Please answer all 4 parts and i will give positive rating. Thanks!

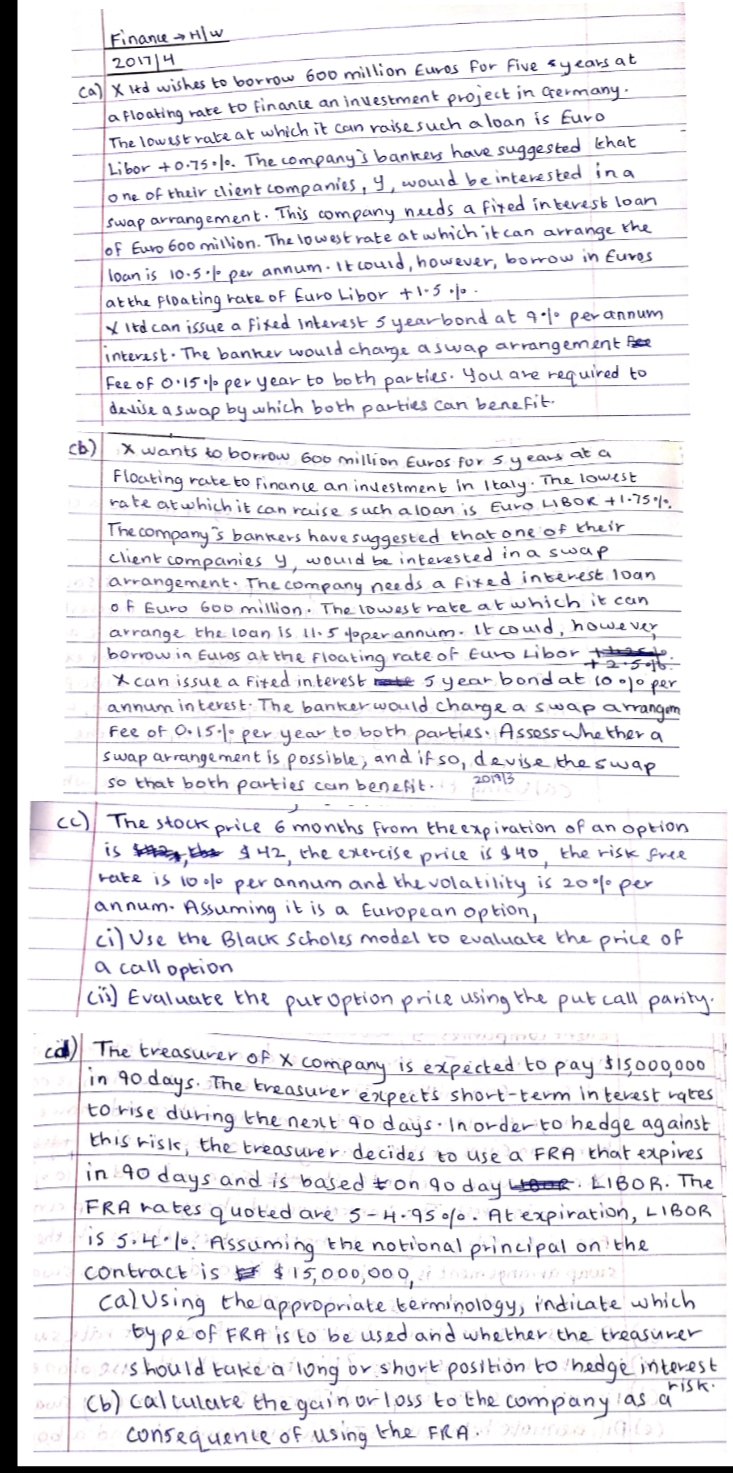

Finance Hw 20114 ca) X td wishes to borrow 600 million Euros for five syears at a floating rate to finance an investment project in Germany. The lowest rate at which it can raise such a loan is Euro Libor +0.75.le. The company's bankers have suggested that one of their client companies, y, would be interested ina swap arrangement. This company needs a fixed interest loan of Euro 600 million. The lowest rate at which it can arrange loan is 10.5.12 per annum. It could, however, borrow in Euros at the floating rate of Euro Libor +1.5.10 Xitd can issue a fixed interest 5 yearbondat qol per annum interest. The banker would change a swap arrangement free Fee of 0.15% per year to both parties. You are required to devise a swap by which both parties can benefit (b) x wants to borrow 600 million Euros for sy ears at a Floating rate to Finance an investment in Italy. The lowest rate at which it can raise such a loan is Euro HBOK +1.750. | he company 5 bankers have suggested that one of their client companies y, would be interested in a swap arrangement. The company needs a fixed interest loan of Euro Goo million. The lowest rate at which it can arrange the loan is 11.5 qoper annum. it could, however borrow in Euros at the Floating rate of Euro Libor +2.5.16 X can issue a Fited interest rate 5 year bondat 10 olo per annum interest. The banker would change a swap arrangem fee of 0.15.10 per year to both parties. Assess whether a swap arrangement is possible, and if so, devise the swap so that both parties can benefit 201113 (c) The stock price 6 months from the expiration of an option is an abs $42, the exercise price is $40, the risk free rake is 10% per annum and the volatility is 20% per annum. Assuming it is a European option, cil Use the Black Scholes model to evaluate the price of a call option (is) Evaluate the put option price using the put call parity. 90 The treasurer of X company is expected to pay $15,000,000 in 90 days. The treasurer expect's short-term interest rates to rise during the neat 90 days in order to hedge against this risic, the treasurer decides to use a FRA that expires in 40 days and is based tongo day LIBOR. The FRA rates quoted are 5-6.9500. At expiration, LIBOR is gondol. Assuming the notional principal on the contract is $15,000,000, torej po 2017 cal Using the appropriate terminology, indicate which type of FRA is to be used and whether the treasurer 12 3115 kould take a long or short position to thedge interest risk. (Cb) calculate the gain or loss to the company as a consequence of using the FRA novostao)