Answered step by step

Verified Expert Solution

Question

1 Approved Answer

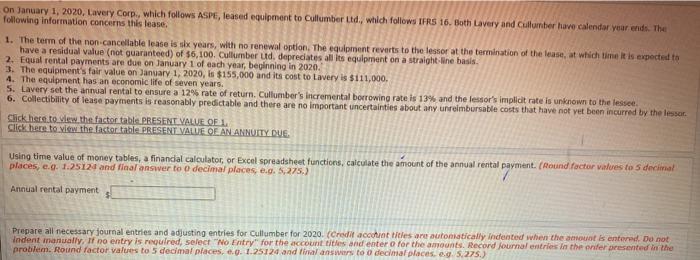

On January 1, 2020, Lavery Corp., which follows ASPE, leased equipment to Cullumber Ltd., which follows IFRS 16. Both Lavery and Culturber have calendar year

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Well Church Book A Practical Guide To Mission Audit

Authors: John Finney

1st Edition

0862015499, 978-0862015497