Question

ORBITS In 1997, J. D. Orbits opened a cell phone accessory manufacturing plant named Orbits. Although the company began its operations at the local level

ORBITS

In 1997, J. D. Orbits opened a cell phone accessory manufacturing plant named Orbits. Although the company began its operations at the local level with only 40 employees, 3 vendors and 5 main customers, it experienced rapid success. By 2001, gross sales tripled, and the enterprise expanded its customer, vendor and employee base. It now serves all major cell phone manufacturers. Currently, Orbits employs more than 120 individuals, including executives, directors, sales representatives, office personnel, and production workers. Customers: Orbits sells to the outlets stores of distributors such as Verizon, MCI, Cingular and AT&T cellular phone in the tri-state area.

Materials and Suppliers: Manufacturing hands-free cell phone devices requires several different materials, none of which is made in-house. Most parts are purchased from 25 vendors. The more complex components used in the manufacturing process are purchased through contracts with vendors. Raw materials are purchased from vendors according to price without a formal contract.

Accounting System

Orbits' s accounting system is comprised of manual procedures that are supported by stand- alone PCs (not networked) in several departments. Key elements of the sales order processing, purchasing, fixed assets, and payroll systems are described in the following paragraphs.

Purchases System

The process begins in the purchasing and inventory control department. Using the department PC, a clerk monitors the inventory levels in the digital inventory ledger. When the inventory on hand falls below the reorder point, the clerk prints two copies of a purchase requisition. The clerk sends one copy to the accounts payable department, where the account payable clerk files it in the account payable pending file. The clerk hands the second copy of the requisition to his co-worker (the purchasing clerk) in the department, who manually prepares a four-part purchase order. The purchasing clerk sends one copy of the purchase order to the account's

payables department (where it filed in the account payable pending file) and two copies to the vendor. The clerk sends the final purchase order copy, along with the original purchase requisition, to another co-worker in the department (the inventory control clerk) who, using the department PC, updates the inventory ledger to record the inventory increase. The inventory control clerk then files the requisition and purchase order in the department.

When the products arrive, the receiving department clerk inspects, counts and reconciles them to the packing slip. The clerk then prepares three copies of a receiving report, which contains quantities, prices, and freight charges transcribed from the packing slip. One copy of the receiving report is sent with then inventory to the storeroom. Another copy is sent to the accounts payable department, where it filed in the accounts payable pending file. The final copy is filed in the receiving department.

Once the accounts payable clerk receives the purchase requisition, purchase order, and receiving report, she accesses the department PC, records the liability in the purchases journal, and posts it to the supplier's account in the account payable subsidiary ledger. The clerk then transfers the hard-copy purchase requisition, purchase order, and receiving report to the open accounts payable file. The accounts payable clerk then prints a journal voucher from PC summarizing the transactions in the purchases journal for the period and sends it to general ledger department. The general ledger clerk receives the hard-copy journal voucher and the invoice from the vendor. The clerk then uses the department PC to post to the inventory and accounts payable control accounts.

Cash Disbursement Process

Periodically, the account payable clerk reviews the hard-copy documents in the open account payable file and identified items to be paid. The clerk accesses the departments PC, prints a hard-copy cash disbursement voucher, and send it to the cash disbursements department. The clerk then removes the liability from the digital accounts payable subsidiary ledger. Finally, the clerk files the hard-copy documents in the closed accounts payable file.

Upon receipt of the cash disbursement voucher, the cash disbursement clerk accesses the department PC, print a vendor check, and records the check in the in the digital check register. Next, the clerk sends the check to the vendor and sends the hard-copy cash disbursement voucher to the general ledger department. The general ledger clerk receives the cash disbursement voucher and posts to the general ledger cash and account payables accounts, using the department PC. Finally, the general ledger clerk files the voucher in the department.

Payroll System

Production

Each week the production department supervisor submits employee timecards to the payroll department for processing. The supervisor also sends the job tickets to the cost accounting department, which uses them to allocate labour and manufacturing overheads costs to work-in- process account.

Payroll

The payroll department clerk receives the timecards and uses the department PC to update the employee payroll records. The clerk also prints the employee pay checks and a payroll register. A copy of the payroll register is sent to the account payables, and the pay checks are signed and sent to the supervisors for distribution to the employees. A copy of the payroll registers and timecards are filed in the department.

Accounts Payable

The accounts payable department uses the payroll register to manually prepare two copies of a cash disbursement voucher. One copy of the voucher and the payroll register are sent to the cash disbursement department. The second copy of the voucher is sent to the general ledger department.

Cash Disbursements

The cash disbursements department uses the payroll register and the cash disbursement voucher to manually prepared a check for a total payroll. The payroll check is signed and sent to the bank for deposit into the payroll imprest account. The voucher, the payroll check copy, and the payroll register are filed in the department.

General Ledger

The general ledger uses the cash disbursement voucher to update the digital general ledger payroll account from the department PC. The voucher is then filed in the department.

Fixed Asset System

Purchasing

At Orbits, the purchasing department is responsible for ordering fixed assets for user departments based on a user-generated purchase requisition. When the purchasing department clerk receives the purchase requisition from the user department, she creates a purchase order and send it to the vendor. The purchase requisition is filed in the purchasing department.

When the asset is shipped, the vendor sends the invoice to the accounts payable department and delivers the assets directly to the user department, where it is reconciled to the packing slip and placed into service. The user then sends the packing slip to the fixed asset department.

Accounts Payable

Upon receipt of the invoice from the vendor, the accounts payable clerk assesses the department PC, determines a due date for payment, records the liability in the accounts payable subsidiary ledger, and files the invoice in the open accounts payable file. Periodically, the clerk reviews the open accounts payable file for items to be paid. When an account payable is due, the clerk assesses the department PC, prints a hard-copy cash disbursement voucher, and sends it to the cash disbursement department. The clerk then removes the liability from the digital account payable subsidiary ledger. Finally, the clerk files the hard-copy invoice in the closed accounts payable file.

Cash Disbursements

Upon receipt of the cash disbursement voucher, the cash disbursements clerk accesses the department PC, prints a vendor check, and records the check in the digital check register. Next, the clerk sends the check to the vendor and sends the hard-copy cash disbursement voucher to the general ledger department.

Fixed Asset Department

When the fixed asset department clerk receives the packing slip from the user department, he accesses the department computer and records the asset in the fixed asset subsidiary ledger. Periodically, the clerk prepares an account summary that he sends to the general ledger. Note: The fixed asset department has additional procedures to manage the maintenance and disposal of fixed assets. These procedures are not part of this assignment.

General Ledger Department

The general ledger receives the cash disbursement voucher from the cash disbursement and the account summary from the fixed asset department. The general ledger then accesses the department PC and posts to the cash, accounts payable control, and fixed asset control accounts. Finally, the general ledger clerk files the voucher and account summary in the department.

Sales Order System

The sales department receives customer orders via fax, mail and e-mail. A sales clerk using the sales department PC records the orders in the sales order file and prints a stock release, invoice, ledger copy, and packing slip. The documents are distributed as follows:

The invoice and ledger copy are sent to billing, where the clerk records the sales record the sale in the digital sales journal form the department computer. The clerk then sends the invoice to the customer and the ledger copy to the account receivable department.

The stock release is sent to the warehouse, where the goods are picked and the warehouse clerk updates the stock records from the department PC. The clerk then sends the stock release and the goods to the shipping department.

The packing slip is sent to the shipping department, where it is reconciled to the stock release. The shipping clerk then manually prepares a bill of lading, the product, and packing slip to the carrier. The stock release is sent to the purchasing department and inventory control department, where it is used to update the inventory subsidiary ledger. The inventory control clerk then files the stock release and prepares an account summary, which is sent to the general ledger department.

The account receivable clerk receives a ledger copy document. The clerk then accesses the department PC to update the accounts receivable subsidiary ledger. The clerk then files the ledger copy and prepares an account summary, which sends to the general ledger department.

Cash Receipts System

The mail room receives envelopes containing customer checks and remittance advices. The checks are sent to the cash receipts department, and the remittance advices are sent to the account receivable department. The cash receipts department records the cash receipts in the cash receipts journal. The clerk then prepares a bank deposit slip and sends the checks and two copies of the deposit slip to the bank. Periodically, the bank returns a deposit slip to the cash receipts department, where it is reconciled with the cash account. The accounts receivable department reviews the remittance advices and updates the account receivable subsidiary ledger. The clerk files the remittance advice and prepares an account summary, which sends to the general ledger.

General Ledger Department

The general ledger clerk receives account summarizes from the account receivable and the purchasing and inventory control departments. The general ledger clerk accesses the department PC and posts to the inventory control, AR control, and cash accounts. Finally, the general ledger clerk files the account summaries in the department.

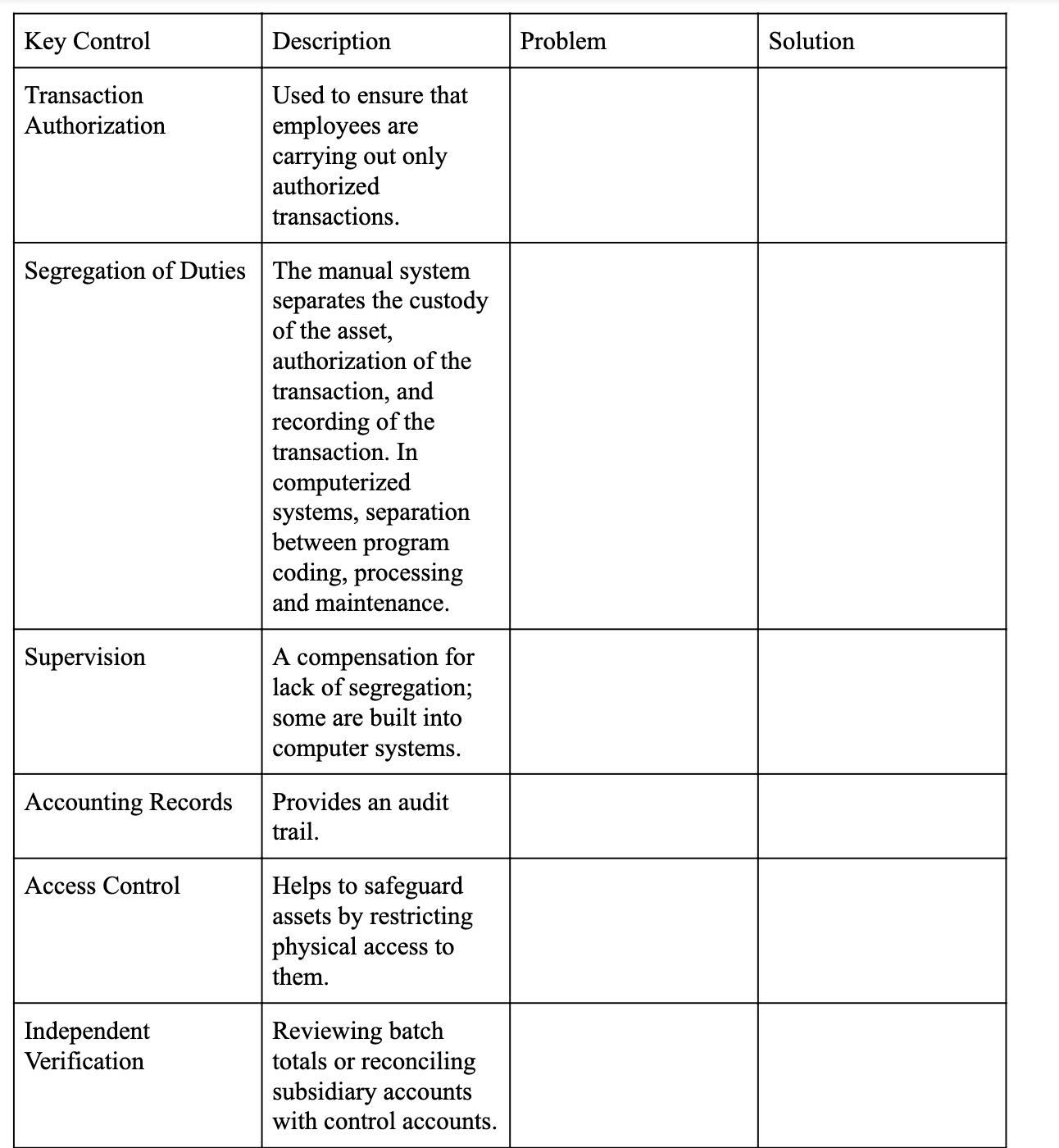

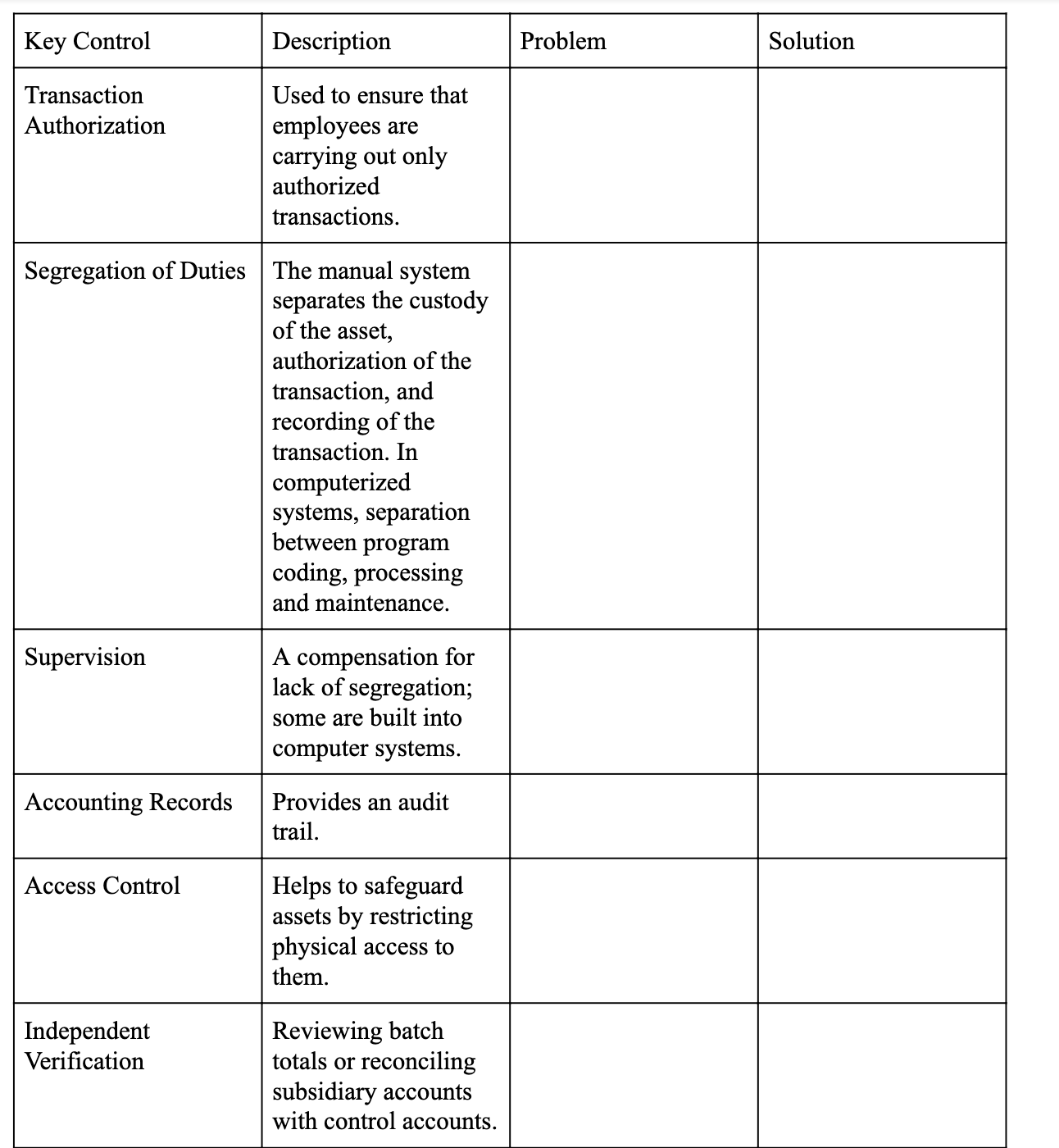

a) Analyse the physical internal control weaknesses in the system. Model your response according to the six categories of physical control activities.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Information System

Authors: James A. Hall

7th Edition

978-1439078570, 1439078572