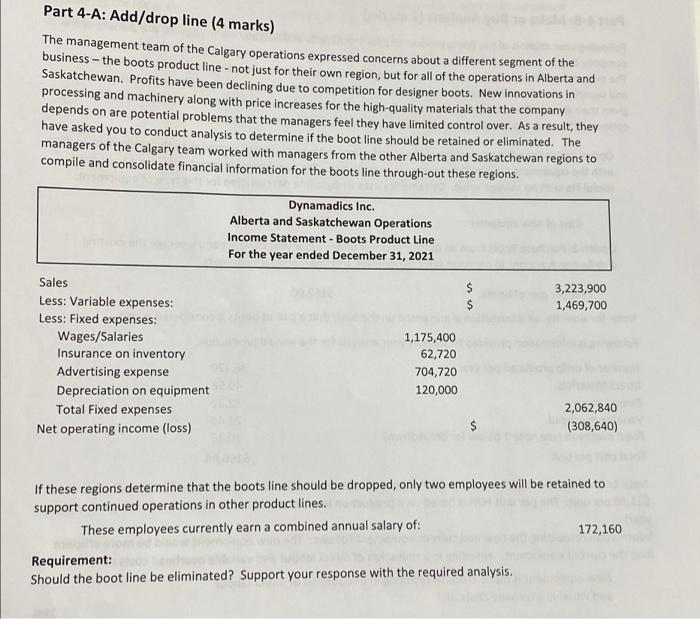

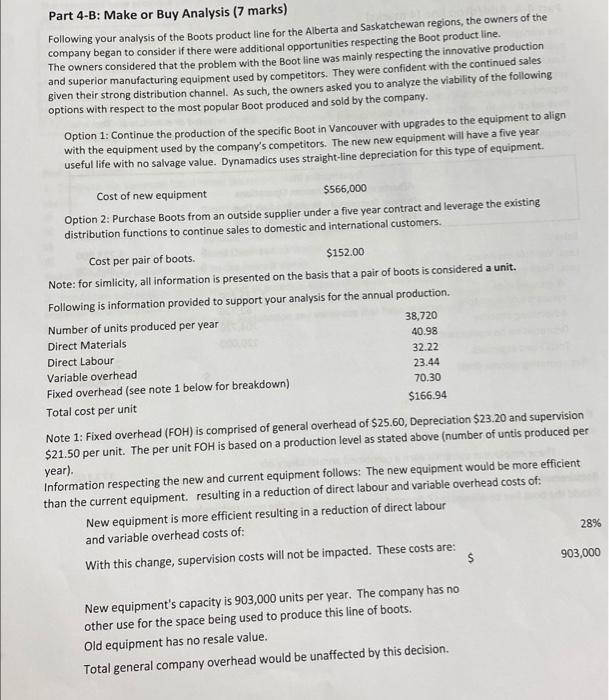

Part 4-A: Add/drop line (4 marks) The management team of the Calgary operations expressed concerns about a different segment of the business - the boots product line - not just for their own region, but for all of the operations in Alberta and Saskatchewan. Profits have been declining due to competition for designer boots. New innovations in processing and machinery along with price increases for the high-quality materials that the company depends on are potential problems that the managers feel they have limited control over. As a result, they have asked you to conduct analysis to determine if the boot line should be retained or eliminated. The managers of the Calgary team worked with managers from the other Alberta and Saskatchewan regions to compile and consolidate financial information for the boots line through-out these regions. Dynamadics Inc. Alberta and Saskatchewan Operations Income Statement - Boots Product Line For the year ended December 31, 2021 $ 3,223,900 1,469,700 Sales Less: Variable expenses: Less: Fixed expenses: Wages/Salaries Insurance on inventory Advertising expense Depreciation on equipment Total Fixed expenses Net operating income (loss) 1,175,400 62,720 704,720 120,000 2,062,840 (308,640) $ If these regions determine that the boots line should be dropped, only two employees will be retained to support continued operations in other product lines. These employees currently earn a combined annual salary of: 172,160 Requirement: Should the boot line be eliminated? Support your response with the required analysis. Part 4-B: Make or Buy Analysis (7 marks) Following your analysis of the Boots product line for the Alberta and Saskatchewan regions, the owners of the company began to consider if there were additional opportunities respecting the Boot product line. The owners considered that the problem with the Boot line was mainly respecting the innovative production and superior manufacturing equipment used by competitors. They were confident with the continued sales given their strong distribution channel. As such, the owners asked you to analyze the viability of the following options with respect to the most popular Boot produced and sold by the company. Option 1: Continue the production of the specific Boot in Vancouver with upgrades to the equipment to align with the equipment used by the company's competitors. The new new equipment will have a five year useful life with no salvage value. Dynamadics uses straight-line depreciation for this type of equipment, Cost of new equipment $566,000 Option 2: Purchase Boots from an outside supplier under a five year contract and leverage the existing distribution functions to continue sales to domestic and international customers. Cost per pair of boots $152.00 Note: for simlicity, all information is presented on the basis that a pair of boots is considered a unit. Following is information provided to support your analysis for the annual production Number of units produced per year 38,720 Direct Materials 40.98 Direct Labour 32.22 Variable overhead 23.44 Fixed overhead (see note 1 below for breakdown) 70.30 Total cost per unit $166.94 Note 1: Fixed overhead (FOH) is comprised of general overhead of $25.60, Depreciation $23.20 and supervision $21.50 per unit. The per unit FOH is based on a production level as stated above (number of untis produced per year). Information respecting the new and current equipment follows: The new equipment would be more efficient than the current equipment resulting in a reduction of direct labour and variable overhead costs of: New equipment is more efficient resulting in a reduction of direct labour and variable overhead costs of: 28% With this change, supervision costs will not be impacted. These costs are: $ 903,000 New equipment's capacity is 903,000 units per year. The company has no other use for the space being used to produce this line of boots. Old equipment has no resale value. Total general company overhead would be unaffected by this decision. Requirement: 1. Calculate the total costs and costs per unit under the two alternatives. Assume the stated units of production are expected to be produced for sale each year. (Tip: depreciation per unit will need to be calculated considering the life of the asset and the number of units being produced). 2. Based on your analysis, provide a recommendation to the owners