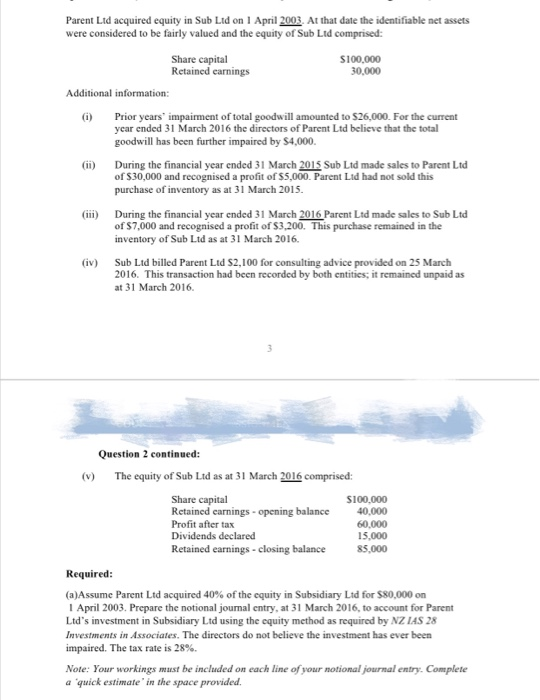

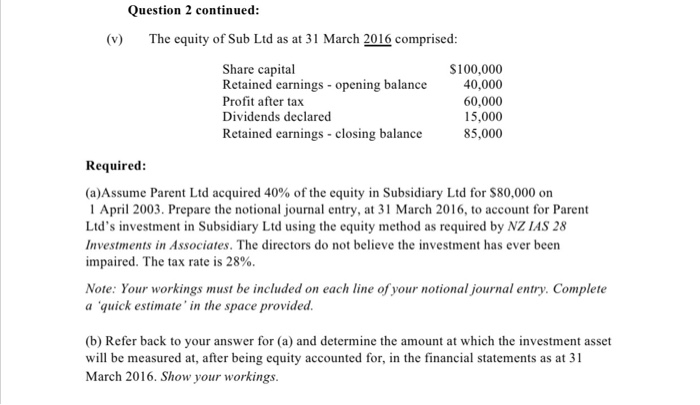

Parent Ltd acquired equity in Sub Ltd on 1 April 2003, At that date the identifiable net assets were considered to be fairly valued and the equity of Sub Ltd comprised: Share capital Retained carnings $100,000 30,000 Additional information: (i) Prior years impairment of total goodwill amounted to $26,000. For the current year ended 31 March 2016 the directors of Parent Ltd believe that the total goodwill has been further impaired by $4,000 ii) During the financial year ended 31 March 201S Sub Ltd made sales to Parent Ltd of $30,000 and recognised a profit of $5,000. Parent Ltd had not sold this purchase of inventory as at 31 March 2015 During the financial year ended 31 March 2016 Parent Ltd made sales to Sub Ltd of $7,000 and recognised a profit of S3,200. This purchase remained in the inventory of Sub Ltd as at 31 March 2016. (iv) Sub Ltd billed Parent Ltd $2,100 for consulting advice provided on 25 March 2016. This transaction had been recorded by both entities; it remained unpaid as at 31 March 2016 Question 2 continued: (v) The equity of Sub Ltd as at 31 March 2016 comprised: Share capital Retained earnings opening balance Profit after tax Dividends declared Retained earnings closing balance S100,000 40,000 60,000 15,000 85,000 Required (a)Assume Parent Ltd acquired 40% of the equity in Subsidiary Ltd for$80,000 on 1 April 2003. Prepare the notional journal entry, at 31 March 2016, to account for Parent Ltd's investment in Subsidiary Ltd using the equity method as required by NZ IAS 28 Investments in Associates. The directors do not believe the investment has ever been impaired. The tax rate is 28%. Note: Your workings must be included on each line of your notional journal entry. Complete a quick estimate in the space provided. Parent Ltd acquired equity in Sub Ltd on 1 April 2003, At that date the identifiable net assets were considered to be fairly valued and the equity of Sub Ltd comprised: Share capital Retained carnings $100,000 30,000 Additional information: (i) Prior years impairment of total goodwill amounted to $26,000. For the current year ended 31 March 2016 the directors of Parent Ltd believe that the total goodwill has been further impaired by $4,000 ii) During the financial year ended 31 March 201S Sub Ltd made sales to Parent Ltd of $30,000 and recognised a profit of $5,000. Parent Ltd had not sold this purchase of inventory as at 31 March 2015 During the financial year ended 31 March 2016 Parent Ltd made sales to Sub Ltd of $7,000 and recognised a profit of S3,200. This purchase remained in the inventory of Sub Ltd as at 31 March 2016. (iv) Sub Ltd billed Parent Ltd $2,100 for consulting advice provided on 25 March 2016. This transaction had been recorded by both entities; it remained unpaid as at 31 March 2016 Question 2 continued: (v) The equity of Sub Ltd as at 31 March 2016 comprised: Share capital Retained earnings opening balance Profit after tax Dividends declared Retained earnings closing balance S100,000 40,000 60,000 15,000 85,000 Required (a)Assume Parent Ltd acquired 40% of the equity in Subsidiary Ltd for$80,000 on 1 April 2003. Prepare the notional journal entry, at 31 March 2016, to account for Parent Ltd's investment in Subsidiary Ltd using the equity method as required by NZ IAS 28 Investments in Associates. The directors do not believe the investment has ever been impaired. The tax rate is 28%. Note: Your workings must be included on each line of your notional journal entry. Complete a quick estimate in the space provided