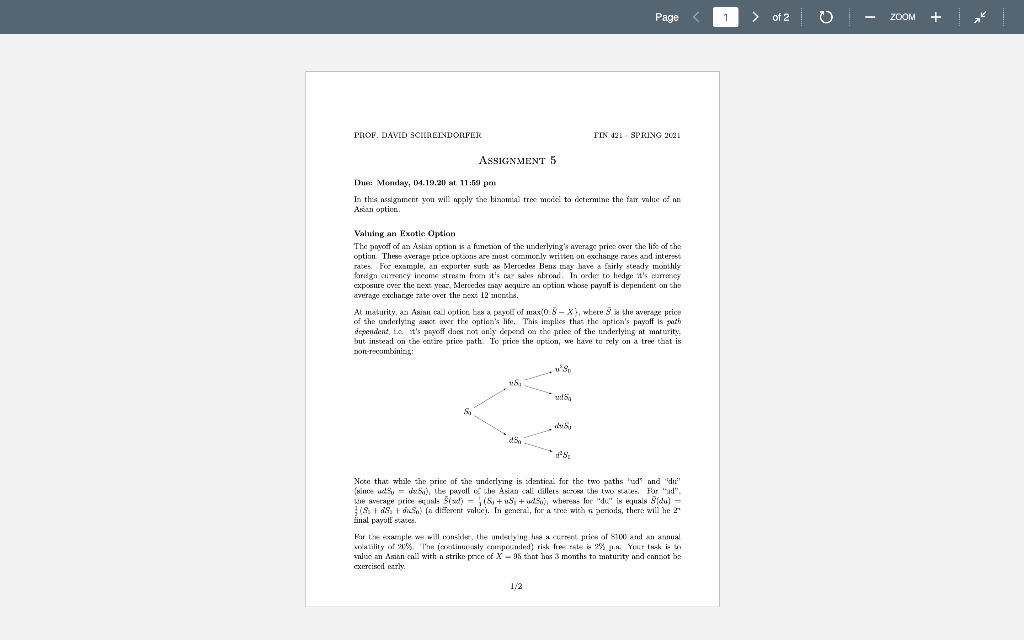

Page of 2 ZOOM PROF. DAVID SCIIREINDORFER TIN 121 SPRING 2021 ASSIGNMENT 5 Due: Monday, 04.19.20 at 11:59 pm In this assignment you will apply the blamal tro mode to determine the fair value of an Asian option Valuing an Exotic Option The power of an Asian cption is a function of the underlying's average price over the life of the option. The average price options are most comply written on exchange rates and interest rates For example, an exporter such as Mercedes Benz Day bave a fairly steady monthly kirgh Cirrency income stream from it's a sales abroad. In order to hedge it's arrek exposure over the next year, Mercedes may acquire an option whose payoff is dependent on the average exchange rate over the box 12 months At maturity, Asian call crotica basa port of max/0.5 - X), where is the average price of the underlying asst wer the option's life. This implies that the option's payoff is proto dependent, ie it's pagod das not only opeod on the price of the underlying nt maturity, trut instead on the entire price path. To price the option, we have tu rely on a tree that is tron-recombining: 15 5 S Note that while the price of the underlying is idmtia for the two paths 'od' and 'dur" since we = xutbe yoll of the Asian call dilets are the waves. For ud" he weape prius Sw) = 16,+u8 + w.), whereas for "" is wuals lau) = (SaS torso difint value. In gmeral, for a trece with i periods, there will be final payut states xatility of 21%. The continuoly compounded) rickles rate X.. Your is kito noe an Asian cnil with a strike peace of X-95 that has 3 months to maturity and cannot be exercised cry 1,2 Page of 2 ZOOM PROF. DAVID SCIIREINDORFER TIN 121 SPRING 2021 ASSIGNMENT 5 Due: Monday, 04.19.20 at 11:59 pm In this assignment you will apply the blamal tro mode to determine the fair value of an Asian option Valuing an Exotic Option The power of an Asian cption is a function of the underlying's average price over the life of the option. The average price options are most comply written on exchange rates and interest rates For example, an exporter such as Mercedes Benz Day bave a fairly steady monthly kirgh Cirrency income stream from it's a sales abroad. In order to hedge it's arrek exposure over the next year, Mercedes may acquire an option whose payoff is dependent on the average exchange rate over the box 12 months At maturity, Asian call crotica basa port of max/0.5 - X), where is the average price of the underlying asst wer the option's life. This implies that the option's payoff is proto dependent, ie it's pagod das not only opeod on the price of the underlying nt maturity, trut instead on the entire price path. To price the option, we have tu rely on a tree that is tron-recombining: 15 5 S Note that while the price of the underlying is idmtia for the two paths 'od' and 'dur" since we = xutbe yoll of the Asian call dilets are the waves. For ud" he weape prius Sw) = 16,+u8 + w.), whereas for "" is wuals lau) = (SaS torso difint value. In gmeral, for a trece with i periods, there will be final payut states xatility of 21%. The continuoly compounded) rickles rate X.. Your is kito noe an Asian cnil with a strike peace of X-95 that has 3 months to maturity and cannot be exercised cry 1,2 Page