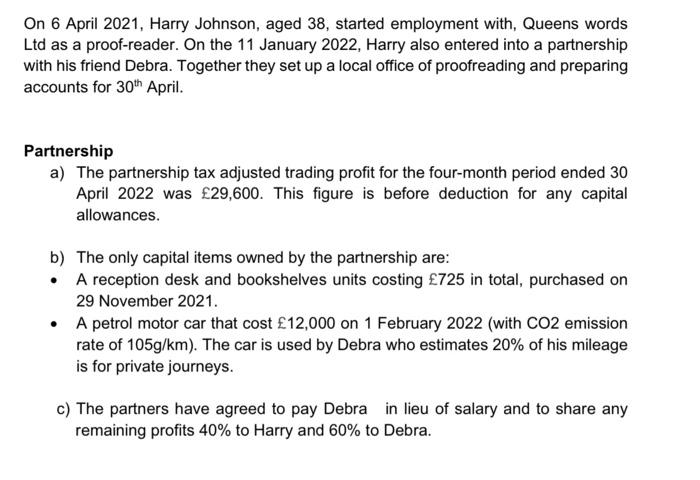

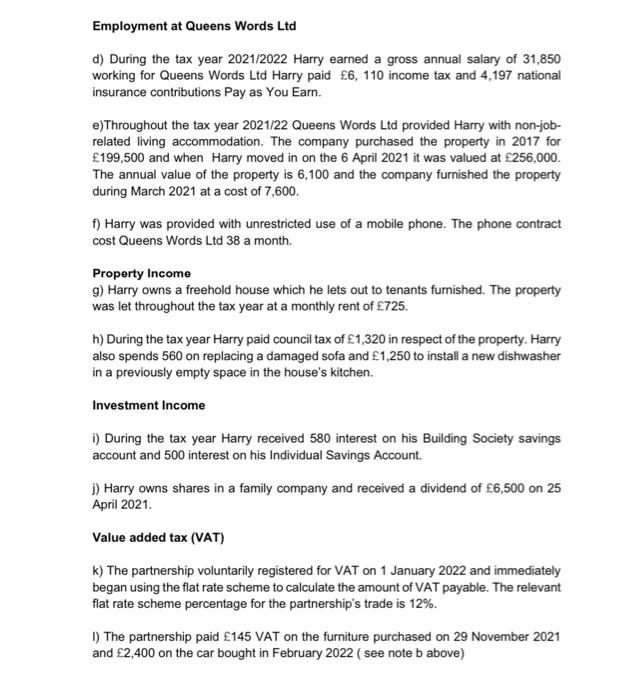

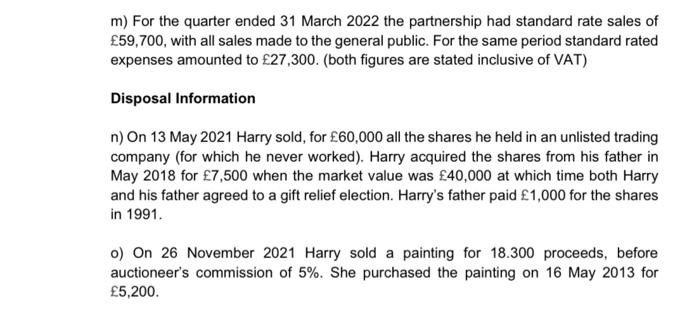

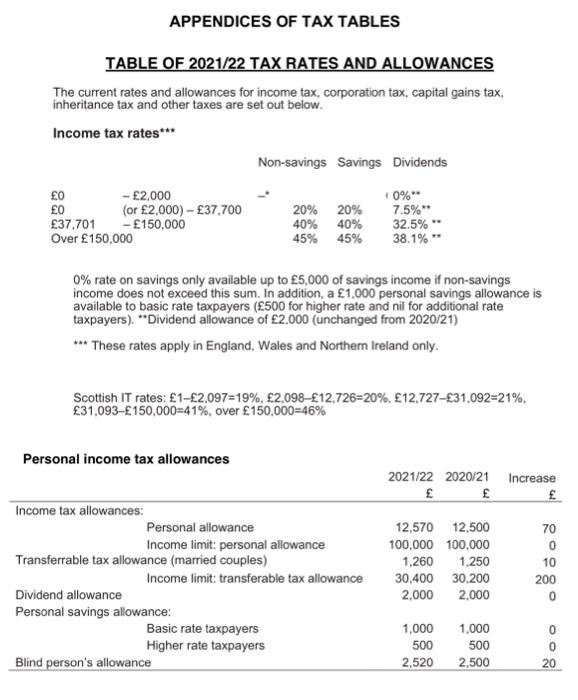

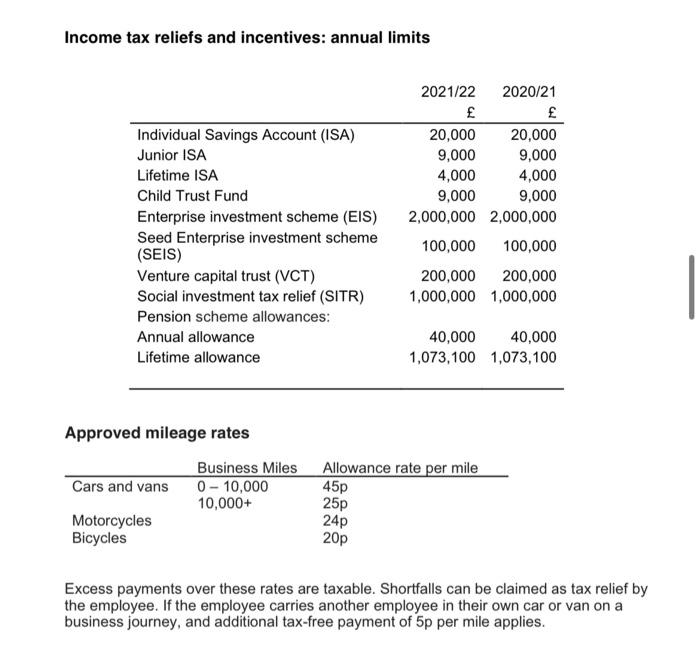

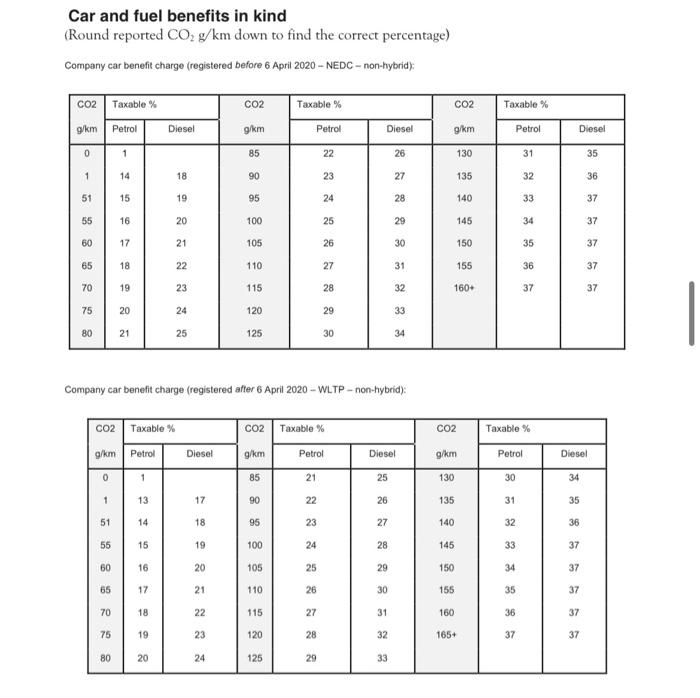

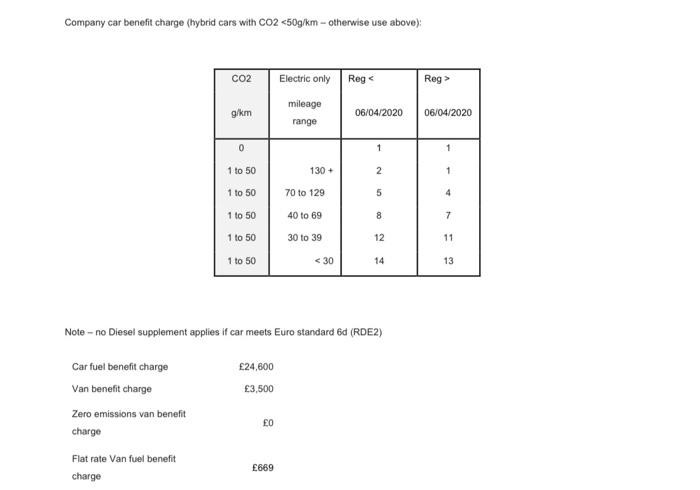

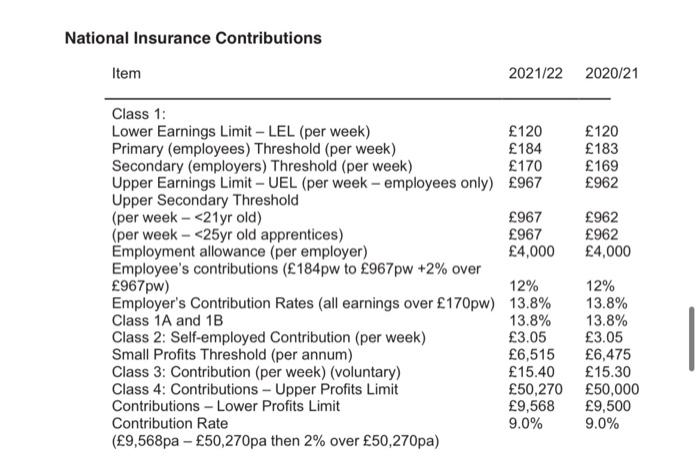

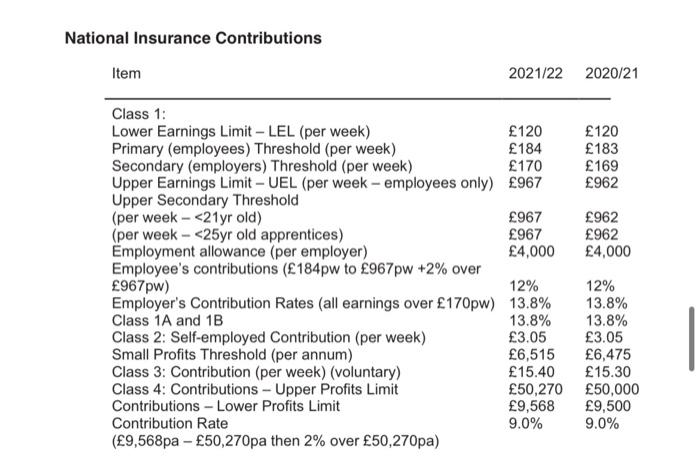

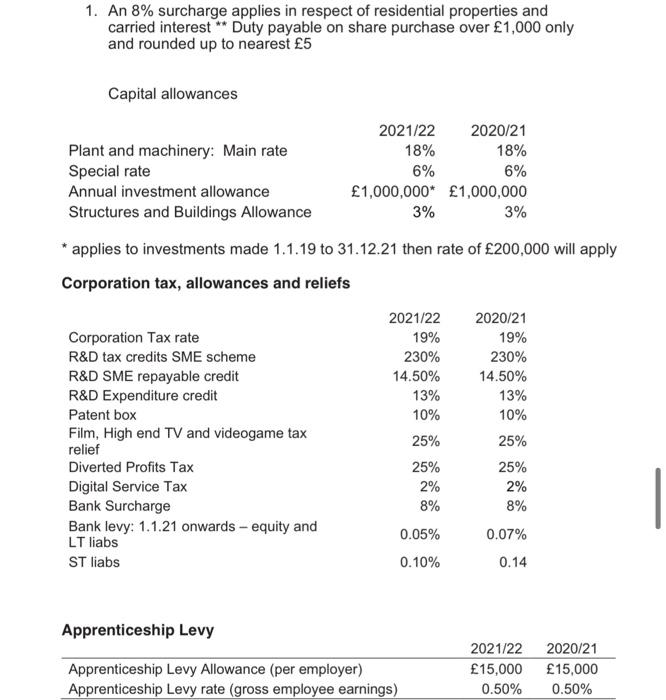

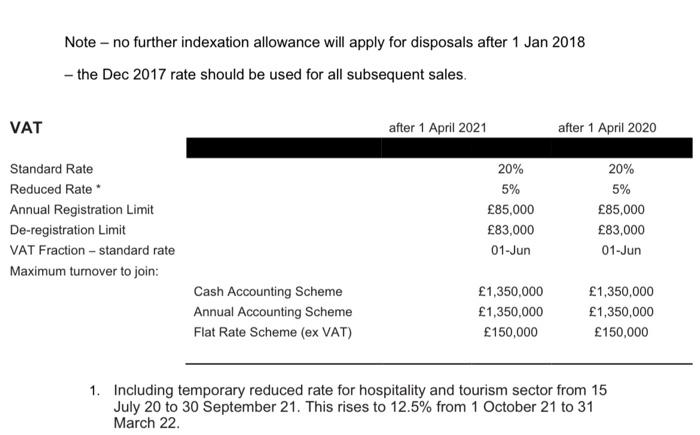

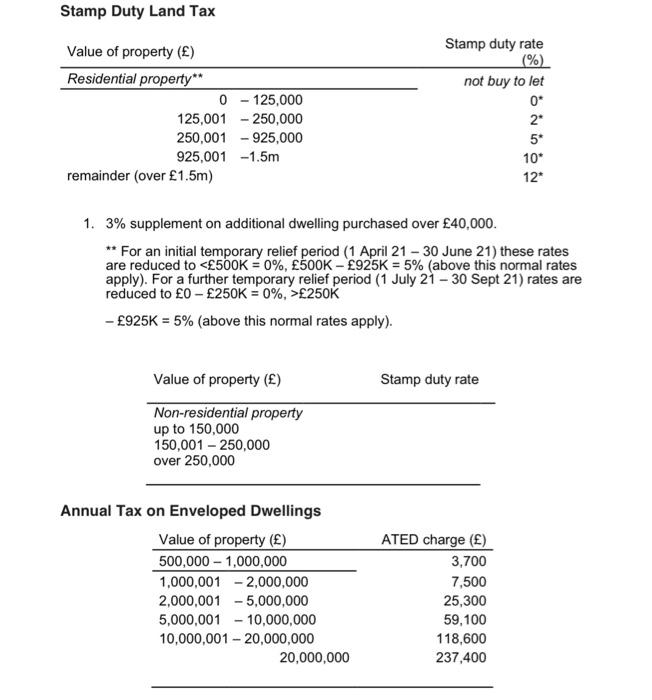

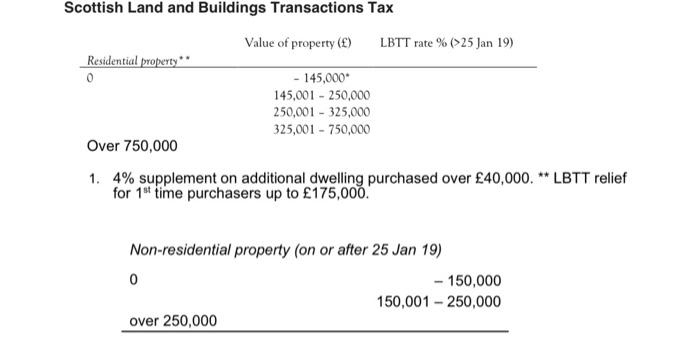

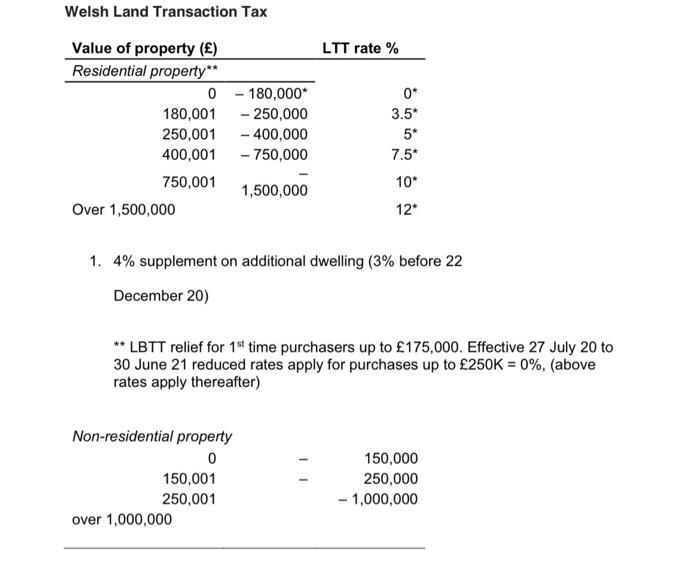

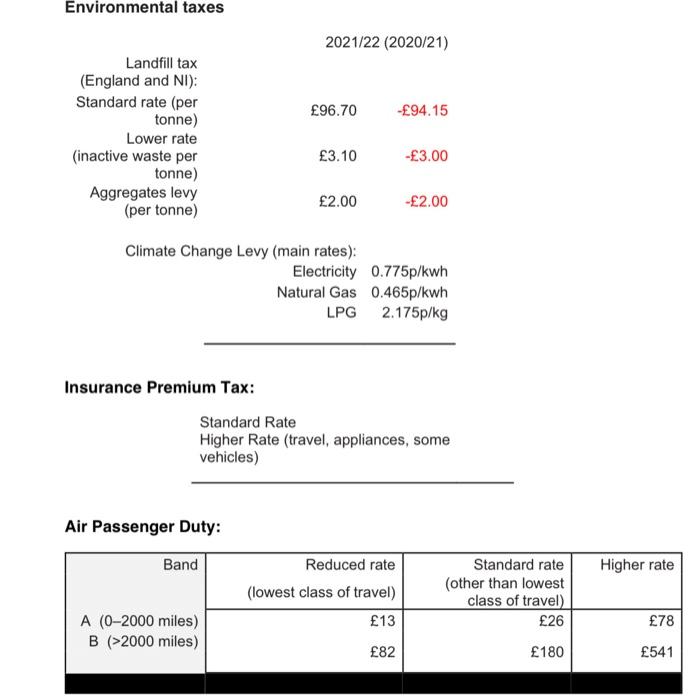

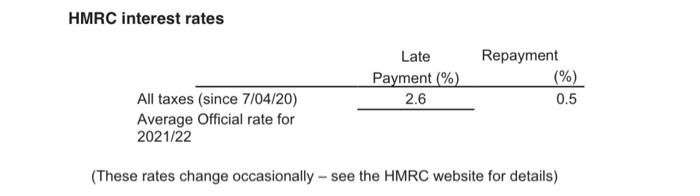

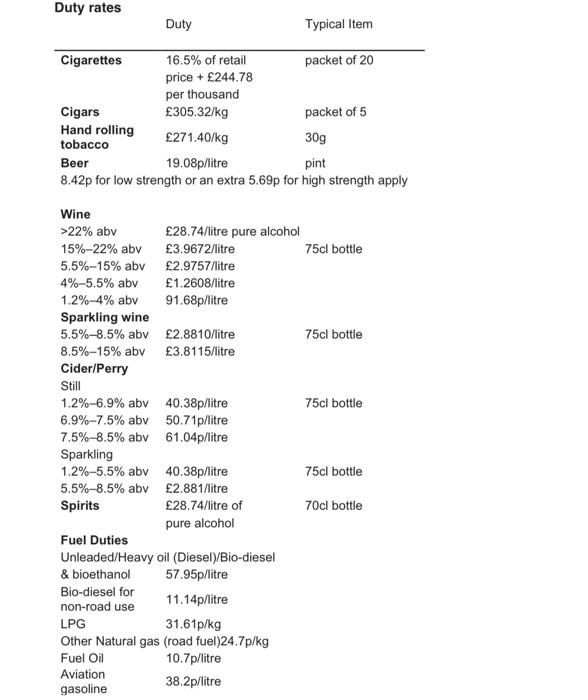

On 6 April 2021, Harry Johnson, aged 38, started employment with, Queens words Ltd as a proof-reader. On the 11 January 2022, Harry also entered into a partnership with his friend Debra. Together they set up a local office of proofreading and preparing accounts for 30th April. Partnership a) The partnership tax adjusted trading profit for the four-month period ended 30 April 2022 was 29,600. This figure is before deduction for any capital allowances. b) The only capital items owned by the partnership are: - A reception desk and bookshelves units costing 725 in total, purchased on 29 November 2021. - A petrol motor car that cost 12,000 on 1 February 2022 (with CO2 emission rate of 105g/km). The car is used by Debra who estimates 20% of his mileage is for private journeys. c) The partners have agreed to pay Debra in lieu of salary and to share any remaining profits 40% to Harry and 60% to Debra. Employment at Queens Words Ltd d) During the tax year 2021/2022 Harry earned a gross annual salary of 31,850 working for Queens Words Ltd Harry paid 6,110 income tax and 4,197 national insurance contributions Pay as You Earn. e)Throughout the tax year 2021/22 Queens Words Ltd provided Harry with non-jobrelated living accommodation. The company purchased the property in 2017 for 199,500 and when Harry moved in on the 6 April 2021 it was valued at 256,000. The annual value of the property is 6,100 and the company furnished the property during March 2021 at a cost of 7,600. f) Harry was provided with unrestricted use of a mobile phone. The phone contract cost Queens Words Ltd 38 a month. Property Income g) Harry owns a freehold house which he lets out to tenants furnished. The property was let throughout the tax year at a monthly rent of 725. h) During the tax year Harry paid council tax of 1,320 in respect of the property. Harry also spends 560 on replacing a damaged sofa and 1,250 to install a new dishwasher in a previously empty space in the house's kitchen. Investment Income i) During the tax year Harry received 580 interest on his Building Society savings account and 500 interest on his Individual Savings Account. j) Harry owns shares in a family company and received a dividend of 6,500 on 25 April 2021. Value added tax (VAT) k) The partnership voluntarily registered for VAT on 1 January 2022 and immediately began using the flat rate scheme to calculate the amount of VAT payable. The relevant flat rate scheme percentage for the partnership's trade is 12%. I) The partnership paid 145 VAT on the furniture purchased on 29 November 2021 and 2,400 on the car bought in February 2022 (see note b above) m) For the quarter ended 31 March 2022 the partnership had standard rate sales of 59,700, with all sales made to the general public. For the same period standard rated expenses amounted to 27,300. (both figures are stated inclusive of VAT) Disposal Information n) On 13 May 2021 Harry sold, for 60,000 all the shares he held in an unlisted trading company (for which he never worked). Harry acquired the shares from his father in May 2018 for 7,500 when the market value was 40,000 at which time both Harry and his father agreed to a gift relief election. Harry's father paid 1,000 for the shares in 1991. o) On 26 November 2021 Harry sold a painting for 18.300 proceeds, before auctioneer's commission of 5%. She purchased the painting on 16 May 2013 for 5,200. B3-Explain, with supporting calculations, whether or not it was beneficial for the partnership to have used the VAT flat rate schemes for the quarter ended 31 March 2022: (20\%) TABLE OF 2021/22 TAX RATES AND ALLOWANCES The current rates and allowances for income tax, corporation tax, capital gains tax, inheritance tax and other taxes are set out below. Income tax rates 0% rate on savings only available up to 5,000 of savings income if non-savings income does not exceed this sum. In addition, a 1,000 personal savings allowance is available to basic rate taxpayers ( 500 for higher rate and nil for additional rate taxpayers). "Dividend allowance of 2.000 (unchanged from 2020/21) ** These rates apply in England, Wales and Northem Ireland only. Scottish IT rates: 12,097=19%,2,09812,726=20%,12,72731,092=21%, 31,093150,000=41%, over 150,000=46% Income tax reliefs and incentives: annual limits Approved mileage rates Excess payments over these rates are taxable. Shortfalls can be claimed as tax relief by the employee. If the employee carries another employee in their own car or van on a business journey, and additional tax-free payment of 5p per mile applies. Car and fuel benefits in kind (Round reported CO2g/km down to find the correct percentage) Company car benefit charge (registered before 6 April 2020 - NEDC - non-hybrid): Company car benefit charge (registered after 6 April 2020 - WLTP - non-hybrid): Company car benefit charge (hybrid cars with CO2250K 925K=5% (above this normal rates apply). Annual Tax on Enveloped Dwellings Uver I ou, unu 1. 4% supplement on additional dwelling purchased over 40,000. LBTT relief for 1st time purchasers up to 175,000. Non-residential property (on or after 25 Jan 19) Welsh Land Transaction Tax 1. 4% supplement on additional dwelling ( 3% before 22 December 20) ** LBTT relief for 1st time purchasers up to 175,000. Effective 27 July 20 to 30 June 21 reduced rates apply for purchases up to 250K=0%, (above rates apply thereafter) Insurance Premium Tax: Standard Higher Ra vehicles) Air Passenger Duty: HMRC interest rates (These rates change occasionally - see the HMRC website for details) Duty rates Duty Typical Item On 6 April 2021, Harry Johnson, aged 38, started employment with, Queens words Ltd as a proof-reader. On the 11 January 2022, Harry also entered into a partnership with his friend Debra. Together they set up a local office of proofreading and preparing accounts for 30th April. Partnership a) The partnership tax adjusted trading profit for the four-month period ended 30 April 2022 was 29,600. This figure is before deduction for any capital allowances. b) The only capital items owned by the partnership are: - A reception desk and bookshelves units costing 725 in total, purchased on 29 November 2021. - A petrol motor car that cost 12,000 on 1 February 2022 (with CO2 emission rate of 105g/km). The car is used by Debra who estimates 20% of his mileage is for private journeys. c) The partners have agreed to pay Debra in lieu of salary and to share any remaining profits 40% to Harry and 60% to Debra. Employment at Queens Words Ltd d) During the tax year 2021/2022 Harry earned a gross annual salary of 31,850 working for Queens Words Ltd Harry paid 6,110 income tax and 4,197 national insurance contributions Pay as You Earn. e)Throughout the tax year 2021/22 Queens Words Ltd provided Harry with non-jobrelated living accommodation. The company purchased the property in 2017 for 199,500 and when Harry moved in on the 6 April 2021 it was valued at 256,000. The annual value of the property is 6,100 and the company furnished the property during March 2021 at a cost of 7,600. f) Harry was provided with unrestricted use of a mobile phone. The phone contract cost Queens Words Ltd 38 a month. Property Income g) Harry owns a freehold house which he lets out to tenants furnished. The property was let throughout the tax year at a monthly rent of 725. h) During the tax year Harry paid council tax of 1,320 in respect of the property. Harry also spends 560 on replacing a damaged sofa and 1,250 to install a new dishwasher in a previously empty space in the house's kitchen. Investment Income i) During the tax year Harry received 580 interest on his Building Society savings account and 500 interest on his Individual Savings Account. j) Harry owns shares in a family company and received a dividend of 6,500 on 25 April 2021. Value added tax (VAT) k) The partnership voluntarily registered for VAT on 1 January 2022 and immediately began using the flat rate scheme to calculate the amount of VAT payable. The relevant flat rate scheme percentage for the partnership's trade is 12%. I) The partnership paid 145 VAT on the furniture purchased on 29 November 2021 and 2,400 on the car bought in February 2022 (see note b above) m) For the quarter ended 31 March 2022 the partnership had standard rate sales of 59,700, with all sales made to the general public. For the same period standard rated expenses amounted to 27,300. (both figures are stated inclusive of VAT) Disposal Information n) On 13 May 2021 Harry sold, for 60,000 all the shares he held in an unlisted trading company (for which he never worked). Harry acquired the shares from his father in May 2018 for 7,500 when the market value was 40,000 at which time both Harry and his father agreed to a gift relief election. Harry's father paid 1,000 for the shares in 1991. o) On 26 November 2021 Harry sold a painting for 18.300 proceeds, before auctioneer's commission of 5%. She purchased the painting on 16 May 2013 for 5,200. B3-Explain, with supporting calculations, whether or not it was beneficial for the partnership to have used the VAT flat rate schemes for the quarter ended 31 March 2022: (20\%) TABLE OF 2021/22 TAX RATES AND ALLOWANCES The current rates and allowances for income tax, corporation tax, capital gains tax, inheritance tax and other taxes are set out below. Income tax rates 0% rate on savings only available up to 5,000 of savings income if non-savings income does not exceed this sum. In addition, a 1,000 personal savings allowance is available to basic rate taxpayers ( 500 for higher rate and nil for additional rate taxpayers). "Dividend allowance of 2.000 (unchanged from 2020/21) ** These rates apply in England, Wales and Northem Ireland only. Scottish IT rates: 12,097=19%,2,09812,726=20%,12,72731,092=21%, 31,093150,000=41%, over 150,000=46% Income tax reliefs and incentives: annual limits Approved mileage rates Excess payments over these rates are taxable. Shortfalls can be claimed as tax relief by the employee. If the employee carries another employee in their own car or van on a business journey, and additional tax-free payment of 5p per mile applies. Car and fuel benefits in kind (Round reported CO2g/km down to find the correct percentage) Company car benefit charge (registered before 6 April 2020 - NEDC - non-hybrid): Company car benefit charge (registered after 6 April 2020 - WLTP - non-hybrid): Company car benefit charge (hybrid cars with CO2250K 925K=5% (above this normal rates apply). Annual Tax on Enveloped Dwellings Uver I ou, unu 1. 4% supplement on additional dwelling purchased over 40,000. LBTT relief for 1st time purchasers up to 175,000. Non-residential property (on or after 25 Jan 19) Welsh Land Transaction Tax 1. 4% supplement on additional dwelling ( 3% before 22 December 20) ** LBTT relief for 1st time purchasers up to 175,000. Effective 27 July 20 to 30 June 21 reduced rates apply for purchases up to 250K=0%, (above rates apply thereafter) Insurance Premium Tax: Standard Higher Ra vehicles) Air Passenger Duty: HMRC interest rates (These rates change occasionally - see the HMRC website for details) Duty rates Duty Typical Item