Answered step by step

Verified Expert Solution

Question

1 Approved Answer

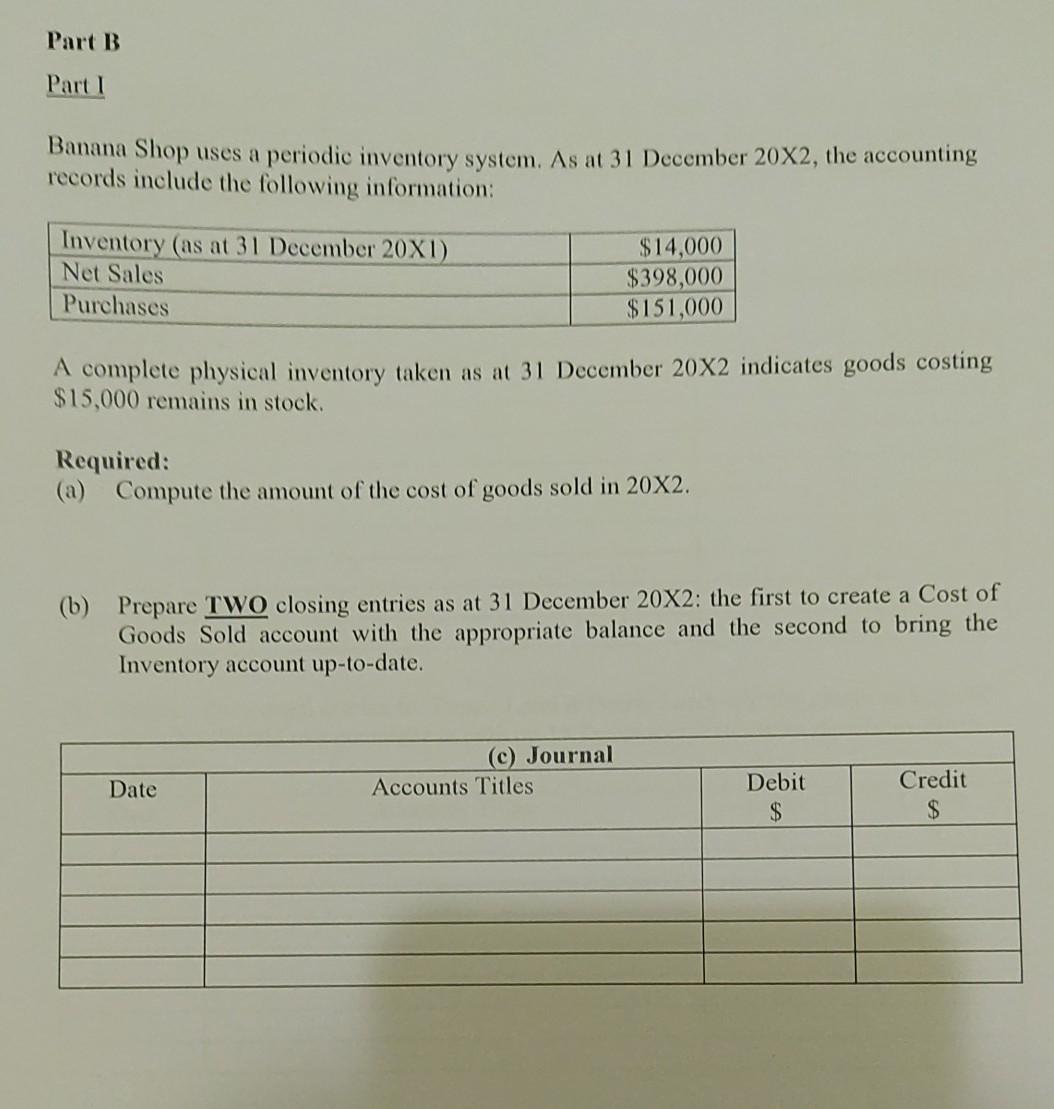

Part B Part 1 Banana Shop uses a periodic inventory system. As at 31 December 20X2, the accounting records include the following information: Inventory (as

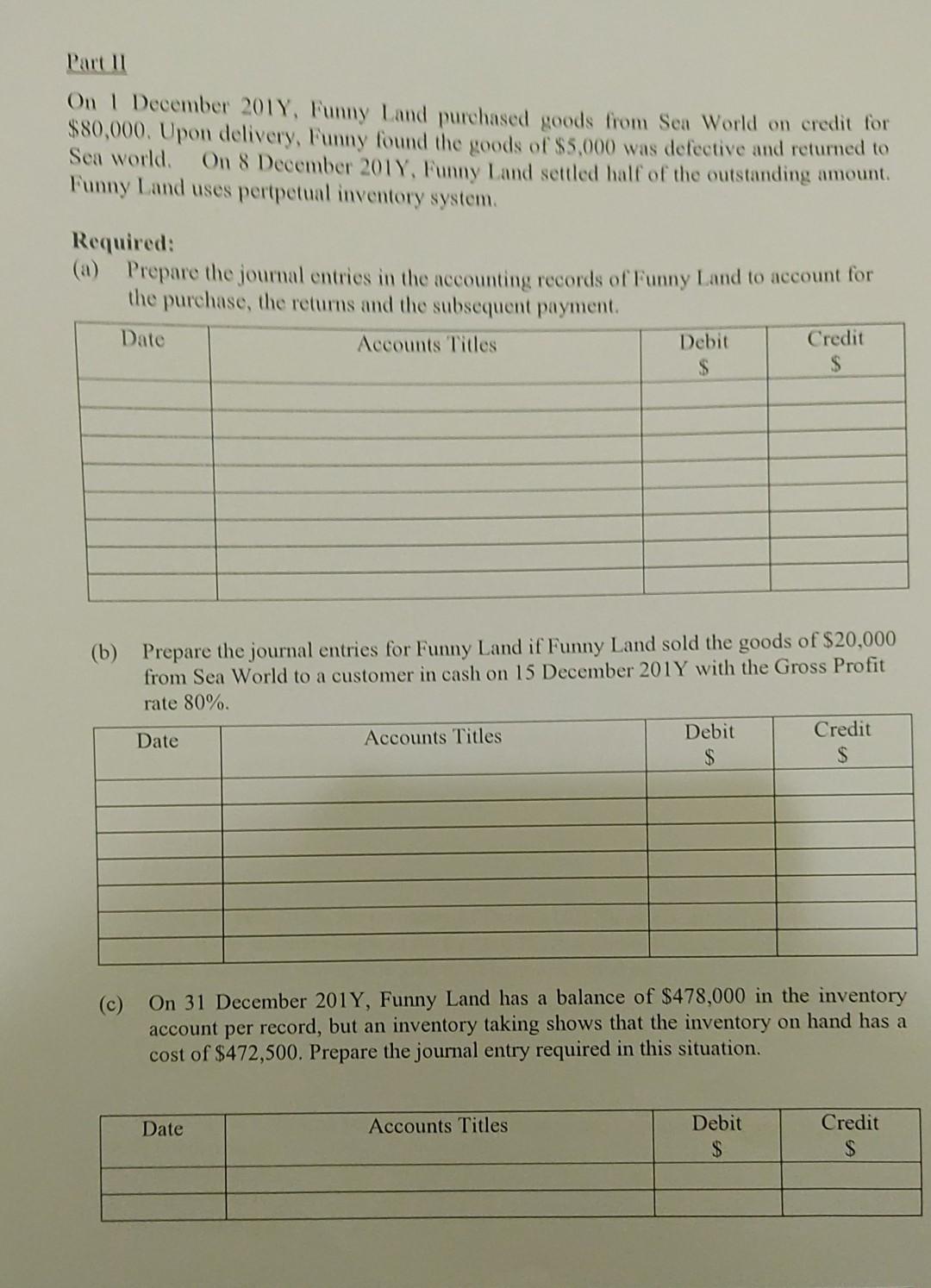

Part B Part 1 Banana Shop uses a periodic inventory system. As at 31 December 20X2, the accounting records include the following information: Inventory (as at 31 December 20X1) Net Sales Purchases $14,000 $398,000 $151,000 A complete physical inventory taken as at 31 December 20X2 indicates goods costing $15,000 remains in stock. (a) Compute the amount of the cost of goods sold in 20X2. (b) Prepare TWO closing entries as at 31 December 20X2: the first to create a Cost of Goods Sold account with the appropriate balance and the second to bring the Inventory account up-to-date. (c) Journal Accounts Titles Date Debit $ Credit $ On 1 December 2017, Funny Land purchased goods from Sea World on credit for $80,000. Upon delivery, Funny found the goods of $5,000 was defective and returned to Sea world. On 8 December 2017, Funny Land settled half of the outstanding amount Funny Land uses pertpetual inventory system. Required: Prepare the journal entries in the accounting records of Funny Land to account for the purchase, the returns and the subsequent payment. Date Accounts Titles Debit Credit S $ (b) Prepare the journal entries for Funny Land if Funny Land sold the goods of $20,000 from Sea World to a customer in cash on 15 December 2017 with the Gross Profit rate 80% Date Accounts Titles Debit $ Credit $ (c) On 31 December 2017, Funny Land has a balance of $478,000 in the inventory account per record, but an inventory taking shows that the inventory on hand has a cost of $472,500. Prepare the journal entry required in this situation. Date Accounts Titles Debit $ Credit $

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Managerial Accounting

Authors: Robert Meigs Jan Williams, Sue Haka, Mark S Bettner

16th Edition

0077557344, 978-0077557348