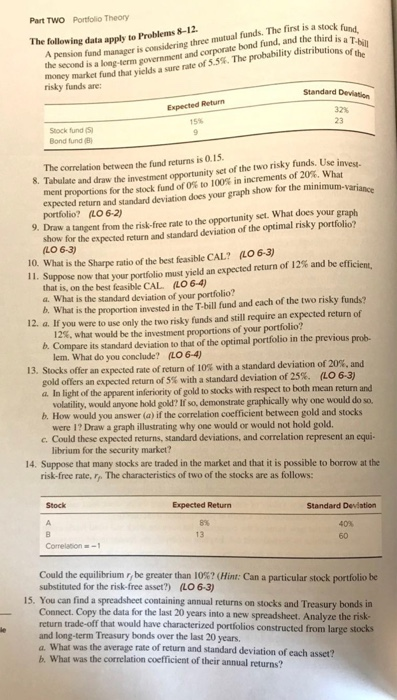

Part TWO Portfolio Theory distributions of the The following data apply to Problems 8-12 pension fund manager is considering three mutual funds. The first is a stock te bond fund, and the third is at the second is a long-term government and cop money market fund that violds a sure rate of 5.5. The probability distributions risky funds are: Standard Deviation Expected Return 15% Stock fund (5) Bond fund The correlation between the fund returns is 0.15. Tabulate and draw the investment opportunity set of the two risky funds. Use inves ment proportions for the stock fund of Os to 100% in increments of 20%. What expected return and standard deviation does your graph show for the minimum-Varian portfolio? (LO 6-2) 9. Draw a tangent from the risk-free rate to the opportunity set. What does your graph show for the expected return and standard deviation of the optimal risky portfolio? (LO 6-3) 10. What is the Sharpe ratio of the best feasible CAL? (10 6-3) 1. Suppose now that your portfolio must vield an expected return of 12% and be efficient that is, on the best feasible CAL (LO 6-4) a. What is the standard deviation of your portfolio? b. What is the proportion invested in the T-bill fund and each of the two risky funds? 12. a. If you were to use only the two risky funds and still require an expected return of 12%, what would be the investment proportions of your portfolio? b. Compare its standard deviation to that of the optimal portfolio in the previous prob- lem. What do you conclude? (LO 6-4) 13. Stocks offer an expected rate of return of 10% with a standard deviation of 20%, and gold offers an expected return of 5% with a standard deviation of 25%. (LO 6-3) a. In light of the apparent inferiority of gold to stocks with respect to both mean return and volatility, would anyone hold gold? If so, demonstrate graphically why one would do so. b. How would you answer (a) if the correlation coefficient between gold and stocks were 1? Draw a graph illustrating why one would or would not hold gold. c. Could these expected returns, standard deviations, and correlation represent an equi- librium for the security market? 14. Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free rate. The characteristics of two of the stocks are as follows: Stock Expected Return Standard Deviation 40% Correlation -1 Could the equilibrium r be greater than 10%? (Hint: Can a particular stock portfolio be substituted for the risk-free asset?) (LO 6-3) 15. You can find a spreadsheet containing annual returns on stocks and Treasury bonds in Connect. Copy the data for the last 20 years into a new spreadsheet. Analyze the risk- return trade-off that would have characterized portfolios constructed from large stocks and long-term Treasury bonds over the last 20 years. a. What was the average rate of return and standard deviation of each asset? b. What was the correlation coefficient of their annual returns? Part TWO Portfolio Theory distributions of the The following data apply to Problems 8-12 pension fund manager is considering three mutual funds. The first is a stock te bond fund, and the third is at the second is a long-term government and cop money market fund that violds a sure rate of 5.5. The probability distributions risky funds are: Standard Deviation Expected Return 15% Stock fund (5) Bond fund The correlation between the fund returns is 0.15. Tabulate and draw the investment opportunity set of the two risky funds. Use inves ment proportions for the stock fund of Os to 100% in increments of 20%. What expected return and standard deviation does your graph show for the minimum-Varian portfolio? (LO 6-2) 9. Draw a tangent from the risk-free rate to the opportunity set. What does your graph show for the expected return and standard deviation of the optimal risky portfolio? (LO 6-3) 10. What is the Sharpe ratio of the best feasible CAL? (10 6-3) 1. Suppose now that your portfolio must vield an expected return of 12% and be efficient that is, on the best feasible CAL (LO 6-4) a. What is the standard deviation of your portfolio? b. What is the proportion invested in the T-bill fund and each of the two risky funds? 12. a. If you were to use only the two risky funds and still require an expected return of 12%, what would be the investment proportions of your portfolio? b. Compare its standard deviation to that of the optimal portfolio in the previous prob- lem. What do you conclude? (LO 6-4) 13. Stocks offer an expected rate of return of 10% with a standard deviation of 20%, and gold offers an expected return of 5% with a standard deviation of 25%. (LO 6-3) a. In light of the apparent inferiority of gold to stocks with respect to both mean return and volatility, would anyone hold gold? If so, demonstrate graphically why one would do so. b. How would you answer (a) if the correlation coefficient between gold and stocks were 1? Draw a graph illustrating why one would or would not hold gold. c. Could these expected returns, standard deviations, and correlation represent an equi- librium for the security market? 14. Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free rate. The characteristics of two of the stocks are as follows: Stock Expected Return Standard Deviation 40% Correlation -1 Could the equilibrium r be greater than 10%? (Hint: Can a particular stock portfolio be substituted for the risk-free asset?) (LO 6-3) 15. You can find a spreadsheet containing annual returns on stocks and Treasury bonds in Connect. Copy the data for the last 20 years into a new spreadsheet. Analyze the risk- return trade-off that would have characterized portfolios constructed from large stocks and long-term Treasury bonds over the last 20 years. a. What was the average rate of return and standard deviation of each asset? b. What was the correlation coefficient of their annual returns