Answered step by step

Verified Expert Solution

Question

1 Approved Answer

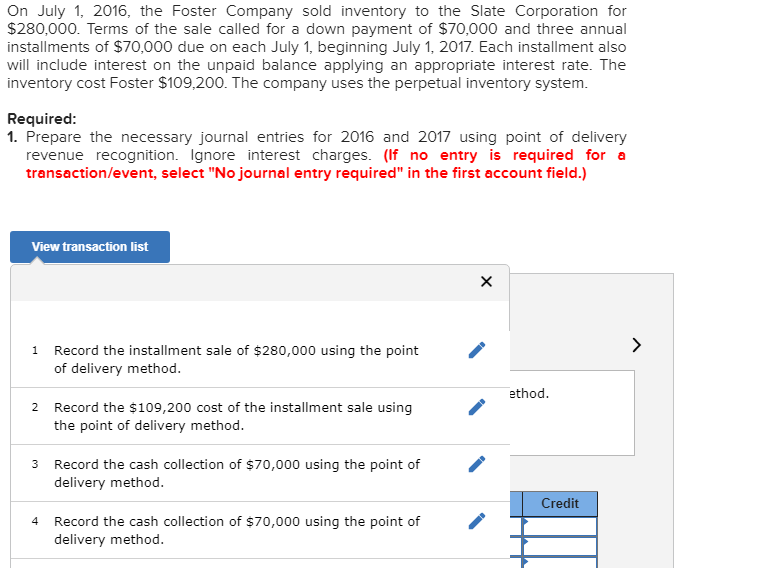

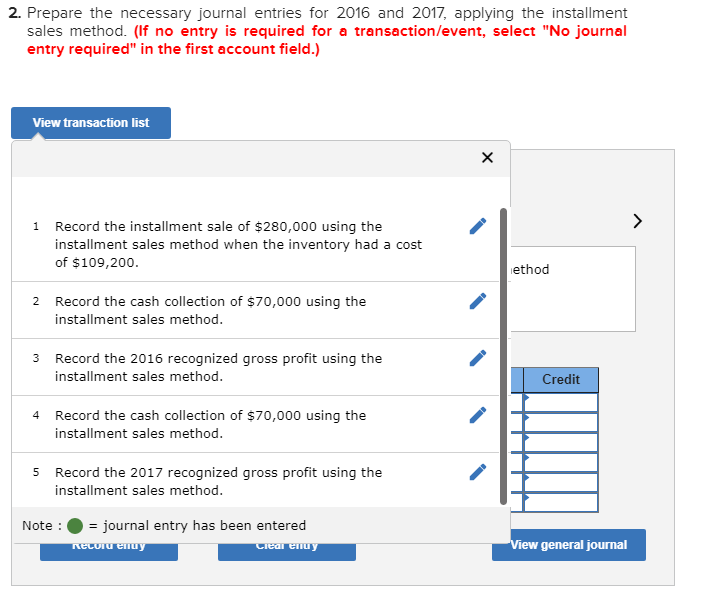

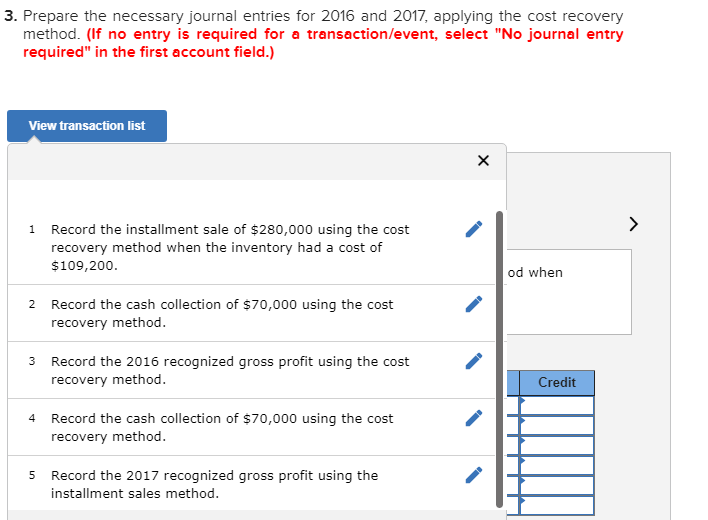

On July 1, 2016, the Foster Company sold inventory to the Slate Corporation for $280,000. Terms of the sale called for a down payment of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

High Performance Cloud Auditing And Applications

Authors: Keesook J. Han, Baek-Young Choi, Sejun Song

1st Edition

1493944355, 978-1493944354