Answered step by step

Verified Expert Solution

Question

1 Approved Answer

On Jan 1, 2016, PORE Inc. purchased 80% of the voting shares of SCORE Inc. for $900,000 cash, plus a commitment to pay an additional

On Jan 1, 2016, PORE Inc. purchased 80% of the voting shares of SCORE Inc. for $900,000 cash, plus a commitment to pay an additional $300,000 in three years if sales grow by more than 20% over the next three years. An independent business valuator stated that PORE Inc. could have paid an extra $100,000 at the date of acquisition instead of agreeing to a potential payment of $300,000 in three years.

On the date of acquisition, SCOREs Common Stock and Retained Earnings were valued at $200,000 and $600,000 respectively. PORE uses the cost method to account for its investment.

SCOREs fair values approximated its carrying values with the following exception:

The equipment had a fair value that was $ 100,000 higher than its carrying value, and was estimated to have a remaining useful life of 10 years from the date of acquisition with no salvage value.

SCOREs inventory had a fair value that was $2,000 more than book value. SCORE sold this inventory in 2016.

SCORE had an internally developed patent that had a fair value of $20,000 and can be used for four years. SCORE did not include the value of the patent on its financial records.

Both companies use straight line amortization exclusively for all assets and liabilities if applicable.

The effective tax rate for both companies is 40%.

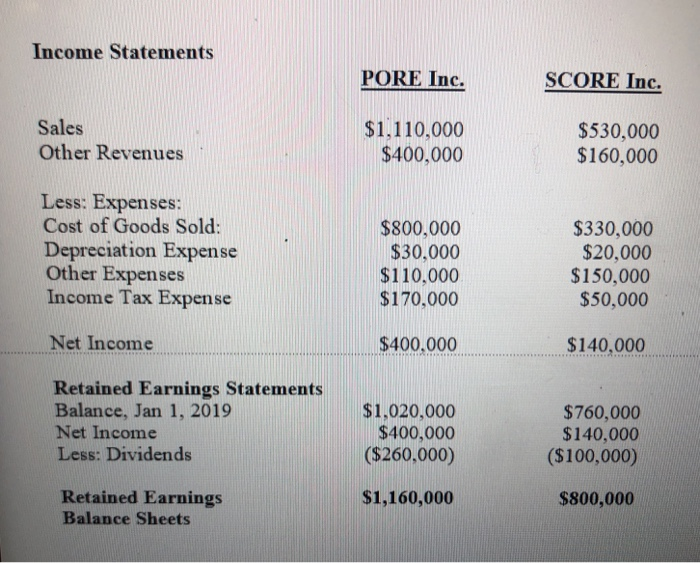

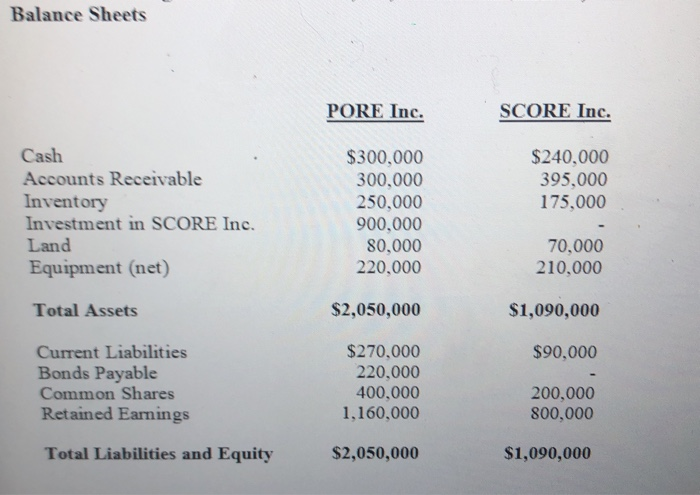

The Financial Statements of PORE & SCORE for the Year ended December 31, 2019 are shown below:

Other Information:

1. On Jan 2, 2016, SCORE purchased equipment for $70,000 and estimated its useful life would be 7 years with no salvage value. On Jan 1, 2019, SCORE sold the equipment to PORE for $80,000. Both companies use straight line depreciation.

2. During 2018, PORE sold a parcel of land to SCORE for $95,000. PORE had purchased this land in 2016 for $80,000. Score still has the land and uses as a warehouse space.

3. During 2019, PORE charged SCORE $15,000 of management fees. SCORE paid $10,000 during the year and expects to pay the remaining $5,000 in 2020.

4. During December 2019, PORE sold inventory to SCORE for $80,000, the cost of the inventory to PORE was $60,000. 40% of these goods remained in SCOREs inventory at the end of 2019.

5. During December 2018, SCORE sold inventory to PORE for $60,000, the cost of the inventory to SCORE was $30,000. 10% of these goods remained in POREs inventory at the end of 2018. PORE eventually sold the entire inventory to an outside customer in 2019.

6. A goodwill impairment test conducted during December of 2017 revealed a loss of $50,000 and Dec of 2019 another loss of 35,000.

REQUIRED:

a) Prepare a schedule showing the calculation of goodwill at the date of acquisition of SCORE under the fair value enterprise method, and an acquisition differential amortization schedule.

b) Prepare a schedule showing the inter-company realized and unrealized profits. Your schedule should include both pre-tax and after-tax amounts.

c) Prepare the consolidated financial statements under the fair value enterprise method: Income statement and Retained Earnings for the year ended December 31st, 2019, and Balance Sheet as at December 31st, 2019. Show all supporting calculations.

NOTE: In preparing Consolidated Statement of Retained Earnings you need to calculate the opening retained earnings. Dont forget to show all your calculations.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using Microcomputers In Managerial Accounting

Authors: George Hildebrand

1st Edition

0938188275, 978-0938188278