Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Peder Mueller-UIA (B). Peder Mueller is a foreign exchange trader for a bank in New York. Using the values and assumptions here,, he decides

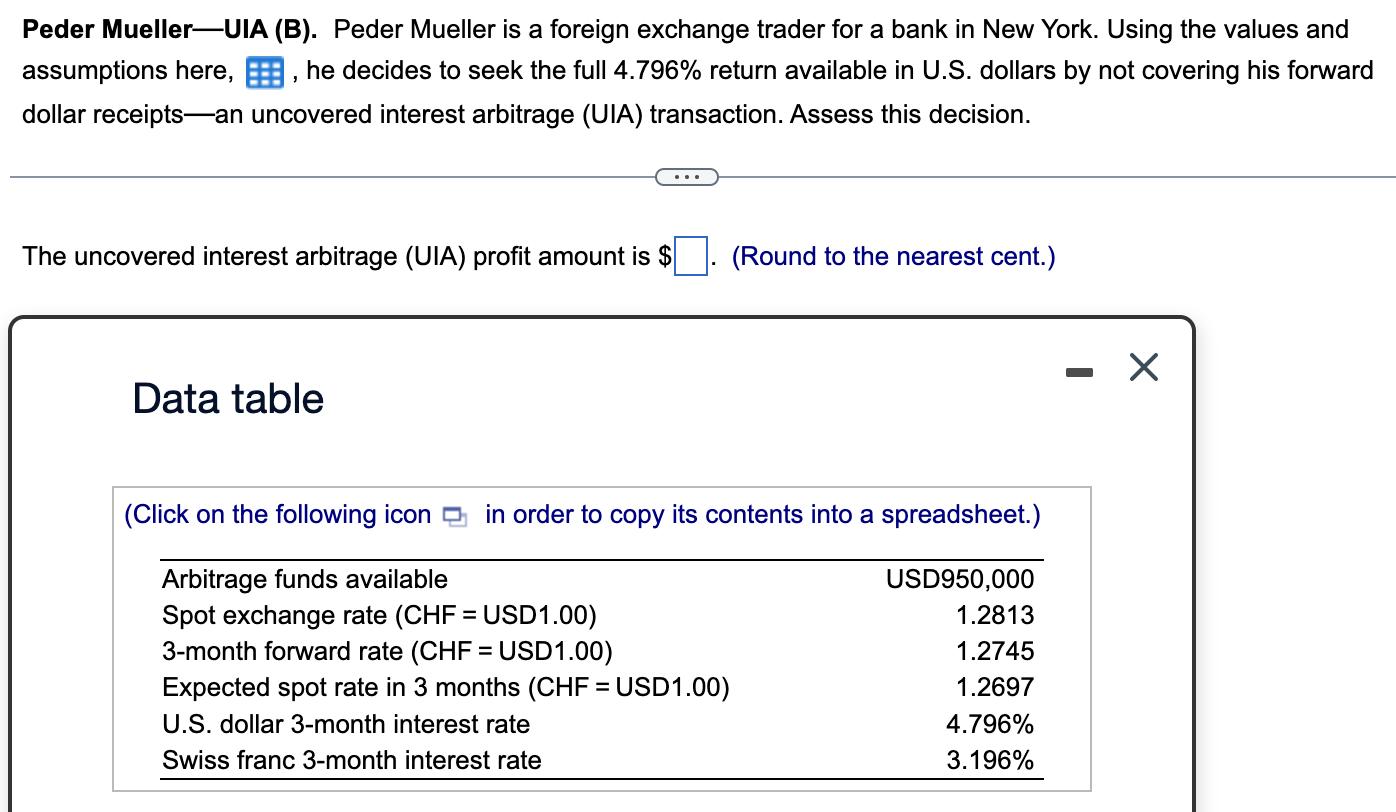

Peder Mueller-UIA (B). Peder Mueller is a foreign exchange trader for a bank in New York. Using the values and assumptions here,, he decides to seek the full 4.796% return available in U.S. dollars by not covering his forward dollar receipts an uncovered interest arbitrage (UIA) transaction. Assess this decision. The uncovered interest arbitrage (UIA) profit amount is $ Data table (Round to the nearest cent.) (Click on the following icon in order to copy its contents into a spreadsheet.) Arbitrage funds available USD950,000 Spot exchange rate (CHF = USD1.00) 1.2813 3-month forward rate (CHF = USD 1.00) 1.2745 Expected spot rate in 3 months (CHF = USD1.00) 1.2697 U.S. dollar 3-month interest rate 4.796% Swiss franc 3-month interest rate 3.196% X

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To assess Peder Muellers decision to engage in uncovered interest arbitrage UIA we need to calculate ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting Financial Statement Analysis And Valuation A Strategic Perspective

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

9th Edition

1337614689, 1337614688, 9781337668262, 978-1337614689