Answered step by step

Verified Expert Solution

Question

1 Approved Answer

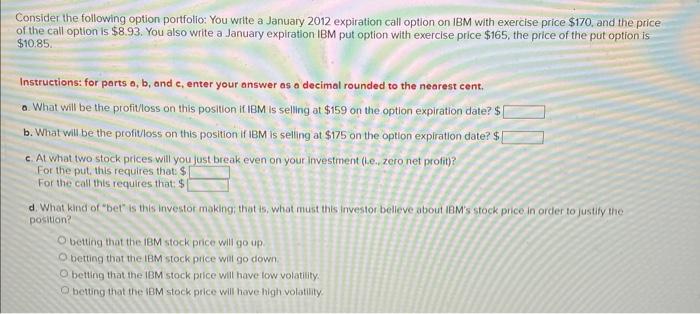

Please answer all parts. No need to show work! Consider the following option portfolio: You write a January 2012 expiration call option on IBM with

Please answer all parts. No need to show work!

Consider the following option portfolio: You write a January 2012 expiration call option on IBM with exercise price $170, and the price of the call option is $8.93. You also write a January expiration IBM put option with exercise price $165, the price of the put option is $10.85 Instructions: for parts a,b, and c, enter your answer as o decimal rounded to the nearest cent. a. What will be the profitloss on this position if IBM Is selling at $159 on the option expiration date? $ b. What will be the profitloss on this position if IBM is selling at $175 on the option expiration date? $ c. At what two stock prices will you lust break even on your investment (Le., zero net profit)? For the put, this requires that:\$ For the call this requires that: $ d. What kind of "bet" is this investor making; that is, what must this investor belleve about IBM's stock price in order to justify the position? betting that the 18M stock price will go up. betting that the IBM stock pice will go down. betting that the IBM stock price will have low volatility. betting that the IBM stock price will have high volatility Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investing From Scratch A Handbook For The Young Investor

Authors: James Lowell

1st Edition

014303684X, 978-0143036845