Answered step by step

Verified Expert Solution

Question

1 Approved Answer

page number on bottom of page 2. On Page 36, under the section Break-Even Analysis, please calculate the breakeven point if the sales price increase

page number on bottom of page

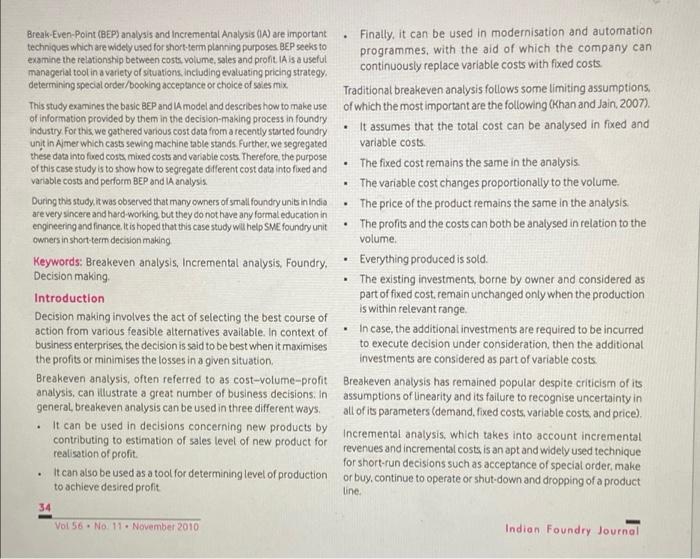

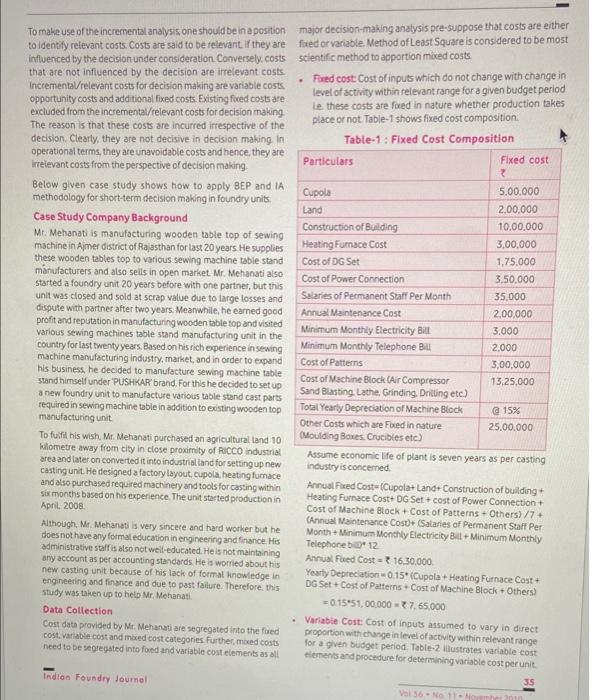

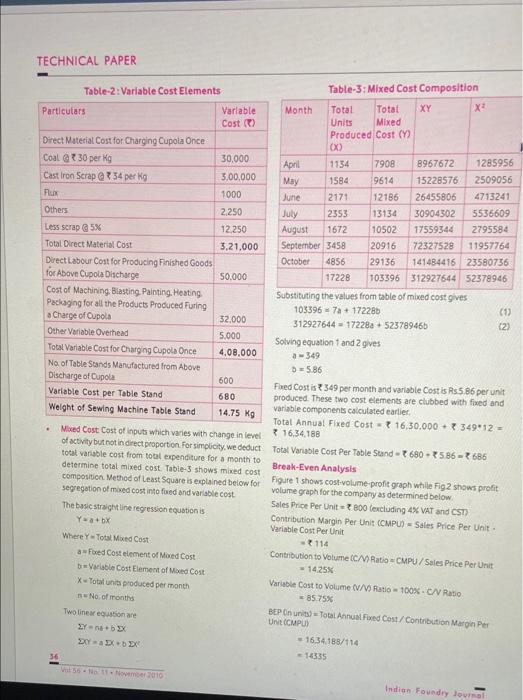

2. On Page 36, under the section Break-Even Analysis", please calculate the breakeven point if the sales price increase by 50. Did the breakeven point increase or decrease? . . Breake-Even-Point (BEP) analysis and Incremental Analysis (IA) are important Finally, it can be used in modernisation and automation techniques which are widely used for short-term planning purposes BEP seeks to programmes, with the aid of which the company can examine the relationship between costs. volume, sales and profit IA is a useful managerial tool in a variety of situations, including evaluating pricing strategy continuously replace variable costs with fixed costs. determining special order/booking acceptance or choice of sales mix, Traditional breakeven analysis follows some limiting assumptions, This study examines the basic BEP and IA model and describes how to make use of which the most important are the following (Khan and Jain 2007). of information provided by them in the decision-making process in foundry Industry For this we gathered various cost data from a recently started foundry It assumes that the total cost can be analysed in fixed and unt in Almer which casts sewing machine table stands Further, we segregated variable costs these data into foed costs mixed costs and variable costs. Therefore the purpose of this case study is to show how to segregate different cost data into fixed and The fixed cost remains the same in the analysis variable costs and perform BEP and IA analysis The variable cost changes proportionally to the volume. During this study, it was observed that many owners of small foundry units in India The price of the product remains the same in the analysis are very sincere and hard working, but they do not have any formal education in engineering and finance. It is hoped that this case study wit help SME foundry unit The profits and the costs can both be analysed in relation to the owners in short-term decision making volume. Keywords: Breakeven analysis, Incremental analysis, Foundry, Everything produced is sold Decision making The existing investments, borne by owner and considered as Introduction part of fixed cost. remain unchanged only when the production Decision making involves the act of selecting the best course of is within relevant range action from various feasible alternatives available. In context of In case, the additional investments are required to be incurred business enterprises, the decision is said to be best when it maximises to execute decision under consideration, then the additional the profits or minimises the losses in a given situation, investments are considered as part of variable costs Breakeven analysis often referred to as cost-volume-profit Breakeven analysis has remained popular despite criticism of its analysis, can illustrate a great number of business decisions, in assumptions of linearity and its failure to recognise uncertainty in general, breakeven analysis can be used in three different ways all of its parameters (demand fixed costs variable costs and price) it can be used in decisions concerning new products by incremental analysis, which takes into account incremental contributing to estimation of sales level of new product for revenues and incremental costs is an apt and widely used technique realisation of profit for short-run decisions such as acceptance of special order, make It can also be used as a tool for determining level of production or buy, continue to operate or shut-down and dropping of a product to achieve desired profit line 34 Vol 56. No 11. November 2010 Indian Foundry Journal . To make use of the incremental analysis one should be in a position major decision-making analysis pre-suppose that costs are either to identify relevant costs. Costs are said to be relevant. If they are faed or variable. Method of Least Square is considered to be most influenced by the decision under consideration Conversely, costs scientific method to apportion mixed costs. that are not influenced by the decision are irrelevant costs Pored cost Cost of inputs which do not change with change in Incremental/relevant costs for decision making are variable costs level of activity within relevant range for a given budget period opportunity costs and additional fixed costs. Existing fuced costs are Le these costs are fixed in nature whether production takes excluded from the incremental/relevant costs for decision making place or not. Table-1 shows fixed cost composition The reason is that these costs are incurred irrespective of the decision, Clearly, they are not decisive in decision making in Table-1: Fixed Cost Composition operational terms, they are unavoidable costs and hence, they are Particulars Fixed cost irrelevant costs from the perspective of decision making Below given case study shows how to apply BEP and IA Cupola 5.00.000 methodology for short-term decision making in foundry units. Land 2,00.000 Case Study Company Background Construction of Building 10.00.000 Mt. Mehanati is manufacturing wooden table top of sewing machine in Ajmer district of Rajasthan for last 20 years. He supplies Heating Furnace Cost 3.00.000 these wooden tables top to various sewing machine table stand Cost of DG Set 1.75.000 manufacturers and also sells in open market Mr. Mehanati also Cost of Power Connection 3.50.000 started a foundry unit 20 years before with one partner, but this unit was closed and sold at scrap value due to large losses and Salaries of Permanent Staff Per Month 35,000 dispute with partner after two years. Meanwhile, he earned good Annual Maintenance Cost 2,00,000 profit and reputation in manufacturing wooden table top and visited various sewing machines table stand manufacturing unit in the Minimum Monthly Electricity Bill 3.000 country for last twenty years. Based on his rich aperience in sewing Minimum Monthly Telephone Bill 2,000 machine manufacturing Industry, market, and in order to expand Cost of Patterns 3,00,000 his business, he decided to manufacture sewing machine table stand himself under 'PUSHKAR brand. For this he decided to set up Cost of Machine Block (Air Compressor 13.25,000 a new foundry unit to manufacture various table stand cast parts Sand Blasting. Lathe Grinding. Drilling etc.) required in sewing machine table in addition to existing wooden top Total Yearty Depreciation of Machine Block @ 15% manufacturing unit Other Costs which are Foxed in nature 25,00.000 To fulfil his wish Mr. Mehanati purchased an agricultural land 10 Moulding Boxes Crucibles etc.) kilometre away from city in close proximity of RICCO industrial Assume economic life of plant is seven years as per casting area and later on converted it into industrial land for setting up new industry is concerned casting unit He designed a factory layout, cupola heating fumace and also purchased required machinery and tools for casting within Annual Pared Cost(Cupola+Land Construction of building six months based on his experience. The unit started production in Heating Furnace Cost+DG Set + cost of Power Connection+ April 2008 Cost of Machine Block + Cost of Patterns + Others)/7+ Although. Mr. Mehanati is very sincere and hard worker but he Annual Maintenance Cost+ (Salaries of Permanent Staff Per does not have any formal education in engineering and finance. His Month Minimum Monthly Electricity Bill + Minimum Monthly administrative staff is also not well educated. He is not maintaining Telephone 12 any account as per accounting standards He is worried about his Annual Fed Cost 16.30,000 new casting unit because of his lack of formal knowledge in Yearty Depreciation 0.15" (Cupola + Heating Furnace Cost engineering and finance and due to past failure. Therefore, this DG Set+Cost of Patterns Cost of Machine Block +Others) study was taken up to helo Mr. Mehanati. = 0.1551,00.000 = 7.65.000 Data Collection Variable Cost Cost of inputs assumed to vary in direct Cost data provided by Mt. Mehanati are segregated into the foed cost variable cost and mixed cost categories. Furthermored costs proportion with change in level of activity within relevant range need to be segregated into ford and variable cost elements as all for a given budget period. Table-2 astrates variable cost elements and procedure for determining variable cost per unit Indian Foundry Journal 35 Volso. No TECHNICAL PAPER Table-2: Variable Cost Elements Particulars Variable Cost 30,000 3,00,000 1000 2.250 12.250 3,21,000 Direct Material Cost for Charging Cupola Once Coal 30 per kg Cast Iron Scrap @ 34 per kg Flu Others Less scrap 5X Total Direct Material Cost Direct Labour Cost for Producing Finished Goods for Above Cupola Discharge Cost of Machining Blasting Painting. Heating Packaging for all the Products Produced Furing Charge of Cupola Other Variable Overhead Total Variable Cost for Charging Cupola Once No. of Table Stands Manufactured from Above Discharge of Cupola Variable Cost per Table Stand Weight of Sewing Machine Table Stand Table-3: Mixed Cost Composition Month Total Total XY X Units Mixed Produced Cost (9) cx) April 1134 7908 8967672 1285956 May 1584 9614 15228576 2509056 June 2171 12186 26455806 4713241 July 2353 13134 30904302 5536609 August 1672 10502 17559344 2795584 September 3458 20916 72327528 11957764 October 4856 29136 141484416 23580736 17228 103596 312927644 52378946 50.000 Substituting the values from table of mixed cost gives 103396 7+ 172286 312927644-172288 +52378946b (2) 52,000 5.000 4.08.000 600 680 14.75 kg Mixed Cost Cost of inputs which varies with change in level of activity but not in direct proportion for simplicity.we deduct total variable cost from total expenditure for a month to determine total mixed cost. Table-3 shows med cost composition Method of Least Square is explained below for segregation of mixed cost into feed and variable cost The basic straight line regression equation is Ya+bX Where Total Med Cost Fored Cost element of Med Cost Variable Cost Element of Med Cost X-Total units produced per month No of months Two linearen Ya+b3X Solving equation 1 and 2 gives a 349 D=5.86 Fored Costis? 349 per month and variable Cost is Rs5 86 per unit produced. These two cost elements are clubbed with fived and variable components calculated earlier. Total Annual Fixed Cost - 16,30,000+ 34912 = * 16.34.188 Total Variable Cost Per Table Sund - 680-586-7686 Break-Even Analysis Figure 1 shows cost-volume-profit graph while Fig2 shows profit volume graph for the company as determined below Sales Price Per Unit = 800 (excluding 4% VAT and CST Contribution Margin PerUnit (CMPUS Ssies Price Per Unit Variable Cost Per Unit - 114 Contribution to Volume C/ Ratio - CMPU / Sales Price Per Unit 14.25% Variable Cost to Volume (V/)Ratio - 100%-CN Ratio 8575% BEP Ons Total Annual Ford Cost/Contribution Margin Per UN CMPUS - 1634.188/114 -14335 55.2016 Indian Foundry lonel Break Even Sales Revenue (BESR) - Total Annual Fixed Cost/CN in near future Old companies can estimate sales volume by using Ratio appropriate forecasting method. = 16,34.188/0.1425 Projected EBT or Margin of Safety (in) = 156650114 = 114, 67.986 17,85,810 Cash Break Even Point in units) - (Total Annual Fixed Cost - Margin of Safety Ratio - Margin of Safety / Actual Sales: icm Depreciation)/CMPU = (16,34,188-7,65,000/114 - 59.53% = 7625 Desired Sales Volume in units) to earn EBT of Rs.10,00.000 Cash Break-Even Sales Revenue (CBESR) =(Total Annual Fored Cost + Desired EBD/CMPU = Total Annual Fored Cost - Depreciation)/C/V Ratio - (16,34,188 + 10,00.000) / 114 = 60.99,565 - 23107 Margin of Safety on units) - Actual Estimated Sales - BEP Gn Units) Desired Sales Volume in units) to earn EBT of 20,00,000 = 50000 - 14355 = 15665 = (Total Annual Fored Cost + Desired EBT/CMPU Sales data are estimated based on past six months sales volume = (16,34,188 + 20,00,000) / 114 and firm orders which company have received from its customers = 31879 2 49000000 1000000 X Direct material cost - Direct labour cost A Variale overheads To il cost line Toal sales revenue line Totalfixed cost line X * X . 20 Costs & Profis X . 20000 150000 X . . 1 . . Sales Figure-1: Cost Volume Profit Graph. Indian Foundry Journal DI Vol 56 No 11. Nov 2010 5000000 4000000 3000000 2000000 Profit 1000000 0 5000 - 1000000 10000 15000 20000 25000 30000 35000 40000 45000 50000 -2000000 Sales volume in units Figure-2 : Profit Volume Graph. Confirmation Revised BEP in units) - Total annual foxed cost / revised CMPU Total Sales Revenue (31879*800) 255.03.200 = 16.34.188 / 79.70 = 20504 Less Variable Cost 31879'686) 218,68,994 Incremental Analysis Total Contribution 36.34,206 Mr. Mehanati's foundry unit has capacity to produce 5000 units Less Total Fixed Cost 16.34,188 per month current plan calls for a monthly production and sales of Earning Before Tax CEBT/Earning After Tax CEAT 20,00,018 only 2500 units so his facility is idle for half of the time. Meanwhile, Ajaymer Industries, maker of flour grinding machines asked *Small-scale industries are exempted from taxes Mr. Mehanati to produce 20000 floor grinding machine stands BEP in units) if variable cost increases by BSX due to inflation weighing 30 kg each at 45.50 per kg bargaining possible). Accepting this offer will cost further ? 50,000 to Mr. Mehanati for Revised Variable Cost = 686*1.085 745 pattern making Revised CMPU 800 - 745 = 55 Mr. Mehanati estimates that its variable cost will be ? 46.50 perag Revised BEP in units) = Total Annual Fored Cost/ Revised CMPU (variable cost of sewing machine stand divided by its weight le 14.75 kg). However, its foued costs, which have been averaging = 16,34.188/55 at 3.70 per kg (Total Annual Fored Cost Actual Estimated Sales of Sewing Machine stand" its weight) will now be spread over 29713 among 1042500 kg castings (30000 14.75+20000*30). As a BEP G units) if variable cost increases by 5% due to inflation result, the average fred cost will drop to 160 per kg (1634.189 Revised Variable Cost = 6869105-720.30 + 50.000//1042500). Mr. Mehanati concluded. "Sure there will be a loss of 1 per kg on variable costs 46.50 variable cost- Revised CMPU-800-720 30 = 79.70 45.50 selling price) but there will be a gain of 2.10 per kg of 38 Vol 56 No 11. November 2010 Indian Foundry Journal castings 3.70 per kg - 1.60 per kg) by spreading the fored competitive market in such a situation, Mr. Mehanati feels that he costs. Therefore, he accepts the offer as it represents an should earn at least 6,00,000 as profit by accepting Ajaymeru advantage of 1.10 per kg" Industries offer. Now, at what bid price he will be able to achieve this profit target considering 8.5% inflation in variable cost Do we agree with Mr. Mehanati? No, we do not agree with Mr. Mehanati's view as the acceptance of the order causes loss of Mr. Mehanati estimates that its new variable cost will be Rs.50.40T 6.50,000 20000 stand 30 kg? 1+ 50,000 of pattern per kg 46.50*1085) and fixed cost will drop to 1.60 per kg making). His contention is based on the illusion that spreading the after accepting the order. Further, each kg of casting should fetch floved cost causes savings. It is also shown below by the comparative profit of Re 1 in order to achieve target profit of 6,00.000 Income statement Therefore, he estimates bid price 53 per kg (50.40+160+1). Comparative Income Statement Again, IA plays an important role to decide the competitive price Alternatives for bidding as illustrated below. Particulars Status Quo Accept Order Anticipated Variable Cost per kg 350.40 (442500 kg (1042500 kg) Additional Fixed Cost per for Pattern Making Sales Revenue 240,00,000 513,00,000** (50,000/20000*30) 30.10 Less Variable Cost 205.76.250 484,76.250 Desired Profit per kg 1.00 Total Contribution 3423,750 28,23,750 Desired Bid Price per kg of Casting 51.50 Less Foxed Cost 16,34,188 16,84.188 Now, submission of higher bid price may lead to cancellation of Profit Before Taxes 17.89,562 11,39.562 Mr Mehanati's quotation by Ajaymeru Industries. Mr. Mehanati *130000 stand x 800). "*30000 stand XT 800 + 20000 flour included existing fixed cost 150 per kg for quoting bid price. A m/estand X 20 kg x 45.50) careful look at the cost items would enable that the existing fixed Above example clearly demonstrates that the existing food costs the share of existing fixed costs should not be charged to such a costs are to be incurred irrespective of the present decision Clearly. do not increase with an increase in the output Another notable new activity, its allocation causes distortion in submission of bid aspect related to fixed costs is that spreading of such costs to a price larger output base does not yield any decrease in total fixed costs either, in spite of the decrease in the average fxed cost per unit Conclusion However, we should not infer that fixed costs are always irrelevant with the help of this case study of foundry industry, we have tried costs. In case, the additional fored costs are required to be incurred to execute decision under consideration, then the additional fixed making say, segregation of costs determination of break-even point. to illustrate the importance of BEP and IA in short-term decision costs are as relevant as variable costs. For instance, 50,000 for making pattern in above example is foed in nature but is relevant level of production to achieve desired profit acceptance of the cost because it is an additional cost caused due to special order special order and determination of bid/tender price. It is hoped that this study will be very useful for owners of SME foundry In present scenario, inflation rate of 5-10% in variable cost is quite industries common in foundry industry. As we seeinflation rate of 85% at References anticipated demand of 50.000 sewing machine stand, leads to absence of profits in any year for Mr. Mehanati at present selling Khan M. Y. and Jan P.K. (2007). "Financial Management Test. Problems and price. Further, it is difficult to sell product at higher selling price in Cases S/ETCH Indian Foundry Journal Who 2010 2. On Page 36, under the section Break-Even Analysis", please calculate the breakeven point if the sales price increase by 50. Did the breakeven point increase or decrease? . . Breake-Even-Point (BEP) analysis and Incremental Analysis (IA) are important Finally, it can be used in modernisation and automation techniques which are widely used for short-term planning purposes BEP seeks to programmes, with the aid of which the company can examine the relationship between costs. volume, sales and profit IA is a useful managerial tool in a variety of situations, including evaluating pricing strategy continuously replace variable costs with fixed costs. determining special order/booking acceptance or choice of sales mix, Traditional breakeven analysis follows some limiting assumptions, This study examines the basic BEP and IA model and describes how to make use of which the most important are the following (Khan and Jain 2007). of information provided by them in the decision-making process in foundry Industry For this we gathered various cost data from a recently started foundry It assumes that the total cost can be analysed in fixed and unt in Almer which casts sewing machine table stands Further, we segregated variable costs these data into foed costs mixed costs and variable costs. Therefore the purpose of this case study is to show how to segregate different cost data into fixed and The fixed cost remains the same in the analysis variable costs and perform BEP and IA analysis The variable cost changes proportionally to the volume. During this study, it was observed that many owners of small foundry units in India The price of the product remains the same in the analysis are very sincere and hard working, but they do not have any formal education in engineering and finance. It is hoped that this case study wit help SME foundry unit The profits and the costs can both be analysed in relation to the owners in short-term decision making volume. Keywords: Breakeven analysis, Incremental analysis, Foundry, Everything produced is sold Decision making The existing investments, borne by owner and considered as Introduction part of fixed cost. remain unchanged only when the production Decision making involves the act of selecting the best course of is within relevant range action from various feasible alternatives available. In context of In case, the additional investments are required to be incurred business enterprises, the decision is said to be best when it maximises to execute decision under consideration, then the additional the profits or minimises the losses in a given situation, investments are considered as part of variable costs Breakeven analysis often referred to as cost-volume-profit Breakeven analysis has remained popular despite criticism of its analysis, can illustrate a great number of business decisions, in assumptions of linearity and its failure to recognise uncertainty in general, breakeven analysis can be used in three different ways all of its parameters (demand fixed costs variable costs and price) it can be used in decisions concerning new products by incremental analysis, which takes into account incremental contributing to estimation of sales level of new product for revenues and incremental costs is an apt and widely used technique realisation of profit for short-run decisions such as acceptance of special order, make It can also be used as a tool for determining level of production or buy, continue to operate or shut-down and dropping of a product to achieve desired profit line 34 Vol 56. No 11. November 2010 Indian Foundry Journal . To make use of the incremental analysis one should be in a position major decision-making analysis pre-suppose that costs are either to identify relevant costs. Costs are said to be relevant. If they are faed or variable. Method of Least Square is considered to be most influenced by the decision under consideration Conversely, costs scientific method to apportion mixed costs. that are not influenced by the decision are irrelevant costs Pored cost Cost of inputs which do not change with change in Incremental/relevant costs for decision making are variable costs level of activity within relevant range for a given budget period opportunity costs and additional fixed costs. Existing fuced costs are Le these costs are fixed in nature whether production takes excluded from the incremental/relevant costs for decision making place or not. Table-1 shows fixed cost composition The reason is that these costs are incurred irrespective of the decision, Clearly, they are not decisive in decision making in Table-1: Fixed Cost Composition operational terms, they are unavoidable costs and hence, they are Particulars Fixed cost irrelevant costs from the perspective of decision making Below given case study shows how to apply BEP and IA Cupola 5.00.000 methodology for short-term decision making in foundry units. Land 2,00.000 Case Study Company Background Construction of Building 10.00.000 Mt. Mehanati is manufacturing wooden table top of sewing machine in Ajmer district of Rajasthan for last 20 years. He supplies Heating Furnace Cost 3.00.000 these wooden tables top to various sewing machine table stand Cost of DG Set 1.75.000 manufacturers and also sells in open market Mr. Mehanati also Cost of Power Connection 3.50.000 started a foundry unit 20 years before with one partner, but this unit was closed and sold at scrap value due to large losses and Salaries of Permanent Staff Per Month 35,000 dispute with partner after two years. Meanwhile, he earned good Annual Maintenance Cost 2,00,000 profit and reputation in manufacturing wooden table top and visited various sewing machines table stand manufacturing unit in the Minimum Monthly Electricity Bill 3.000 country for last twenty years. Based on his rich aperience in sewing Minimum Monthly Telephone Bill 2,000 machine manufacturing Industry, market, and in order to expand Cost of Patterns 3,00,000 his business, he decided to manufacture sewing machine table stand himself under 'PUSHKAR brand. For this he decided to set up Cost of Machine Block (Air Compressor 13.25,000 a new foundry unit to manufacture various table stand cast parts Sand Blasting. Lathe Grinding. Drilling etc.) required in sewing machine table in addition to existing wooden top Total Yearty Depreciation of Machine Block @ 15% manufacturing unit Other Costs which are Foxed in nature 25,00.000 To fulfil his wish Mr. Mehanati purchased an agricultural land 10 Moulding Boxes Crucibles etc.) kilometre away from city in close proximity of RICCO industrial Assume economic life of plant is seven years as per casting area and later on converted it into industrial land for setting up new industry is concerned casting unit He designed a factory layout, cupola heating fumace and also purchased required machinery and tools for casting within Annual Pared Cost(Cupola+Land Construction of building six months based on his experience. The unit started production in Heating Furnace Cost+DG Set + cost of Power Connection+ April 2008 Cost of Machine Block + Cost of Patterns + Others)/7+ Although. Mr. Mehanati is very sincere and hard worker but he Annual Maintenance Cost+ (Salaries of Permanent Staff Per does not have any formal education in engineering and finance. His Month Minimum Monthly Electricity Bill + Minimum Monthly administrative staff is also not well educated. He is not maintaining Telephone 12 any account as per accounting standards He is worried about his Annual Fed Cost 16.30,000 new casting unit because of his lack of formal knowledge in Yearty Depreciation 0.15" (Cupola + Heating Furnace Cost engineering and finance and due to past failure. Therefore, this DG Set+Cost of Patterns Cost of Machine Block +Others) study was taken up to helo Mr. Mehanati. = 0.1551,00.000 = 7.65.000 Data Collection Variable Cost Cost of inputs assumed to vary in direct Cost data provided by Mt. Mehanati are segregated into the foed cost variable cost and mixed cost categories. Furthermored costs proportion with change in level of activity within relevant range need to be segregated into ford and variable cost elements as all for a given budget period. Table-2 astrates variable cost elements and procedure for determining variable cost per unit Indian Foundry Journal 35 Volso. No TECHNICAL PAPER Table-2: Variable Cost Elements Particulars Variable Cost 30,000 3,00,000 1000 2.250 12.250 3,21,000 Direct Material Cost for Charging Cupola Once Coal 30 per kg Cast Iron Scrap @ 34 per kg Flu Others Less scrap 5X Total Direct Material Cost Direct Labour Cost for Producing Finished Goods for Above Cupola Discharge Cost of Machining Blasting Painting. Heating Packaging for all the Products Produced Furing Charge of Cupola Other Variable Overhead Total Variable Cost for Charging Cupola Once No. of Table Stands Manufactured from Above Discharge of Cupola Variable Cost per Table Stand Weight of Sewing Machine Table Stand Table-3: Mixed Cost Composition Month Total Total XY X Units Mixed Produced Cost (9) cx) April 1134 7908 8967672 1285956 May 1584 9614 15228576 2509056 June 2171 12186 26455806 4713241 July 2353 13134 30904302 5536609 August 1672 10502 17559344 2795584 September 3458 20916 72327528 11957764 October 4856 29136 141484416 23580736 17228 103596 312927644 52378946 50.000 Substituting the values from table of mixed cost gives 103396 7+ 172286 312927644-172288 +52378946b (2) 52,000 5.000 4.08.000 600 680 14.75 kg Mixed Cost Cost of inputs which varies with change in level of activity but not in direct proportion for simplicity.we deduct total variable cost from total expenditure for a month to determine total mixed cost. Table-3 shows med cost composition Method of Least Square is explained below for segregation of mixed cost into feed and variable cost The basic straight line regression equation is Ya+bX Where Total Med Cost Fored Cost element of Med Cost Variable Cost Element of Med Cost X-Total units produced per month No of months Two linearen Ya+b3X Solving equation 1 and 2 gives a 349 D=5.86 Fored Costis? 349 per month and variable Cost is Rs5 86 per unit produced. These two cost elements are clubbed with fived and variable components calculated earlier. Total Annual Fixed Cost - 16,30,000+ 34912 = * 16.34.188 Total Variable Cost Per Table Sund - 680-586-7686 Break-Even Analysis Figure 1 shows cost-volume-profit graph while Fig2 shows profit volume graph for the company as determined below Sales Price Per Unit = 800 (excluding 4% VAT and CST Contribution Margin PerUnit (CMPUS Ssies Price Per Unit Variable Cost Per Unit - 114 Contribution to Volume C/ Ratio - CMPU / Sales Price Per Unit 14.25% Variable Cost to Volume (V/)Ratio - 100%-CN Ratio 8575% BEP Ons Total Annual Ford Cost/Contribution Margin Per UN CMPUS - 1634.188/114 -14335 55.2016 Indian Foundry lonel Break Even Sales Revenue (BESR) - Total Annual Fixed Cost/CN in near future Old companies can estimate sales volume by using Ratio appropriate forecasting method. = 16,34.188/0.1425 Projected EBT or Margin of Safety (in) = 156650114 = 114, 67.986 17,85,810 Cash Break Even Point in units) - (Total Annual Fixed Cost - Margin of Safety Ratio - Margin of Safety / Actual Sales: icm Depreciation)/CMPU = (16,34,188-7,65,000/114 - 59.53% = 7625 Desired Sales Volume in units) to earn EBT of Rs.10,00.000 Cash Break-Even Sales Revenue (CBESR) =(Total Annual Fored Cost + Desired EBD/CMPU = Total Annual Fored Cost - Depreciation)/C/V Ratio - (16,34,188 + 10,00.000) / 114 = 60.99,565 - 23107 Margin of Safety on units) - Actual Estimated Sales - BEP Gn Units) Desired Sales Volume in units) to earn EBT of 20,00,000 = 50000 - 14355 = 15665 = (Total Annual Fored Cost + Desired EBT/CMPU Sales data are estimated based on past six months sales volume = (16,34,188 + 20,00,000) / 114 and firm orders which company have received from its customers = 31879 2 49000000 1000000 X Direct material cost - Direct labour cost A Variale overheads To il cost line Toal sales revenue line Totalfixed cost line X * X . 20 Costs & Profis X . 20000 150000 X . . 1 . . Sales Figure-1: Cost Volume Profit Graph. Indian Foundry Journal DI Vol 56 No 11. Nov 2010 5000000 4000000 3000000 2000000 Profit 1000000 0 5000 - 1000000 10000 15000 20000 25000 30000 35000 40000 45000 50000 -2000000 Sales volume in units Figure-2 : Profit Volume Graph. Confirmation Revised BEP in units) - Total annual foxed cost / revised CMPU Total Sales Revenue (31879*800) 255.03.200 = 16.34.188 / 79.70 = 20504 Less Variable Cost 31879'686) 218,68,994 Incremental Analysis Total Contribution 36.34,206 Mr. Mehanati's foundry unit has capacity to produce 5000 units Less Total Fixed Cost 16.34,188 per month current plan calls for a monthly production and sales of Earning Before Tax CEBT/Earning After Tax CEAT 20,00,018 only 2500 units so his facility is idle for half of the time. Meanwhile, Ajaymer Industries, maker of flour grinding machines asked *Small-scale industries are exempted from taxes Mr. Mehanati to produce 20000 floor grinding machine stands BEP in units) if variable cost increases by BSX due to inflation weighing 30 kg each at 45.50 per kg bargaining possible). Accepting this offer will cost further ? 50,000 to Mr. Mehanati for Revised Variable Cost = 686*1.085 745 pattern making Revised CMPU 800 - 745 = 55 Mr. Mehanati estimates that its variable cost will be ? 46.50 perag Revised BEP in units) = Total Annual Fored Cost/ Revised CMPU (variable cost of sewing machine stand divided by its weight le 14.75 kg). However, its foued costs, which have been averaging = 16,34.188/55 at 3.70 per kg (Total Annual Fored Cost Actual Estimated Sales of Sewing Machine stand" its weight) will now be spread over 29713 among 1042500 kg castings (30000 14.75+20000*30). As a BEP G units) if variable cost increases by 5% due to inflation result, the average fred cost will drop to 160 per kg (1634.189 Revised Variable Cost = 6869105-720.30 + 50.000//1042500). Mr. Mehanati concluded. "Sure there will be a loss of 1 per kg on variable costs 46.50 variable cost- Revised CMPU-800-720 30 = 79.70 45.50 selling price) but there will be a gain of 2.10 per kg of 38 Vol 56 No 11. November 2010 Indian Foundry Journal castings 3.70 per kg - 1.60 per kg) by spreading the fored competitive market in such a situation, Mr. Mehanati feels that he costs. Therefore, he accepts the offer as it represents an should earn at least 6,00,000 as profit by accepting Ajaymeru advantage of 1.10 per kg" Industries offer. Now, at what bid price he will be able to achieve this profit target considering 8.5% inflation in variable cost Do we agree with Mr. Mehanati? No, we do not agree with Mr. Mehanati's view as the acceptance of the order causes loss of Mr. Mehanati estimates that its new variable cost will be Rs.50.40T 6.50,000 20000 stand 30 kg? 1+ 50,000 of pattern per kg 46.50*1085) and fixed cost will drop to 1.60 per kg making). His contention is based on the illusion that spreading the after accepting the order. Further, each kg of casting should fetch floved cost causes savings. It is also shown below by the comparative profit of Re 1 in order to achieve target profit of 6,00.000 Income statement Therefore, he estimates bid price 53 per kg (50.40+160+1). Comparative Income Statement Again, IA plays an important role to decide the competitive price Alternatives for bidding as illustrated below. Particulars Status Quo Accept Order Anticipated Variable Cost per kg 350.40 (442500 kg (1042500 kg) Additional Fixed Cost per for Pattern Making Sales Revenue 240,00,000 513,00,000** (50,000/20000*30) 30.10 Less Variable Cost 205.76.250 484,76.250 Desired Profit per kg 1.00 Total Contribution 3423,750 28,23,750 Desired Bid Price per kg of Casting 51.50 Less Foxed Cost 16,34,188 16,84.188 Now, submission of higher bid price may lead to cancellation of Profit Before Taxes 17.89,562 11,39.562 Mr Mehanati's quotation by Ajaymeru Industries. Mr. Mehanati *130000 stand x 800). "*30000 stand XT 800 + 20000 flour included existing fixed cost 150 per kg for quoting bid price. A m/estand X 20 kg x 45.50) careful look at the cost items would enable that the existing fixed Above example clearly demonstrates that the existing food costs the share of existing fixed costs should not be charged to such a costs are to be incurred irrespective of the present decision Clearly. do not increase with an increase in the output Another notable new activity, its allocation causes distortion in submission of bid aspect related to fixed costs is that spreading of such costs to a price larger output base does not yield any decrease in total fixed costs either, in spite of the decrease in the average fxed cost per unit Conclusion However, we should not infer that fixed costs are always irrelevant with the help of this case study of foundry industry, we have tried costs. In case, the additional fored costs are required to be incurred to execute decision under consideration, then the additional fixed making say, segregation of costs determination of break-even point. to illustrate the importance of BEP and IA in short-term decision costs are as relevant as variable costs. For instance, 50,000 for making pattern in above example is foed in nature but is relevant level of production to achieve desired profit acceptance of the cost because it is an additional cost caused due to special order special order and determination of bid/tender price. It is hoped that this study will be very useful for owners of SME foundry In present scenario, inflation rate of 5-10% in variable cost is quite industries common in foundry industry. As we seeinflation rate of 85% at References anticipated demand of 50.000 sewing machine stand, leads to absence of profits in any year for Mr. Mehanati at present selling Khan M. Y. and Jan P.K. (2007). "Financial Management Test. Problems and price. Further, it is difficult to sell product at higher selling price in Cases S/ETCH Indian Foundry Journal Who 2010 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Charles T. Horngren, Walter T. Harrison Jr., M. Suzanne Oliv

9th Edition

130898414, 9780132997379, 978-0130898418, 132997371, 978-0132569309