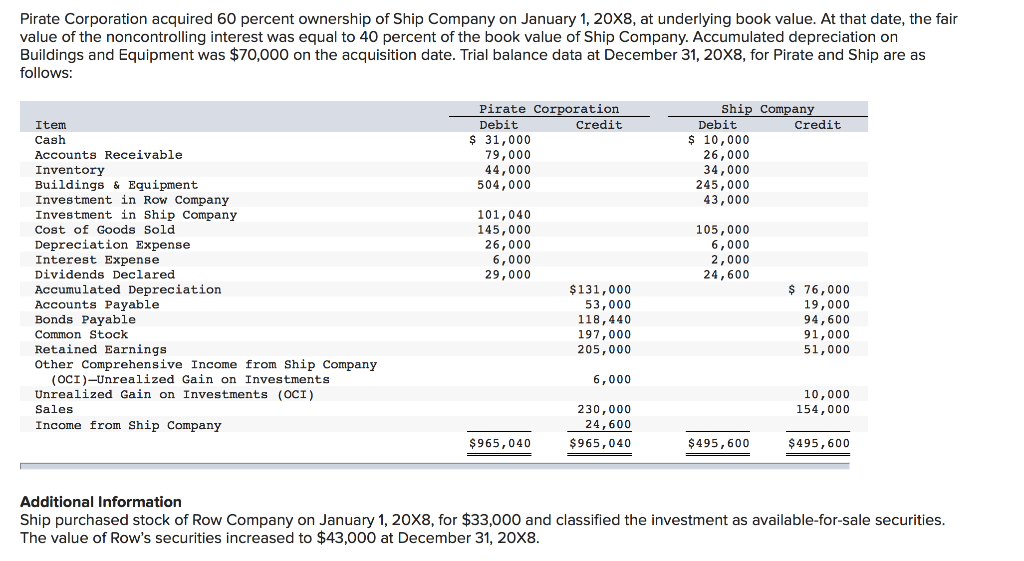

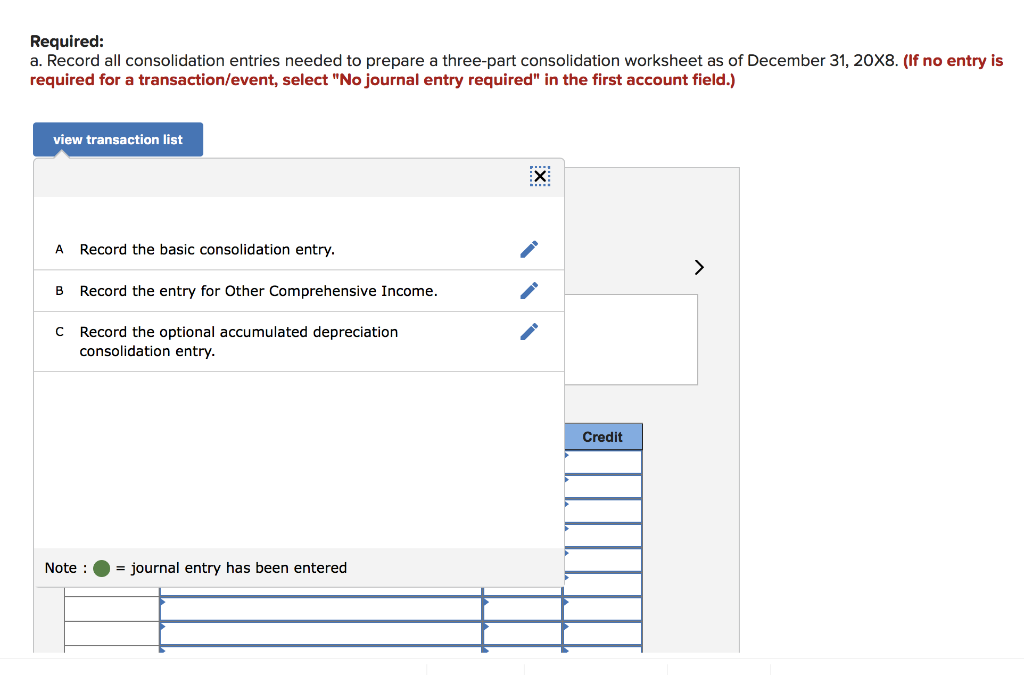

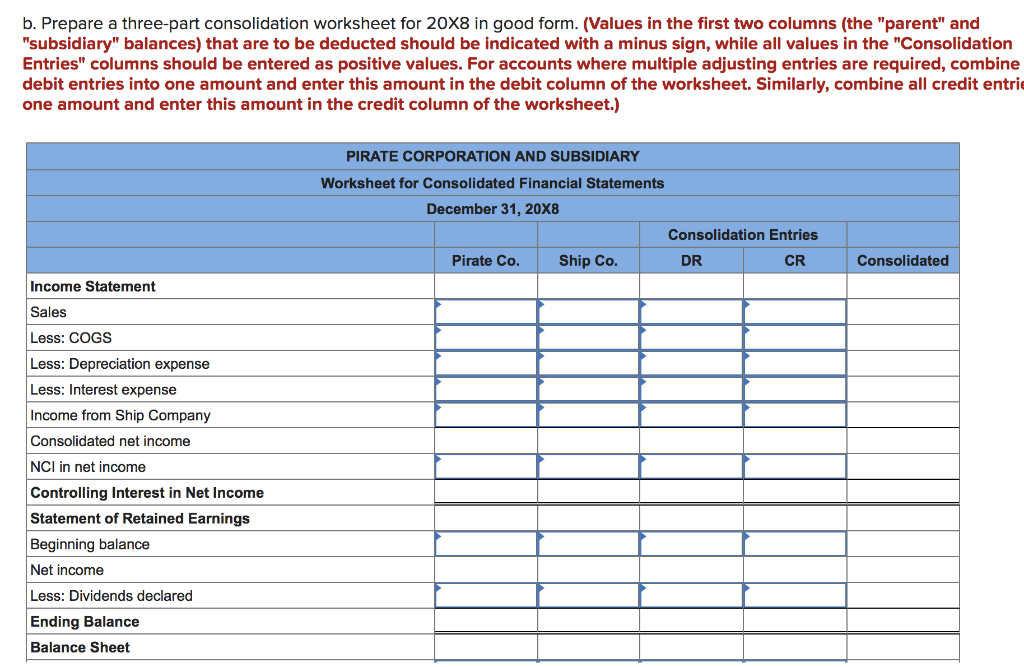

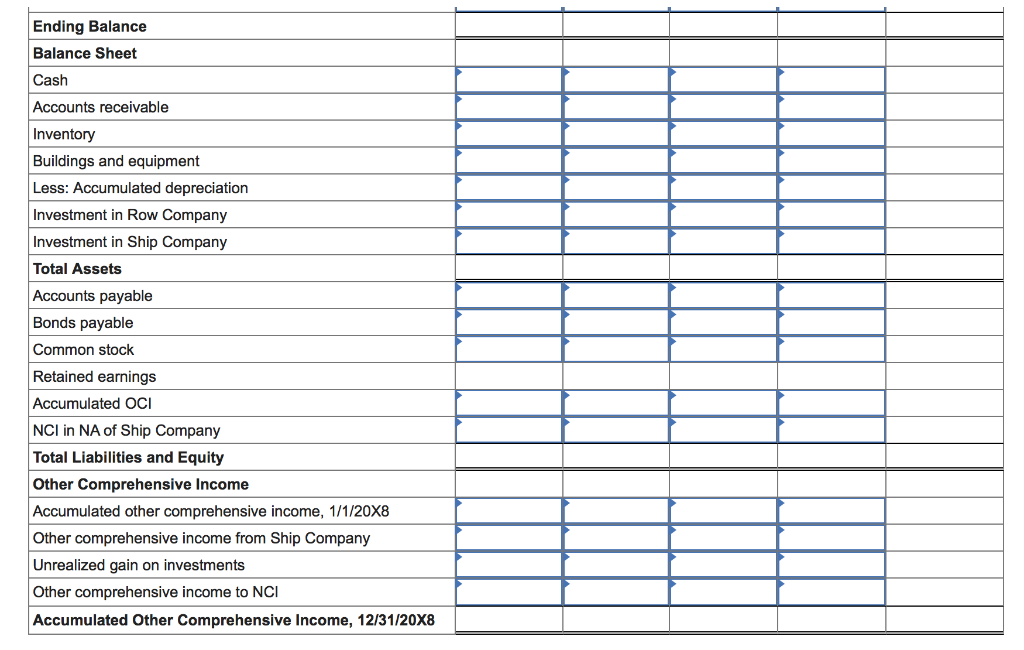

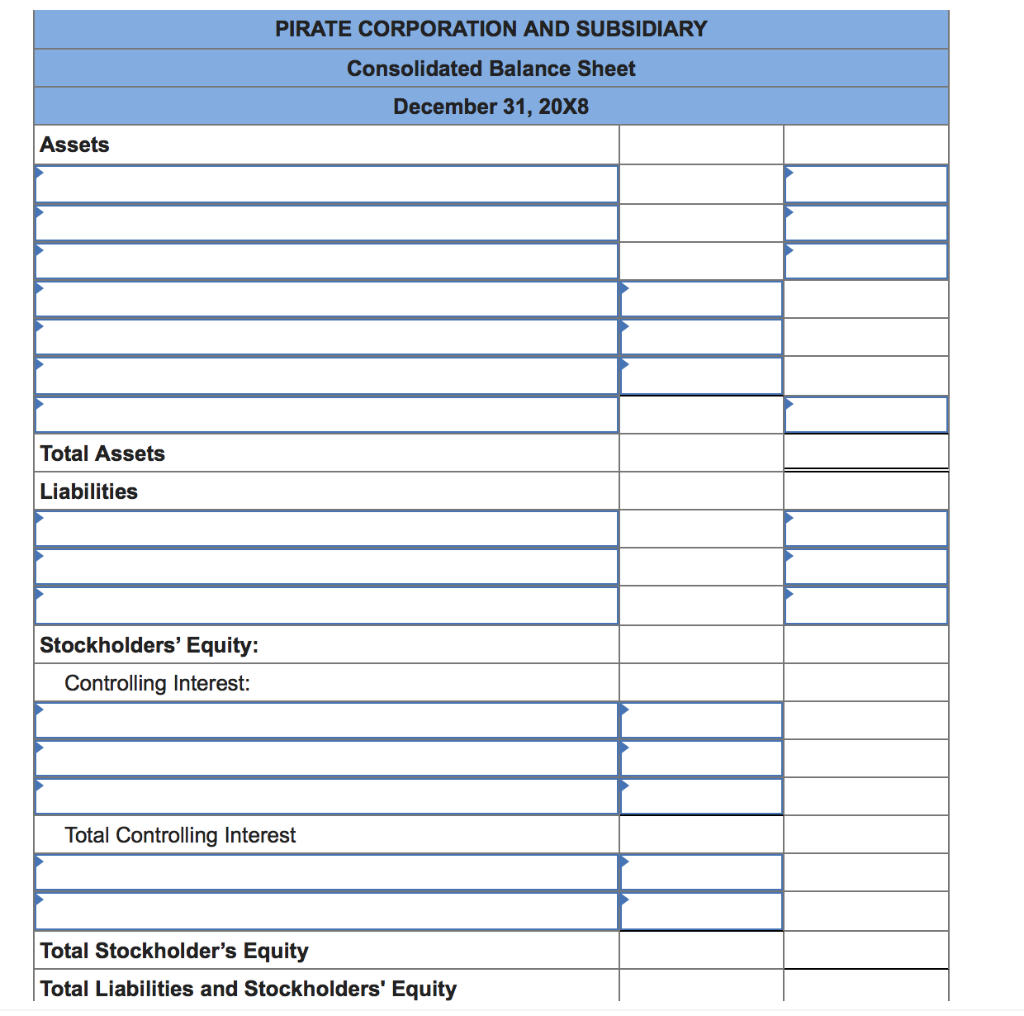

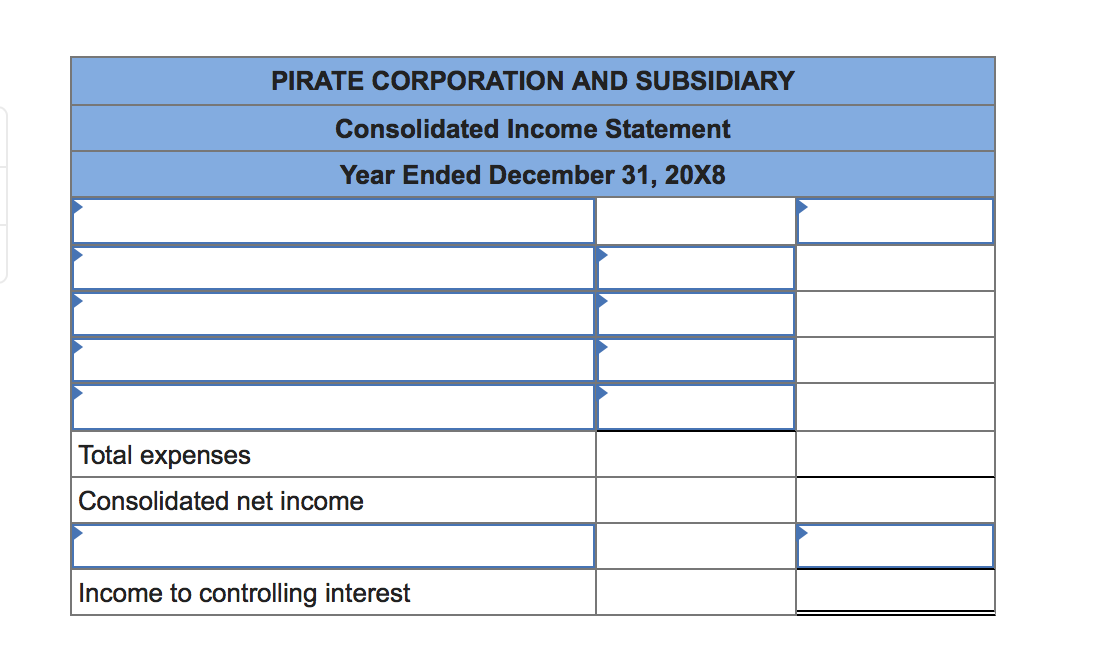

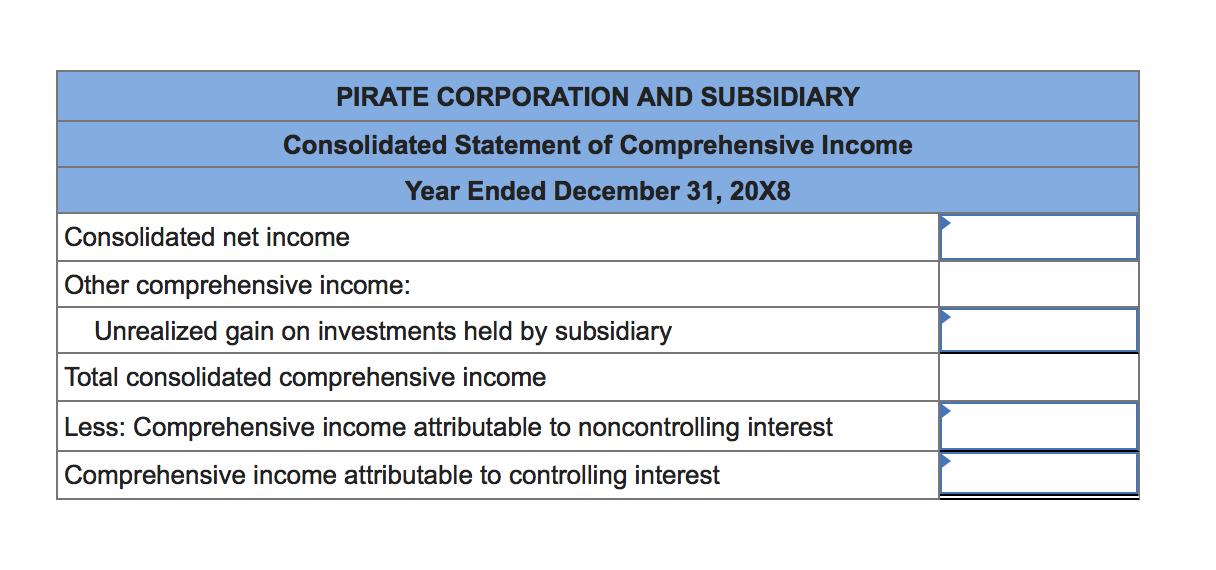

Pirate Corporation acquired 60 percent ownership of Ship Company on January 1, 20X8, at underlying book value. At that date, the fair value of the noncontrolling interest was equal to 40 percent of the book value of Ship Company. Accumulated depreciation on Buildings and Equipment was $70,000 on the acquisition date. Trial balance data at December 31, 20X8, for Pirate and Ship are as follows: Pirate Corporation Debit Credit $ 31,000 79,000 44,000 504,000 Ship Company Debit Credit $ 10,000 26,000 34,000 245,000 43,000 Item Cash Accounts Receivable Inventory Buildings & Equipment Investment in Row Company Investment in Ship Company Cost of Goods Sold Depreciation Expense Interest Expense Dividends Declared Accumulated Depreciation Accounts Payable Bonds Payable Common Stock Retained Earnings Other Comprehensive Income from Ship Company (OCI)Unrealized Gain on Investments Unrealized Gain on Investments (OCI) Sales Income from Ship Company 101,040 145,000 26,000 6,000 29,000 105,000 6,000 2,000 24,600 $ 131,000 53,000 118,440 197,000 205,000 $ 76,000 19,000 94,600 91,000 51,000 6,000 10,000 154,000 $965,040 230,000 24,600 $965,040 $495,600 $495,600 Additional Information Ship purchased stock of Row Company on January 1, 20X8, for $33,000 and classified the investment as available-for-sale securities. The value of Row's securities increased to $43,000 at December 31, 20X8. Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) view transaction list X Record the basic consolidation entry. > B Record the entry for Other Comprehensive Income. Record the optional accumulated depreciation consolidation entry. Credit Note : journal entry has been entered view transaction list Consolidation Worksheet Entries Record the basic consolidation entry. Note: Enter debits before credits. Entry Accounts Debit Credit 1 Record entry Clear entry view consolidation entries b. Prepare a three-part consolidation worksheet for 20X8 in good form. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entrie one amount and enter this amount in the credit column of the worksheet.) PIRATE CORPORATION AND SUBSIDIARY Worksheet for Consolidated Financial Statements December 31, 20X8 Consolidation Entries Pirate Co. Ship Co. DR CR Consolidated Income Statement Sales Less: COGS Less: Depreciation expense Less: Interest expense Income from Ship Company Consolidated net income NCI in net income Controlling Interest in Net Income Statement of Retained Earnings Beginning balance Net income Less: Dividends declared Ending Balance Balance Sheet Ending Balance Balance Sheet Cash Accounts receivable Inventory Buildings and equipment Less: Accumulated depreciation Investment in Row Company Investment in Ship Company Total Assets Accounts payable Bonds payable Common stock Retained earnings Accumulated OCI NCI in NA of Ship Company Total Liabilities and Equity Other Comprehensive Income Accumulated other comprehensive income, 1/1/20X8 Other comprehensive income from Ship Company Unrealized gain on investments Other comprehensive income to NCI Accumulated Other Comprehensive Income, 12/31/20X8 PIRATE CORPORATION AND SUBSIDIARY Consolidated Balance Sheet December 31, 20X8 Assets Total Assets Liabilities Stockholders' Equity: Controlling Interest: Total Controlling Interest Total Stockholder's Equity Total Liabilities and Stockholders' Equity PIRATE CORPORATION AND SUBSIDIARY Consolidated Income Statement Year Ended December 31, 20X8 Total expenses Consolidated net income Income to controlling interest PIRATE CORPORATION AND SUBSIDIARY Consolidated Statement of Comprehensive Income Year Ended December 31, 20X8 Consolidated net income Other comprehensive income: Unrealized gain on investments held by subsidiary Total consolidated comprehensive income Less: Comprehensive income attributable to noncontrolling interest Comprehensive income attributable to controlling interest Pirate Corporation acquired 60 percent ownership of Ship Company on January 1, 20X8, at underlying book value. At that date, the fair value of the noncontrolling interest was equal to 40 percent of the book value of Ship Company. Accumulated depreciation on Buildings and Equipment was $70,000 on the acquisition date. Trial balance data at December 31, 20X8, for Pirate and Ship are as follows: Pirate Corporation Debit Credit $ 31,000 79,000 44,000 504,000 Ship Company Debit Credit $ 10,000 26,000 34,000 245,000 43,000 Item Cash Accounts Receivable Inventory Buildings & Equipment Investment in Row Company Investment in Ship Company Cost of Goods Sold Depreciation Expense Interest Expense Dividends Declared Accumulated Depreciation Accounts Payable Bonds Payable Common Stock Retained Earnings Other Comprehensive Income from Ship Company (OCI)Unrealized Gain on Investments Unrealized Gain on Investments (OCI) Sales Income from Ship Company 101,040 145,000 26,000 6,000 29,000 105,000 6,000 2,000 24,600 $ 131,000 53,000 118,440 197,000 205,000 $ 76,000 19,000 94,600 91,000 51,000 6,000 10,000 154,000 $965,040 230,000 24,600 $965,040 $495,600 $495,600 Additional Information Ship purchased stock of Row Company on January 1, 20X8, for $33,000 and classified the investment as available-for-sale securities. The value of Row's securities increased to $43,000 at December 31, 20X8. Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) view transaction list X Record the basic consolidation entry. > B Record the entry for Other Comprehensive Income. Record the optional accumulated depreciation consolidation entry. Credit Note : journal entry has been entered view transaction list Consolidation Worksheet Entries Record the basic consolidation entry. Note: Enter debits before credits. Entry Accounts Debit Credit 1 Record entry Clear entry view consolidation entries b. Prepare a three-part consolidation worksheet for 20X8 in good form. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entrie one amount and enter this amount in the credit column of the worksheet.) PIRATE CORPORATION AND SUBSIDIARY Worksheet for Consolidated Financial Statements December 31, 20X8 Consolidation Entries Pirate Co. Ship Co. DR CR Consolidated Income Statement Sales Less: COGS Less: Depreciation expense Less: Interest expense Income from Ship Company Consolidated net income NCI in net income Controlling Interest in Net Income Statement of Retained Earnings Beginning balance Net income Less: Dividends declared Ending Balance Balance Sheet Ending Balance Balance Sheet Cash Accounts receivable Inventory Buildings and equipment Less: Accumulated depreciation Investment in Row Company Investment in Ship Company Total Assets Accounts payable Bonds payable Common stock Retained earnings Accumulated OCI NCI in NA of Ship Company Total Liabilities and Equity Other Comprehensive Income Accumulated other comprehensive income, 1/1/20X8 Other comprehensive income from Ship Company Unrealized gain on investments Other comprehensive income to NCI Accumulated Other Comprehensive Income, 12/31/20X8 PIRATE CORPORATION AND SUBSIDIARY Consolidated Balance Sheet December 31, 20X8 Assets Total Assets Liabilities Stockholders' Equity: Controlling Interest: Total Controlling Interest Total Stockholder's Equity Total Liabilities and Stockholders' Equity PIRATE CORPORATION AND SUBSIDIARY Consolidated Income Statement Year Ended December 31, 20X8 Total expenses Consolidated net income Income to controlling interest PIRATE CORPORATION AND SUBSIDIARY Consolidated Statement of Comprehensive Income Year Ended December 31, 20X8 Consolidated net income Other comprehensive income: Unrealized gain on investments held by subsidiary Total consolidated comprehensive income Less: Comprehensive income attributable to noncontrolling interest Comprehensive income attributable to controlling interest