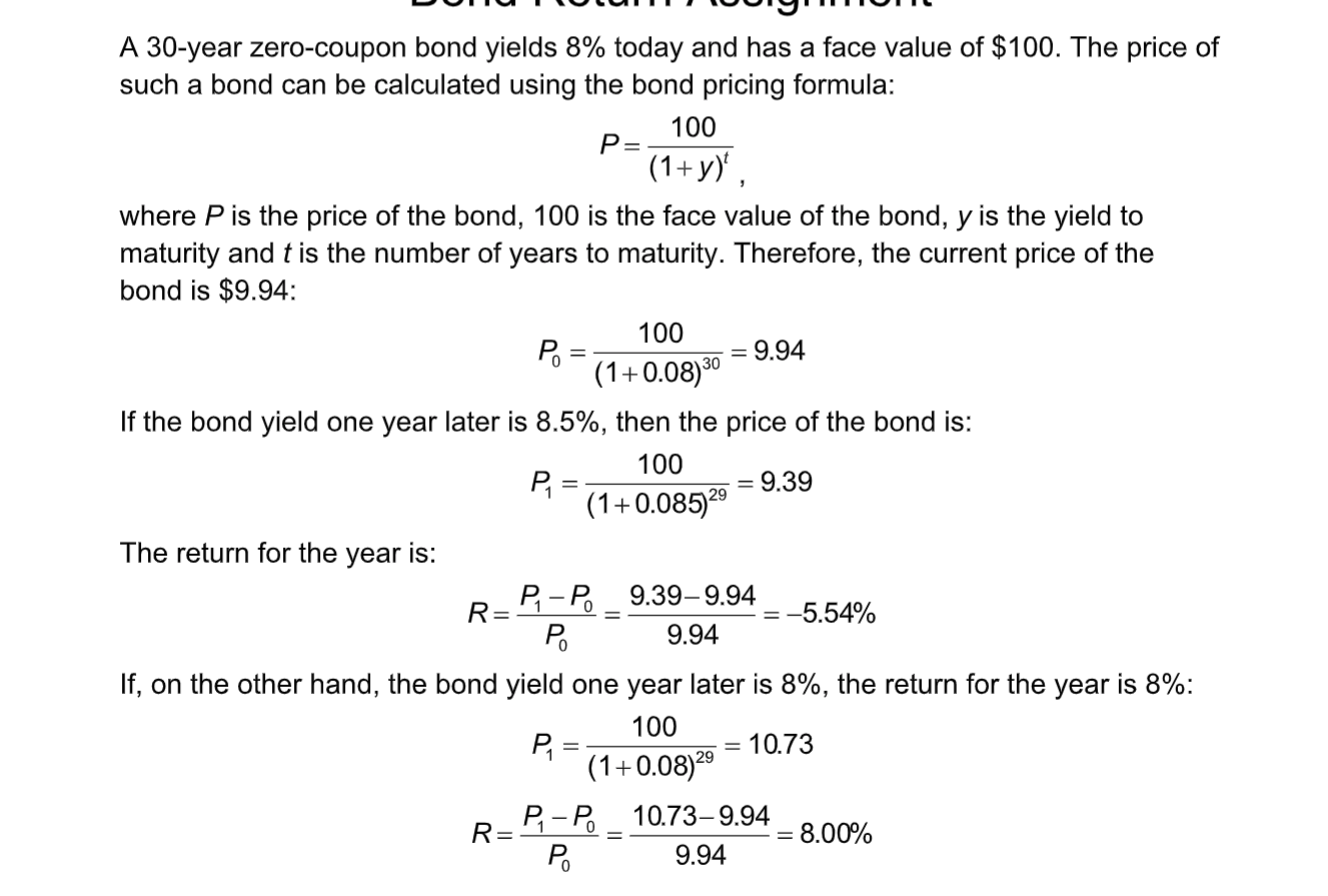

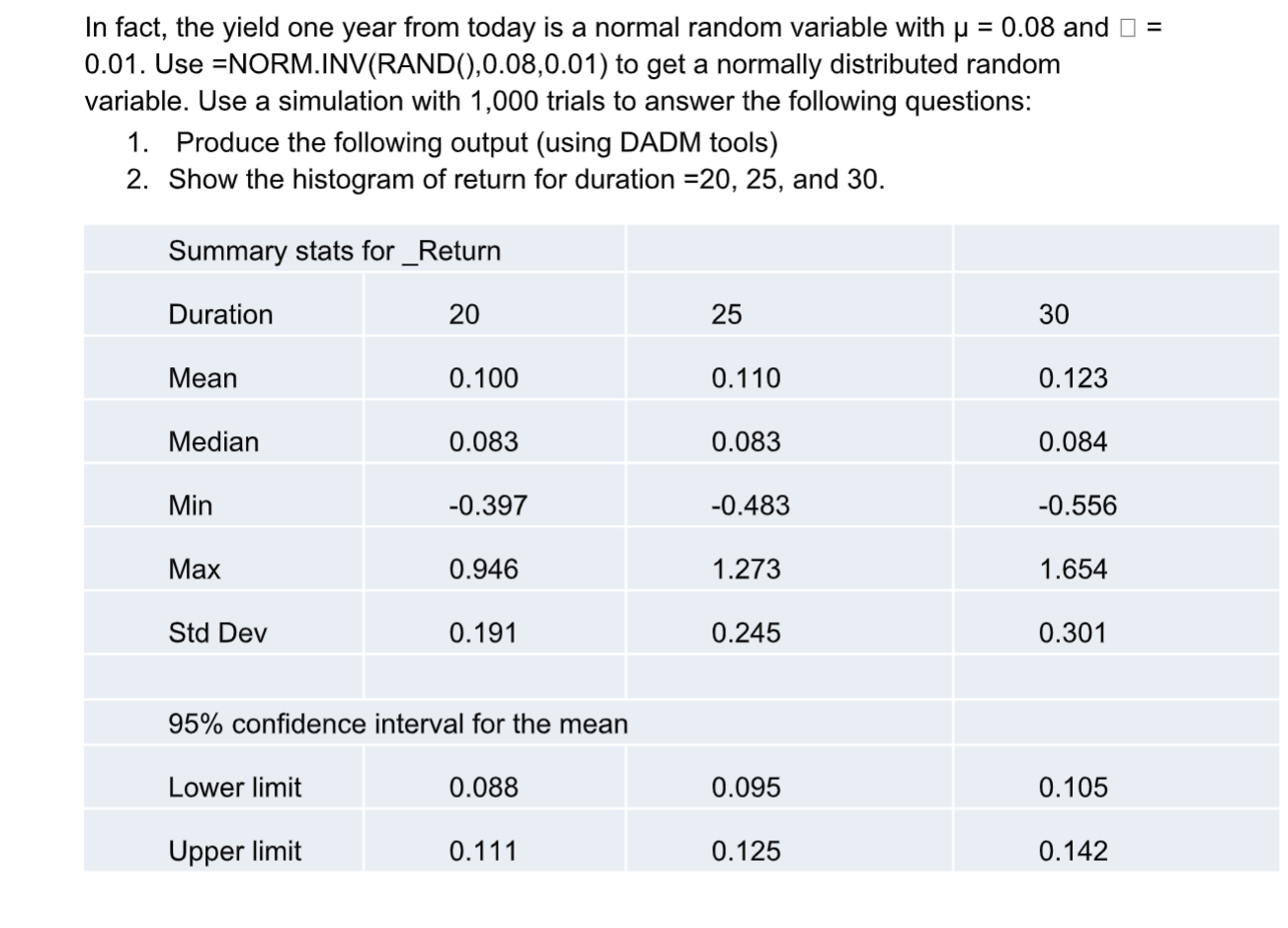

P= A 30-year zero-coupon bond yields 8% today and has a face value of $100. The price of such a bond can be calculated using the bond pricing formula: 100 (1+y) where P is the price of the bond, 100 is the face value of the bond, y is the yield to maturity and t is the number of years to maturity. Therefore, the current price of the bond is $9.94: 100 Po 9.94 (1+0.08) 30 If the bond yield one year later is 8.5%, then the price of the bond is: 100 9.39 (1+0.085)29 The return for the year is: R= P.-P. _9.399.94 -5.54% Po 9.94 If, on the other hand, the bond yield one year later is 8%, the return for the year is 8%: 100 10.73 (1+0.08)29 10.73-9.94 R = 8.00% 9.94 = P.-Po = In fact, the yield one year from today is a normal random variable with u = 0.08 and I = 0.01. Use =NORM.INV(RAND(),0.08,0.01) to get a normally distributed random variable. Use a simulation with 1,000 trials to answer the following questions: 1. Produce the following output (using DADM tools) 2. Show the histogram of return for duration=20, 25, and 30. Summary stats for _Return Duration 20 25 30 Mean 0.100 0.110 0.123 Median 0.083 0.083 0.084 Min -0.397 -0.483 -0.556 Max 0.946 1.273 1.654 Std Dev 0.191 0.245 0.301 95% confidence interval for the mean Lower limit 0.088 0.095 0.105 Upper limit 0.111 0.125 0.142 P= A 30-year zero-coupon bond yields 8% today and has a face value of $100. The price of such a bond can be calculated using the bond pricing formula: 100 (1+y) where P is the price of the bond, 100 is the face value of the bond, y is the yield to maturity and t is the number of years to maturity. Therefore, the current price of the bond is $9.94: 100 Po 9.94 (1+0.08) 30 If the bond yield one year later is 8.5%, then the price of the bond is: 100 9.39 (1+0.085)29 The return for the year is: R= P.-P. _9.399.94 -5.54% Po 9.94 If, on the other hand, the bond yield one year later is 8%, the return for the year is 8%: 100 10.73 (1+0.08)29 10.73-9.94 R = 8.00% 9.94 = P.-Po = In fact, the yield one year from today is a normal random variable with u = 0.08 and I = 0.01. Use =NORM.INV(RAND(),0.08,0.01) to get a normally distributed random variable. Use a simulation with 1,000 trials to answer the following questions: 1. Produce the following output (using DADM tools) 2. Show the histogram of return for duration=20, 25, and 30. Summary stats for _Return Duration 20 25 30 Mean 0.100 0.110 0.123 Median 0.083 0.083 0.084 Min -0.397 -0.483 -0.556 Max 0.946 1.273 1.654 Std Dev 0.191 0.245 0.301 95% confidence interval for the mean Lower limit 0.088 0.095 0.105 Upper limit 0.111 0.125 0.142