Answered step by step

Verified Expert Solution

Question

1 Approved Answer

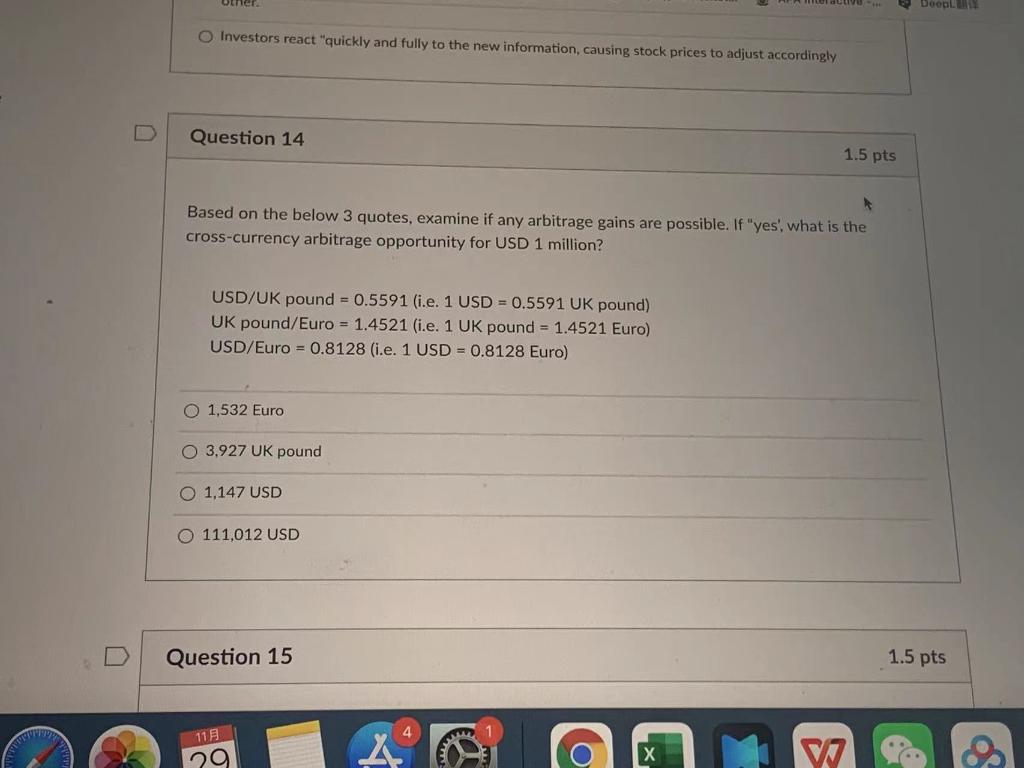

otnet Doop Investors react quickly and fully to the new information, causing stock prices to adjust accordingly Question 14 1.5 pts Based on the below

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Security Global Vulnerabilities Threats And Responses

Authors: Martin S. Navias

1st Edition

1787381366, 978-1787381360