Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Option Payoffs. Suppose that you wish to make a bet on Sofi Technologies (SOFI) as follows. You will (a) buy two calls on SOFI

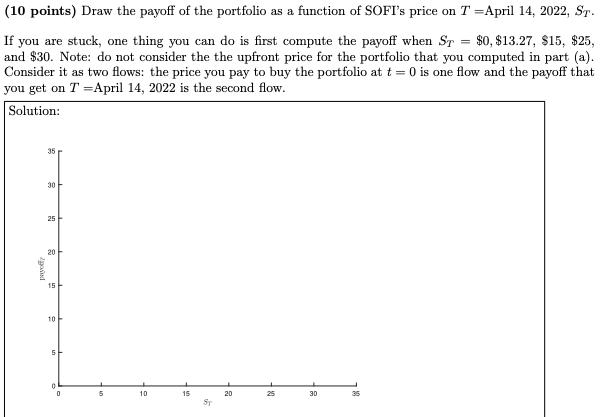

Option Payoffs. Suppose that you wish to make a bet on Sofi Technologies (SOFI) as follows. You will (a) buy two calls on SOFI struck at $15 expiring on April 14, 2022, (b) sell six calls on SOFI struck at $25 expiring on April 14, 2022, (c) buy four calls on SOFI struck at $30 expiring on April 14, 2022, SOFI is currently trading at $13.27. For the purpose of this problem, assume the calls are European (in fact, standard single name options are American) and assume you can buy a call on one share (in fact, call options contracts are options on 100 shares). Prices of the calls are given below: (10 points) Draw the payoff of the portfolio as a function of SOFI's price on T=April 14, 2022, ST. If you are stuck, one thing you can do is first compute the payoff when ST $0, $13.27, $15, $25, and $30. Note: do not consider the the upfront price for the portfolio that you computed in part (a). Consider it as two flows: the price you pay to buy the portfolio at t = 0 is one flow and the payoff that you get on T = April 14, 2022 is the second flow. Solution: payofy 35 30 25 20 15 10 5 0 0 5 10 15 ST 20 25 30 35 =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Here is the payoff diagram of the portfolio as a function of SOFIs stock price ST on Apr...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Derivatives And Risk Management

Authors: Don M. Chance, Robert Brooks

10th Edition

130510496X, 978-1305104969