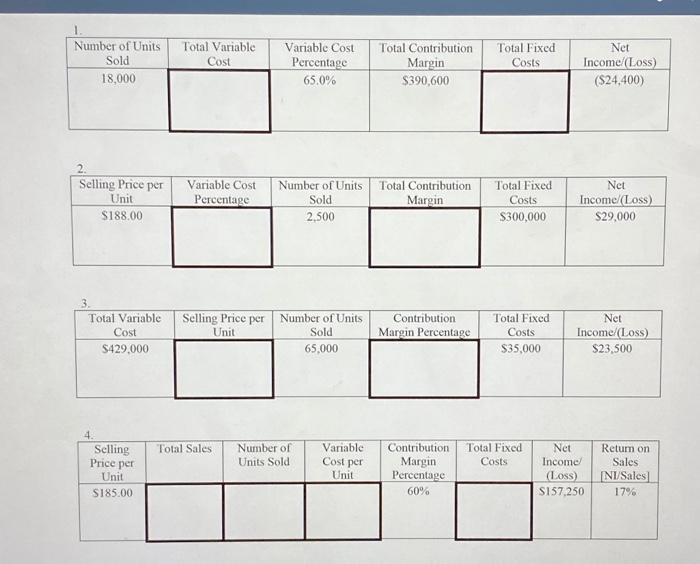

Number of Units Sold 18,000 Total Variable Cost Variable Cost Percentage 65.0% Total Contribution Margin $390,600 Total Fixed Costs Net Income/(Loss) (524,400) 2. Selling Price

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting Chapters 1-9

Authors: James A. Heintz, Robert W. Parry

22nd Edition

1305666186, 9781305666184